Factoring and forfaiting are financial solutions designed to improve cash flow by converting receivables into immediate funds. Factoring typically involves the sale of short-term accounts receivable, often with recourse, to a third party, whereas forfaiting covers medium to long-term receivables without recourse. Explore the key differences and benefits of factoring versus forfaiting to determine the best option for your business needs.

Main Difference

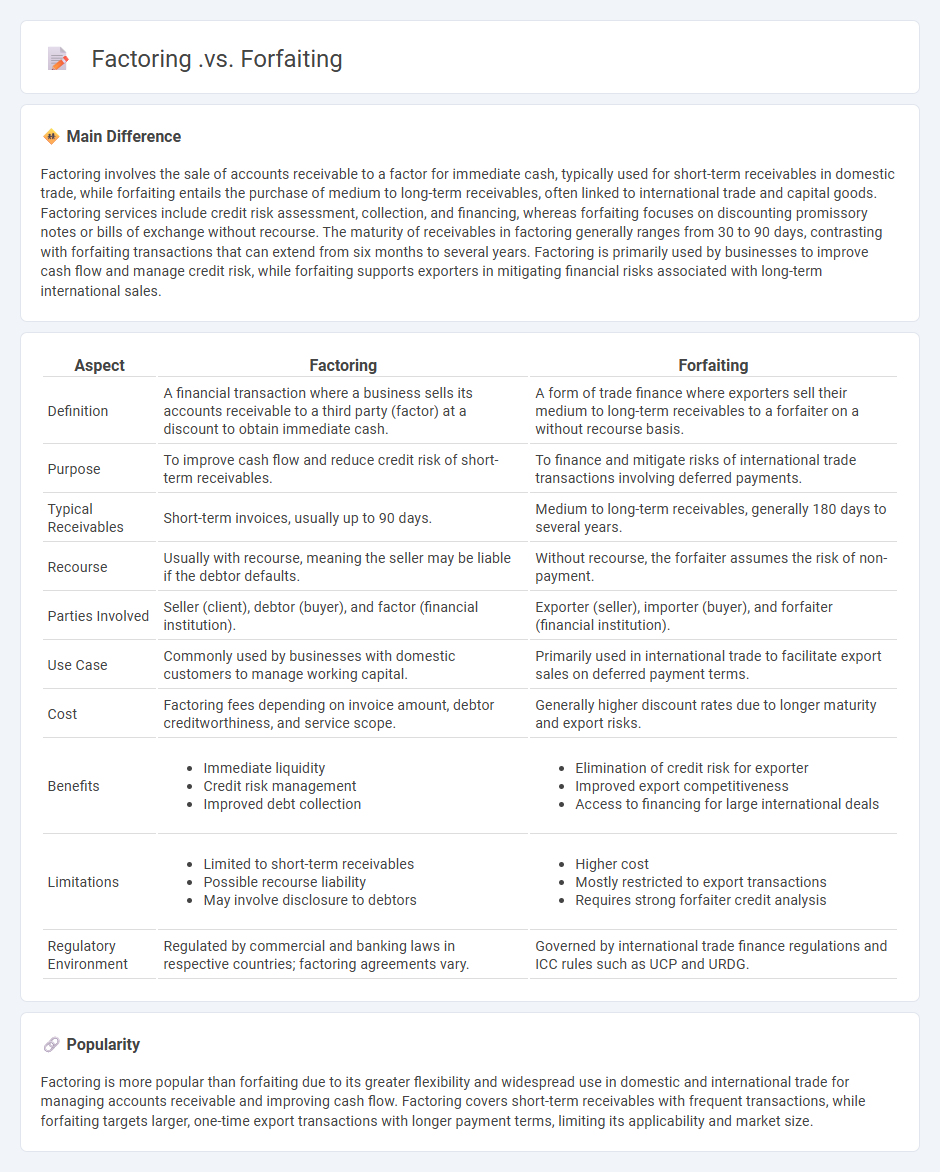

Factoring involves the sale of accounts receivable to a factor for immediate cash, typically used for short-term receivables in domestic trade, while forfaiting entails the purchase of medium to long-term receivables, often linked to international trade and capital goods. Factoring services include credit risk assessment, collection, and financing, whereas forfaiting focuses on discounting promissory notes or bills of exchange without recourse. The maturity of receivables in factoring generally ranges from 30 to 90 days, contrasting with forfaiting transactions that can extend from six months to several years. Factoring is primarily used by businesses to improve cash flow and manage credit risk, while forfaiting supports exporters in mitigating financial risks associated with long-term international sales.

