Double entry bookkeeping records every transaction with equal and opposite entries in two accounts, enhancing accuracy and financial tracking for businesses. Single entry bookkeeping logs transactions only once, typically in a cash book, making it simpler but less comprehensive and prone to errors. Explore detailed comparisons to understand which accounting method best suits your financial management needs.

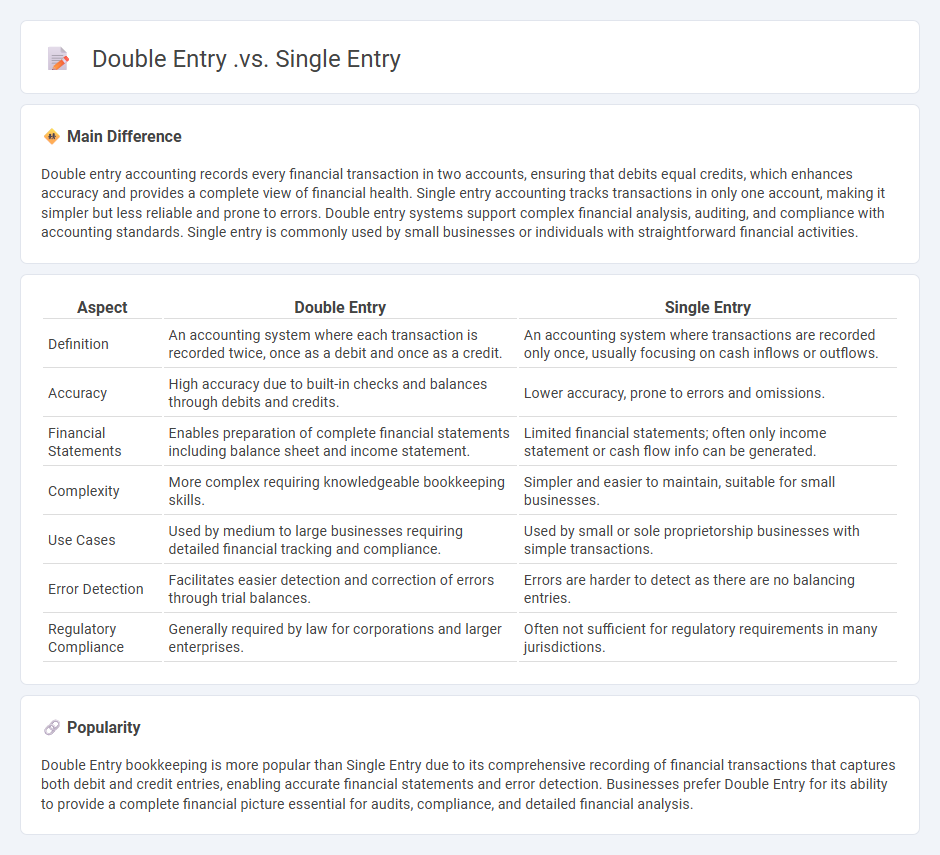

Main Difference

Double entry accounting records every financial transaction in two accounts, ensuring that debits equal credits, which enhances accuracy and provides a complete view of financial health. Single entry accounting tracks transactions in only one account, making it simpler but less reliable and prone to errors. Double entry systems support complex financial analysis, auditing, and compliance with accounting standards. Single entry is commonly used by small businesses or individuals with straightforward financial activities.

Connection

Double entry and single entry bookkeeping are connected through their fundamental role in recording financial transactions, with single entry serving as a simplified form primarily used by small businesses, while double entry provides a more comprehensive system ensuring accuracy by recording every transaction in two accounts: debit and credit. Single entry lacks the internal checks of double entry, which helps detect errors and maintain the accounting equation (Assets = Liabilities + Equity). The connection lies in their shared purpose of tracking financial data, but double entry offers enhanced reliability and financial statement preparation.

Comparison Table

| Aspect | Double Entry | Single Entry |

|---|---|---|

| Definition | An accounting system where each transaction is recorded twice, once as a debit and once as a credit. | An accounting system where transactions are recorded only once, usually focusing on cash inflows or outflows. |

| Accuracy | High accuracy due to built-in checks and balances through debits and credits. | Lower accuracy, prone to errors and omissions. |

| Financial Statements | Enables preparation of complete financial statements including balance sheet and income statement. | Limited financial statements; often only income statement or cash flow info can be generated. |

| Complexity | More complex requiring knowledgeable bookkeeping skills. | Simpler and easier to maintain, suitable for small businesses. |

| Use Cases | Used by medium to large businesses requiring detailed financial tracking and compliance. | Used by small or sole proprietorship businesses with simple transactions. |

| Error Detection | Facilitates easier detection and correction of errors through trial balances. | Errors are harder to detect as there are no balancing entries. |

| Regulatory Compliance | Generally required by law for corporations and larger enterprises. | Often not sufficient for regulatory requirements in many jurisdictions. |

Transaction Recording

Transaction recording in business involves systematically documenting all financial exchanges to ensure accurate accounting and regulatory compliance. Each transaction, such as sales, purchases, receipts, and payments, is recorded in journals and ledgers using double-entry bookkeeping principles. This process supports the creation of financial statements like the income statement and balance sheet, which are essential for internal decision-making and external audits. Effective transaction recording enhances transparency, reduces errors, and facilitates efficient financial management across business operations.

