SWIFT codes and IBANs are essential components in international banking, facilitating secure and accurate cross-border transactions. A SWIFT code identifies specific banks worldwide, while an IBAN standardizes the format for individual bank accounts across countries. Explore the differences and uses of SWIFT codes and IBANs to simplify your global banking experience.

Main Difference

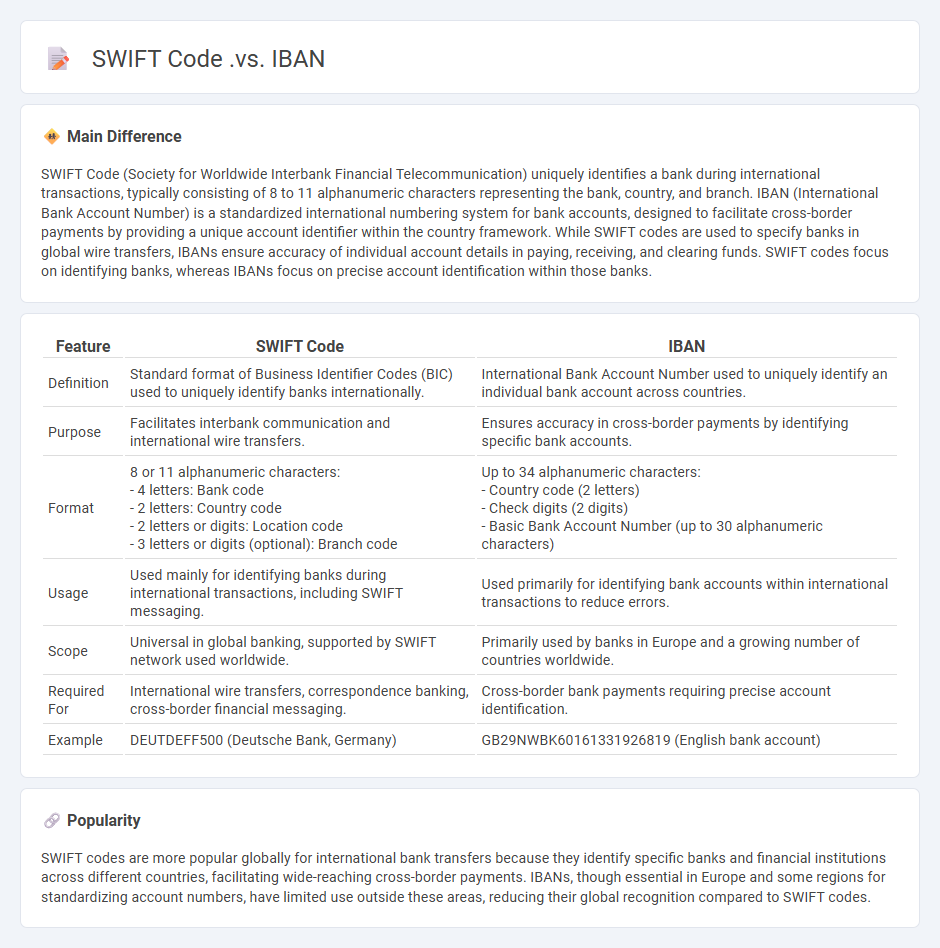

SWIFT Code (Society for Worldwide Interbank Financial Telecommunication) uniquely identifies a bank during international transactions, typically consisting of 8 to 11 alphanumeric characters representing the bank, country, and branch. IBAN (International Bank Account Number) is a standardized international numbering system for bank accounts, designed to facilitate cross-border payments by providing a unique account identifier within the country framework. While SWIFT codes are used to specify banks in global wire transfers, IBANs ensure accuracy of individual account details in paying, receiving, and clearing funds. SWIFT codes focus on identifying banks, whereas IBANs focus on precise account identification within those banks.

Connection

SWIFT codes and IBANs are both essential components in international banking transactions, facilitating accurate and secure cross-border payments. The IBAN (International Bank Account Number) identifies the individual bank account, while the SWIFT code (or BIC) specifies the bank's unique worldwide identity. Together, they ensure funds are routed efficiently from the sender's bank to the recipient's account, minimizing errors and delays.

Comparison Table

| Feature | SWIFT Code | IBAN |

|---|---|---|

| Definition | Standard format of Business Identifier Codes (BIC) used to uniquely identify banks internationally. | International Bank Account Number used to uniquely identify an individual bank account across countries. |

| Purpose | Facilitates interbank communication and international wire transfers. | Ensures accuracy in cross-border payments by identifying specific bank accounts. |

| Format | 8 or 11 alphanumeric characters: - 4 letters: Bank code - 2 letters: Country code - 2 letters or digits: Location code - 3 letters or digits (optional): Branch code |

