Cash accounting records transactions only when cash changes hands, providing a straightforward view of business liquidity. Accrual accounting recognizes revenues and expenses when they are incurred, offering a more accurate reflection of financial performance over time. Explore the key differences and benefits of each method to determine the best fit for your business needs.

Main Difference

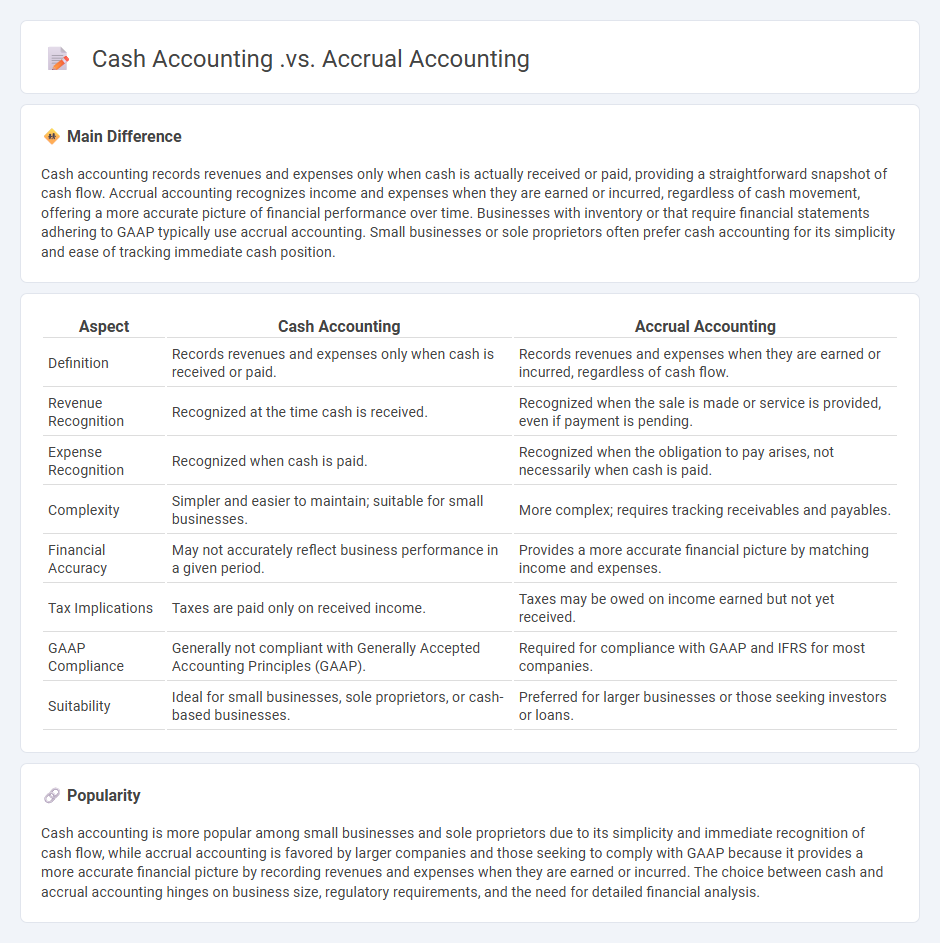

Cash accounting records revenues and expenses only when cash is actually received or paid, providing a straightforward snapshot of cash flow. Accrual accounting recognizes income and expenses when they are earned or incurred, regardless of cash movement, offering a more accurate picture of financial performance over time. Businesses with inventory or that require financial statements adhering to GAAP typically use accrual accounting. Small businesses or sole proprietors often prefer cash accounting for its simplicity and ease of tracking immediate cash position.

Connection

Cash accounting records transactions only when cash is exchanged, reflecting actual cash flow, while accrual accounting recognizes revenues and expenses when they are earned or incurred, providing a more accurate financial picture over time. The connection between the two lies in their impact on financial statements; cash accounting affects cash flow statements directly, whereas accrual accounting influences the income statement and balance sheet by matching income and expenses to the relevant periods. Businesses often reconcile these methods to ensure compliance with accounting standards and to optimize financial reporting accuracy.

