Direct Costing allocates only variable manufacturing costs to products, treating fixed costs as period expenses, which enhances short-term decision-making and cost control. Absorption Costing assigns both fixed and variable manufacturing costs to products, aligning with GAAP and providing a comprehensive view of product cost for external reporting. Discover more about how these costing methods impact financial analysis and strategic planning.

Main Difference

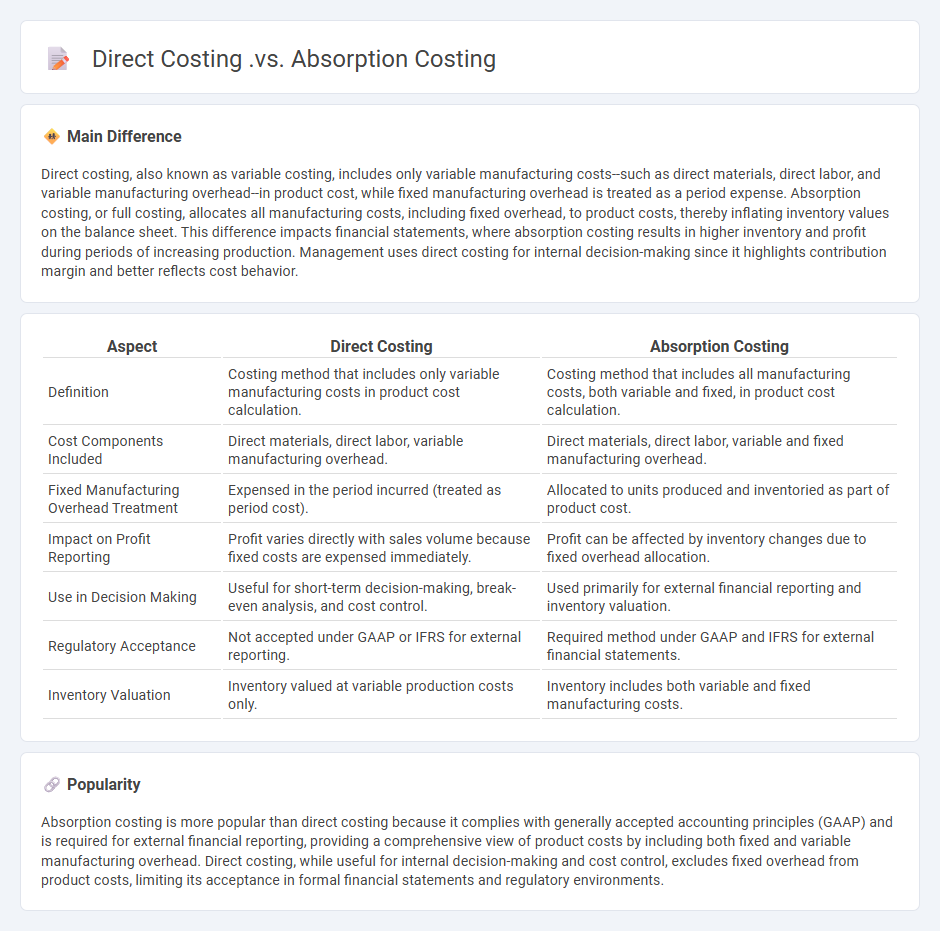

Direct costing, also known as variable costing, includes only variable manufacturing costs--such as direct materials, direct labor, and variable manufacturing overhead--in product cost, while fixed manufacturing overhead is treated as a period expense. Absorption costing, or full costing, allocates all manufacturing costs, including fixed overhead, to product costs, thereby inflating inventory values on the balance sheet. This difference impacts financial statements, where absorption costing results in higher inventory and profit during periods of increasing production. Management uses direct costing for internal decision-making since it highlights contribution margin and better reflects cost behavior.

Connection

Direct costing and absorption costing are connected through their approach to expense allocation, with direct costing assigning only variable manufacturing costs to products while treating fixed manufacturing overhead as a period expense, and absorption costing including both variable and fixed manufacturing costs in product costs. This relationship impacts inventory valuation and profitability analysis, as absorption costing typically results in higher inventory values and affects net income during periods of inventory fluctuation. Understanding this connection is crucial for management decision-making, cost control, and financial reporting compliance.