Debit and Credit

Debit and credit are fundamental accounting entries used to record financial transactions in business. Debits increase asset or expense accounts and decrease liabilities or equity, while credits do the opposite by increasing liabilities, equity, or revenue accounts and decreasing assets or expenses. Every business transaction affects at least two accounts, maintaining the accounting equation: Assets = Liabilities + Equity. Accurate use of debits and credits ensures balanced financial statements and reliable bookkeeping.

Ledger Accounts

Ledger accounts in business serve as detailed records that track individual financial transactions within specific categories such as assets, liabilities, equity, revenue, and expenses. Each ledger account captures debit and credit entries to maintain accurate balances, facilitating the preparation of key financial statements like the balance sheet and income statement. Modern accounting software, including QuickBooks and SAP, automates ledger management, increasing accuracy and efficiency. Proper maintenance of ledger accounts is critical for regulatory compliance and informed financial decision-making.

Error Detection

Error detection in business processes enhances operational efficiency by identifying discrepancies and preventing costly mistakes. Advanced techniques such as machine learning algorithms analyze transaction data for anomalies that indicate fraud or systemic errors. Effective error detection systems reduce financial losses and improve compliance with regulatory standards like SOX and GDPR. Continuous monitoring and real-time alerts maintain data integrity across accounting, supply chain, and customer management systems.

Financial Statements

Financial statements are essential documents used in business to provide a comprehensive overview of a company's financial performance and position. They include the balance sheet, income statement, cash flow statement, and statement of shareholders' equity, each offering critical insights into assets, liabilities, revenues, expenses, and cash movements. Accurate financial statements comply with accounting standards such as GAAP or IFRS, ensuring transparency and facilitating informed decision-making by investors, creditors, and management. Regular analysis of these statements helps businesses monitor profitability, liquidity, and financial stability to strategize growth and manage risks effectively.

Source and External Links

Key Differences: Single-Entry Vs Double-Entry - Financfy - Single-entry accounting records each transaction once and is simpler but less accurate, suited for small businesses, while double-entry records every transaction twice (debit and credit), provides greater accuracy, detailed financial reporting, and is suitable for all business sizes especially larger ones.

Single vs. Double Entry Accounting - Modern Treasury - Single-entry accounting records transactions only once and is easy but error-prone and unsuitable for generating full financial statements, whereas double-entry records transactions twice, enables error detection, accurate financial statements, and complies with GAAP standards.

Single Entry VS Double Entry Accounting: A Comprehensive Guide - Single-entry bookkeeping records only cash and personal accounts and lacks automated error detection, while double-entry bookkeeping records all types of accounts, follows standard accounting principles, tracks assets, liabilities, and equity, and provides comprehensive financial information and reports.

FAQs

What is single entry bookkeeping?

Single entry bookkeeping is a simplified accounting method where only one entry is recorded for each financial transaction, typically tracking income and expenses without maintaining detailed accounts like assets or liabilities.

What is double entry bookkeeping?

Double entry bookkeeping is an accounting system where every financial transaction is recorded in at least two accounts, with one debit and one credit of equal value to ensure the accounting equation (Assets = Liabilities + Equity) remains balanced.

How does double entry differ from single entry?

Double entry records every transaction in two accounts with equal debits and credits, ensuring balanced books and accurate financial statements; single entry records transactions only once, typically in a cash book, lacking a complete audit trail or error detection.

What are the advantages of double entry?

Double entry accounting ensures accurate financial records by recording each transaction in two accounts, enhances error detection, improves financial statement reliability, facilitates balance sheet and income statement preparation, and supports comprehensive financial analysis.

What are the limitations of single entry?

The limitations of single entry accounting include lack of double verification, incomplete financial records, inability to track liabilities and assets accurately, difficulty in detecting errors or fraud, and unsuitability for complex businesses requiring detailed financial analysis.

Which businesses use double entry or single entry?

Most large corporations, accounting firms, and publicly traded companies use double-entry accounting for accurate financial tracking and compliance; small businesses, sole proprietors, and freelancers often use single-entry accounting for simplicity.

Why is double entry more reliable?

Double entry is more reliable because it records every transaction in two accounts, ensuring accuracy through automatic cross-verification and reducing errors or fraud.