Comparison Table

| Aspect | Cash Accounting | Accrual Accounting |

|---|---|---|

| Definition | Records revenues and expenses only when cash is received or paid. | Records revenues and expenses when they are earned or incurred, regardless of cash flow. |

| Revenue Recognition | Recognized at the time cash is received. | Recognized when the sale is made or service is provided, even if payment is pending. |

| Expense Recognition | Recognized when cash is paid. | Recognized when the obligation to pay arises, not necessarily when cash is paid. |

| Complexity | Simpler and easier to maintain; suitable for small businesses. | More complex; requires tracking receivables and payables. |

| Financial Accuracy | May not accurately reflect business performance in a given period. | Provides a more accurate financial picture by matching income and expenses. |

| Tax Implications | Taxes are paid only on received income. | Taxes may be owed on income earned but not yet received. |

| GAAP Compliance | Generally not compliant with Generally Accepted Accounting Principles (GAAP). | Required for compliance with GAAP and IFRS for most companies. |

| Suitability | Ideal for small businesses, sole proprietors, or cash-based businesses. | Preferred for larger businesses or those seeking investors or loans. |

Revenue Recognition

Revenue recognition in business refers to the accounting principle that determines the specific conditions under which income becomes realized as revenue. Companies follow Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) to ensure consistent revenue reporting. This process involves identifying the contract with a customer, determining the transaction price, and recognizing revenue when the performance obligations are satisfied. Accurate revenue recognition is critical for financial reporting, investor confidence, and regulatory compliance.

Expense Matching

Expense matching in business accounting ensures that expenses are recorded in the same period as the revenues they help generate, following the matching principle under GAAP. This practice enhances financial statement accuracy by aligning costs like wages, rent, and depreciation with corresponding income. Proper expense matching improves profitability analysis and aids effective budgeting, tax reporting, and financial decision-making. Companies use accrual accounting methods to implement expense matching consistently for reliable financial performance measurement.

Financial Reporting

Financial reporting in business involves the systematic preparation and presentation of financial statements, including the balance sheet, income statement, and cash flow statement. These reports comply with accounting standards such as GAAP or IFRS to ensure accuracy, transparency, and comparability. Companies use financial reporting to communicate their financial performance and position to stakeholders, including investors, regulators, and management. Effective financial reporting supports better decision-making, regulatory compliance, and improved capital market efficiency.

Tax Implications

Understanding tax implications in business is crucial for optimizing financial performance and compliance. Corporate taxes vary by jurisdiction, often including income tax rates ranging from 15% to 35%, sales tax obligations, and payroll tax responsibilities affecting employee wages. Businesses must also consider tax deductions and credits available for expenses such as research and development, capital investments, and employee benefits to reduce taxable income. Strategic tax planning helps minimize liabilities and ensures adherence to regulations set by authorities like the IRS in the United States or HMRC in the United Kingdom.

Timing of Transactions

Timing of transactions significantly impacts cash flow management and financial reporting accuracy in business operations. Effective scheduling ensures optimal liquidity, enabling companies to meet obligations and invest strategically. Understanding market cycles and seasonal demand enhances transaction timing, improving profitability and competitive advantage. Real-time data analytics further supports precise timing decisions, aligning with business goals and regulatory compliance.

Source and External Links

Understanding Cash vs Accrual Accounting with Examples - Discusses the differences between cash and accrual accounting, highlighting how they record transactions and their suitability for different business types.

Cash Vs. Accrual Accounting: What's the Difference - Explains the main differences between cash accounting (focusing on cash flow) and accrual accounting (tracking revenue and expenses when earned), and their application in various business contexts.

Understanding Cash vs. Accrual Business Accounting - Provides guidance on when to use cash accounting (for simplicity and tax control) versus accrual accounting (for inventory management and financial accuracy).

FAQs

What is cash accounting?

Cash accounting is a method where revenues and expenses are recorded only when cash is actually received or paid.

What is accrual accounting?

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of cash flow timing, providing a more accurate financial position.

How does cash accounting differ from accrual accounting?

Cash accounting records revenues and expenses only when cash is received or paid, while accrual accounting records revenues and expenses when they are earned or incurred, regardless of cash flow.

What are the main advantages of cash accounting?

Cash accounting offers simplicity, immediate tracking of cash flow, easier tax preparation by recording income and expenses only when cash exchanges hands, enhanced visibility of actual cash on hand, and improved management of small business finances.

What are the primary benefits of accrual accounting?

Accrual accounting provides accurate financial position by recognizing revenues and expenses when earned or incurred, improves matching of income and expenses, enhances decision-making through timely financial information, and ensures compliance with GAAP and IFRS standards.

Which types of businesses prefer cash accounting?

Small businesses, sole proprietorships, and service-based businesses often prefer cash accounting due to its simplicity and straightforward cash flow tracking.

Why do some businesses choose accrual accounting?

Some businesses choose accrual accounting to accurately match revenues with expenses, provide a clearer financial picture, comply with Generally Accepted Accounting Principles (GAAP), and improve decision-making by reflecting all earned income and incurred liabilities during a period.