Comparison Table

| Aspect | Direct Costing | Absorption Costing |

|---|---|---|

| Definition | Costing method that includes only variable manufacturing costs in product cost calculation. | Costing method that includes all manufacturing costs, both variable and fixed, in product cost calculation. |

| Cost Components Included | Direct materials, direct labor, variable manufacturing overhead. | Direct materials, direct labor, variable and fixed manufacturing overhead. |

| Fixed Manufacturing Overhead Treatment | Expensed in the period incurred (treated as period cost). | Allocated to units produced and inventoried as part of product cost. |

| Impact on Profit Reporting | Profit varies directly with sales volume because fixed costs are expensed immediately. | Profit can be affected by inventory changes due to fixed overhead allocation. |

| Use in Decision Making | Useful for short-term decision-making, break-even analysis, and cost control. | Used primarily for external financial reporting and inventory valuation. |

| Regulatory Acceptance | Not accepted under GAAP or IFRS for external reporting. | Required method under GAAP and IFRS for external financial statements. |

| Inventory Valuation | Inventory valued at variable production costs only. | Inventory includes both variable and fixed manufacturing costs. |

Variable Costs

Variable costs in business refer to expenses that fluctuate directly with production volume or sales activity, such as raw materials, direct labor, and utility costs tied to manufacturing. These costs differ from fixed costs and are vital for calculating the contribution margin and break-even point. Businesses must monitor variable costs to optimize pricing strategies and maintain profitability during changes in demand. Efficient management of variable costs enables companies to scale operations and adjust to market conditions effectively.

Fixed Manufacturing Overhead

Fixed manufacturing overhead represents the consistent indirect costs incurred during production, such as factory rent, property taxes, and salaried personnel expenses, that remain unchanged regardless of output levels. These costs are allocated to products through predetermined overhead rates to ensure accurate product costing and inventory valuation. Proper management and allocation of fixed manufacturing overhead are essential for effective budgeting, cost control, and profitability analysis in business operations. Understanding fixed overhead helps businesses set pricing strategies and forecast financial performance accurately.

Inventory Valuation

Inventory valuation plays a critical role in business accounting by determining the cost assigned to inventory for financial reporting and tax purposes. Methods such as First-In, First-Out (FIFO), Last-In, First-Out (LIFO), and Weighted Average Cost directly impact gross profit and taxable income. Accurate inventory valuation ensures compliance with financial standards like GAAP and IFRS while reflecting true business performance. Advanced inventory management systems integrate real-time data, enhancing the precision of inventory costing and stock control.

Net Income Fluctuation

Net income fluctuation reflects the variability in a company's profitability over specific accounting periods, influenced by factors such as revenue changes, cost management, and market conditions. Analyzing quarterly financial reports from Fortune 500 companies reveals that industries like technology and retail experience higher net income volatility due to rapid innovation cycles and consumer demand shifts. Effective financial forecasting models incorporate historical earnings data, economic indicators, and operational expenses to predict income stability. Investors and stakeholders closely monitor these fluctuations to assess risk, guide strategic decisions, and evaluate long-term financial health.

Cost Allocation

Cost allocation in business refers to the process of identifying, aggregating, and assigning expenses to various departments, products, or projects to accurately reflect resource consumption. It enables companies to determine the true cost of operations by distributing indirect costs like overhead, utilities, and administrative expenses based on relevant cost drivers. Effective cost allocation supports budgeting, pricing strategies, and financial reporting, ensuring transparency and informed decision-making. Firms commonly use methods such as activity-based costing (ABC) to enhance accuracy and operational efficiency.

Source and External Links

Direct Versus Absorption Costing: One Company's Decision - Absorption costing defers fixed manufacturing costs in inventory until sold, while direct costing treats fixed manufacturing costs as period expenses impacting current profit and management decision-making differently.

What Is Absorption Costing? Definition, Tips and Examples - NetSuite - Absorption costing includes all direct and indirect manufacturing costs (variable and fixed overhead) in product costs, required by GAAP for external reporting and tax purposes.

Direct and Absorption Costing - Studocu - Direct costing (also called variable or marginal costing) considers only variable production costs as product costs, treating fixed production overheads as period costs, while absorption costing includes fixed overheads in product costs.

FAQs

What is direct costing?

Direct costing is a managerial accounting method that assigns only variable manufacturing costs to product costs, treating fixed manufacturing overhead as a period expense.

What is absorption costing?

Absorption costing is an accounting method that includes all manufacturing costs--direct materials, direct labor, and both variable and fixed manufacturing overhead--in the cost of a product.

How do direct costing and absorption costing differ?

Direct costing treats only variable manufacturing costs as product costs, while absorption costing includes both variable and fixed manufacturing costs in product costs.

What are the main components of direct costing?

The main components of direct costing are direct materials, direct labor, and variable manufacturing overhead, while fixed manufacturing overhead is treated as a period expense.

What costs are included in absorption costing?

Absorption costing includes direct materials, direct labor, variable manufacturing overhead, and fixed manufacturing overhead costs.

When is direct costing preferred?

Direct costing is preferred when managerial decisions require clear insight into variable costs for pricing, cost control, and profit analysis.

What are the advantages of absorption costing?

Absorption costing provides a comprehensive view of product costs by including both variable and fixed manufacturing overheads, improves inventory valuation accuracy, complies with GAAP for external reporting, and supports long-term pricing and profitability analysis.