Up to 34 alphanumeric characters: - Country code (2 letters) - Check digits (2 digits) - Basic Bank Account Number (up to 30 alphanumeric characters) |

| Usage | Used mainly for identifying banks during international transactions, including SWIFT messaging. | Used primarily for identifying bank accounts within international transactions to reduce errors. |

| Scope | Universal in global banking, supported by SWIFT network used worldwide. | Primarily used by banks in Europe and a growing number of countries worldwide. |

| Required For | International wire transfers, correspondence banking, cross-border financial messaging. | Cross-border bank payments requiring precise account identification. |

| Example | DEUTDEFF500 (Deutsche Bank, Germany) | GB29NWBK60161331926819 (English bank account) |

International Bank Account Number (IBAN)

The International Bank Account Number (IBAN) standardizes bank account identification across over 70 countries, facilitating cross-border transactions with improved accuracy and efficiency. It consists of up to 34 alphanumeric characters, including a country code, check digits, and a domestic bank account number, ensuring error detection in international payments. Financial institutions and businesses utilize IBAN to streamline the processing of wire transfers and reduce delays caused by incorrect account details. Compliance with the International Organization for Standardization (ISO 13616) enhances global banking interoperability and regulatory adherence.

Society for Worldwide Interbank Financial Telecommunication (SWIFT) Code

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) code is a unique identifier used by financial institutions worldwide to securely and accurately process international money transfers and payments. Comprising 8 to 11 alphanumeric characters, the SWIFT code encodes the bank code, country code, location code, and optionally a branch code, facilitating precise routing of transactions. SWIFT messaging standardizes financial communication, ensuring interoperability across more than 11,000 banking institutions in over 200 countries. Reliable use of SWIFT codes reduces errors, enhances transaction speed, and supports compliance with global financial regulations.

Cross-Border Transactions

Cross-border transactions involve the exchange of goods, services, or capital across international borders, often requiring compliance with diverse regulatory frameworks such as customs laws, tax policies, and anti-money laundering regulations. Multinational corporations and small businesses alike engage in cross-border trade to expand market reach, optimize supply chains, and leverage cost advantages. Effective management of currency exchange risks and international payment systems is critical to minimizing financial losses and ensuring transaction security. Technological advancements, including blockchain and digital payment platforms, are increasingly facilitating faster, transparent, and more efficient cross-border transactions.

Banking Identification

Banking identification systems utilize secure protocols such as Know Your Customer (KYC) and Anti-Money Laundering (AML) to verify client identities and prevent fraud. These methods often incorporate biometric authentication, two-factor authentication, and digital identity verification tools to enhance security. Financial institutions rely on blockchain technology and encrypted databases to safeguard sensitive customer information against cyber threats. Accurate banking identification improves regulatory compliance and fosters trust in digital banking environments.

Payment Processing

Payment processing in business involves the secure handling of financial transactions between customers and merchants, enabling seamless transfer of funds through various methods such as credit cards, debit cards, and digital wallets. Leading payment processors like PayPal, Stripe, and Square facilitate these transactions by providing robust encryption and fraud detection systems to protect sensitive information. The global payment processing market is projected to reach over $130 billion by 2027, driven by the growth of e-commerce and mobile payments. Efficient payment processing enhances customer experience, reduces cart abandonment rates, and supports cash flow management for businesses of all sizes.

Source and External Links

IBAN vs. SWIFT BIC Code: Are These the Same Thing? - This article explains the differences between IBAN and SWIFT codes, highlighting their roles in identifying bank accounts and financial institutions during international transactions.

SWIFT Vs IBAN: Understanding Their Uses And Limitations - This blog post provides a detailed comparison of IBAN and SWIFT codes, focusing on their definitions, purposes, and usage in international transactions.

IBAN vs SWIFT: Which Do I Need for International Transfers? - This article discusses when to use SWIFT or IBAN codes for international money transfers, offering examples of each and their specific functionalities.

FAQs

What is a SWIFT code?

A SWIFT code is an international bank identifier used for secure and standardized financial transactions, consisting of 8 to 11 characters that specify the bank, country, location, and branch.

What is an IBAN?

An IBAN (International Bank Account Number) is a standardized alphanumeric code used to identify bank accounts internationally, facilitating cross-border transactions and ensuring accurate routing of payments.

What is the difference between a SWIFT code and an IBAN?

A SWIFT code identifies a specific bank globally for international money transfers, while an IBAN provides a standardized format for identifying individual bank accounts within countries to facilitate cross-border payments.

How are SWIFT codes used in international banking?

SWIFT codes uniquely identify banks during international transactions, enabling secure and accurate transfer of funds worldwide.

How do you find your IBAN number?

Find your IBAN number on your bank statement, through your online banking portal, or by contacting your bank directly.

Can you transfer money with only a SWIFT code or only an IBAN?

You cannot transfer money with only a SWIFT code or only an IBAN; both the SWIFT code (for identifying the bank internationally) and the IBAN (for identifying the beneficiary's account) are required for a successful international money transfer.

Why do banks require both SWIFT code and IBAN for overseas transfers?

Banks require both SWIFT code and IBAN for overseas transfers because the SWIFT code identifies the specific bank globally, while the IBAN accurately specifies the individual account within that bank, ensuring precise and secure international payment routing.