EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) measures a company's operational profitability by excluding non-cash charges, providing insight into cash flow potential. EBIT (Earnings Before Interest and Taxes) accounts for depreciation and amortization expenses, reflecting operational performance with asset wear and tear considered. Explore the detailed comparison to understand which metric best suits financial analysis.

Main Difference

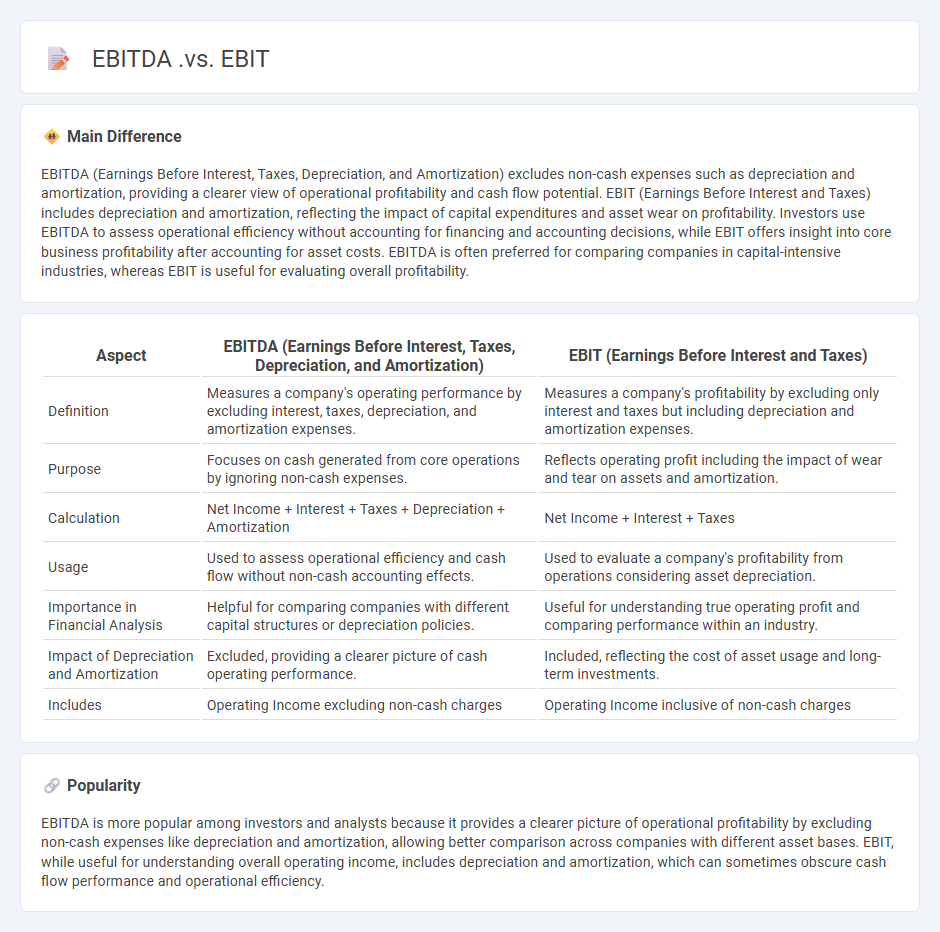

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) excludes non-cash expenses such as depreciation and amortization, providing a clearer view of operational profitability and cash flow potential. EBIT (Earnings Before Interest and Taxes) includes depreciation and amortization, reflecting the impact of capital expenditures and asset wear on profitability. Investors use EBITDA to assess operational efficiency without accounting for financing and accounting decisions, while EBIT offers insight into core business profitability after accounting for asset costs. EBITDA is often preferred for comparing companies in capital-intensive industries, whereas EBIT is useful for evaluating overall profitability.

Connection

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) and EBIT (Earnings Before Interest and Taxes) are connected as they both measure a company's operating performance but differ by the exclusion of non-cash expenses. EBITDA adds back depreciation and amortization to EBIT, providing a clearer view of cash flow from core operations. This connection helps investors assess profitability before accounting for capital expenditures and financial structure.

Comparison Table

| Aspect | EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) | EBIT (Earnings Before Interest and Taxes) |

|---|---|---|

| Definition | Measures a company's operating performance by excluding interest, taxes, depreciation, and amortization expenses. | Measures a company's profitability by excluding only interest and taxes but including depreciation and amortization expenses. |

| Purpose | Focuses on cash generated from core operations by ignoring non-cash expenses. | Reflects operating profit including the impact of wear and tear on assets and amortization. |

| Calculation | Net Income + Interest + Taxes + Depreciation + Amortization | Net Income + Interest + Taxes |

| Usage | Used to assess operational efficiency and cash flow without non-cash accounting effects. | Used to evaluate a company's profitability from operations considering asset depreciation. |

| Importance in Financial Analysis | Helpful for comparing companies with different capital structures or depreciation policies. | Useful for understanding true operating profit and comparing performance within an industry. |

| Impact of Depreciation and Amortization | Excluded, providing a clearer picture of cash operating performance. | Included, reflecting the cost of asset usage and long-term investments. |

| Includes | Operating Income excluding non-cash charges | Operating Income inclusive of non-cash charges |

Operating Income

Operating income measures a company's profitability from core business operations, excluding non-operating revenues and expenses. It is calculated by subtracting operating expenses, such as cost of goods sold (COGS) and selling, general, and administrative expenses (SG&A), from total revenue. This metric provides insight into operational efficiency and is crucial for comparing performance across companies within the same industry. A higher operating income indicates better control over operating costs relative to sales revenue.

Depreciation & Amortization

Depreciation and amortization represent non-cash expenses that allocate the cost of tangible and intangible assets over their useful lives, impacting a company's financial statements. Depreciation typically applies to physical assets like machinery, buildings, and vehicles, while amortization is used for intangible assets such as patents, trademarks, and goodwill. These expenses reduce taxable income and provide a more accurate representation of asset value on the balance sheet. Companies employ methods like straight-line or declining balance to calculate depreciation and amortization, reflecting asset consumption or usage patterns.

Core Profitability

Core profitability measures a company's ability to generate earnings from its primary operations, excluding non-operating income or expenses. It focuses on operating profit or EBIT (Earnings Before Interest and Taxes), providing insight into operational efficiency and sustainable earnings. Analysts often assess core profitability through margins like operating margin or EBITDA margin to evaluate business performance. High core profitability indicates strong management control over costs and revenue generation within the firm's main activities.

Non-Cash Expenses

Non-cash expenses refer to charges recorded in financial statements that do not involve actual cash outflows, such as depreciation and amortization. These expenses allocate the cost of tangible and intangible assets over their useful lives, impacting net income without affecting cash flow. Businesses use non-cash expenses to comply with accounting principles, provide realistic profit representation, and manage taxable income. Understanding non-cash expenses is essential for accurate cash flow analysis and financial decision-making.

Financial Analysis

Financial analysis in business involves evaluating financial statements, such as balance sheets, income statements, and cash flow statements, to assess a company's performance and stability. Key financial ratios like return on equity (ROE), current ratio, and debt-to-equity ratio provide insights into profitability, liquidity, and solvency. Tools such as trend analysis and benchmarking against industry standards help identify growth opportunities and risks. Accurate financial analysis supports strategic decision-making and investor confidence.

Source and External Links

EBIT vs EBITDA - Definition, Example, Template, Use - EBIT is earnings before interest and taxes, while EBITDA is EBIT plus depreciation and amortization, making it earnings before interest, taxes, depreciation, and amortization.

EBIT vs EBITDA: Key Differences & Calculations - The key difference is that EBIT deducts depreciation and amortization from net profit, whereas EBITDA adds them back, focusing on cash earnings before these non-cash charges.

EBIT vs. EBITDA | Comparative Analysis + Differences - EBIT includes depreciation and amortization as operating expenses, while EBITDA excludes these non-cash expenses to provide a clearer view of operational cash flow.

FAQs

What is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization, measuring a company's operational profitability by excluding non-operational expenses and accounting adjustments.

What does EBIT mean?

EBIT stands for Earnings Before Interest and Taxes, representing a company's operating profit excluding interest expenses and tax charges.

How is EBITDA different from EBIT?

EBITDA excludes depreciation and amortization expenses, while EBIT includes them.

Why do companies use EBITDA instead of EBIT?

Companies use EBITDA instead of EBIT to focus on operational performance by excluding non-cash expenses like depreciation and amortization, providing a clearer picture of cash flow and facilitating easier comparisons across firms with different capital structures and asset bases.

What are the limitations of EBITDA and EBIT?

EBITDA excludes depreciation, amortization, interest, and taxes, ignoring capital expenditure, debt costs, and tax impacts, which can distort profitability analysis. EBIT includes depreciation and amortization but ignores tax and interest expenses, limiting its reflection of net profitability and cash flow. Both metrics overlook changes in working capital and non-operating items, affecting comprehensive financial assessment.

Which is better for comparing company performance, EBITDA or EBIT?

EBITDA is better for comparing company performance because it excludes non-cash expenses like depreciation and amortization, providing a clearer view of operational profitability across companies with different capital structures and asset ages.

Can EBITDA and EBIT be negative?

EBITDA and EBIT can be negative if a company's operating expenses and costs exceed its revenue, indicating operating losses.