Connection

Factoring and forfaiting both provide businesses with liquidity by converting receivables into immediate cash, yet factoring typically involves short-term accounts receivable, while forfaiting focuses on medium to long-term trade receivables, often related to international transactions. Both financial services help manage credit risk and improve cash flow, leveraging the sale of receivables to specialized financial institutions. Factoring commonly serves domestic markets with ongoing customer relationships, whereas forfaiting is favored for one-time large export deals backed by negotiable instruments like promissory notes or bills of exchange.

Comparison Table

| Aspect | Factoring | Forfaiting |

|---|---|---|

| Definition | A financial transaction where a business sells its accounts receivable to a third party (factor) at a discount to obtain immediate cash. | A form of trade finance where exporters sell their medium to long-term receivables to a forfaiter on a without recourse basis. |

| Purpose | To improve cash flow and reduce credit risk of short-term receivables. | To finance and mitigate risks of international trade transactions involving deferred payments. |

| Typical Receivables | Short-term invoices, usually up to 90 days. | Medium to long-term receivables, generally 180 days to several years. |

| Recourse | Usually with recourse, meaning the seller may be liable if the debtor defaults. | Without recourse, the forfaiter assumes the risk of non-payment. |

| Parties Involved | Seller (client), debtor (buyer), and factor (financial institution). | Exporter (seller), importer (buyer), and forfaiter (financial institution). |

| Use Case | Commonly used by businesses with domestic customers to manage working capital. | Primarily used in international trade to facilitate export sales on deferred payment terms. |

| Cost | Factoring fees depending on invoice amount, debtor creditworthiness, and service scope. | Generally higher discount rates due to longer maturity and export risks. |

| Benefits |

|

|

| Limitations |

|

|

| Regulatory Environment | Regulated by commercial and banking laws in respective countries; factoring agreements vary. | Governed by international trade finance regulations and ICC rules such as UCP and URDG. |

Receivables Financing

Receivables financing enables businesses to improve cash flow by selling or borrowing against outstanding invoices. This financial strategy reduces payment delays, providing immediate working capital to support operations or growth. Companies often leverage factoring or invoice discounting as common methods to unlock liquidity from accounts receivable. Effective receivables management enhances liquidity ratios and strengthens overall financial stability for enterprises.

Risk Transfer

Risk transfer in business involves shifting potential financial losses from one party to another, often through insurance policies, contracts, or hedging strategies. Companies utilize risk transfer to protect assets, stabilize cash flow, and comply with regulatory requirements. Instruments like liability insurance, warranties, and derivatives serve as common tools for mitigating risks such as operational failures, legal liabilities, and market fluctuations. Effective risk transfer enhances organizational resilience by distributing exposure among specialized risk handlers.

Short-term vs Long-term

Short-term business strategies focus on immediate goals such as boosting quarterly revenue, managing cash flow, and addressing operational challenges. Long-term business planning emphasizes sustainable growth, brand development, market expansion, and innovation over several years. Companies investing in research and development, customer loyalty programs, and strategic partnerships often achieve long-term competitive advantage. Balancing short-term performance with long-term vision is essential for financial stability and enduring success.

Recourse vs Non-recourse

Recourse and non-recourse financing represent key distinctions in business loans and credit agreements. Recourse loans require the borrower to be personally liable, meaning the lender can claim the borrower's other assets if the collateral does not cover the debt. Non-recourse loans limit the lender's recovery strictly to the collateral specified in the agreement, protecting the borrower's other assets from claims. Understanding these differences impacts risk management strategies in corporate finance and capital structuring.

Trade Credit Management

Trade credit management plays a crucial role in optimizing cash flow and enhancing business liquidity by regulating credit terms extended to customers. Effective trade credit management reduces the risk of bad debts and ensures timely collections, directly impacting a company's working capital efficiency. Companies often leverage credit analysis tools and risk assessment models to establish appropriate credit limits and payment terms tailored to individual clients. Strong trade credit policies support sustainable business growth and improve supplier relationships within competitive markets.

Source and External Links

Know the Difference between Factoring and Forfaiting - Testbook - Factoring involves selling accounts receivable to a third party, mainly for short-term domestic trade, retaining credit risk, while forfaiting is the outright purchase of medium to long-term trade receivables, transferring credit risk, and is used mainly in international trade.

Forfaiting - what it is and how it differs from factoring - PragmaGO - Factoring can be domestic or international with partial upfront payment and flexible contract durations, while forfaiting applies only to international transactions, paying 100% upfront with higher costs and covering a single receivable per agreement.

Difference between factoring and forfaiting in export finance - Factoring typically finances 80-90% of short-term receivables related to ordinary goods, whereas forfaiting offers full financing of medium to long-term receivables primarily involving capital goods like machinery.

FAQs

What is factoring in finance?

Factoring in finance is a financial transaction where a business sells its accounts receivable (invoices) to a third party (factor) at a discount to improve cash flow and reduce credit risk.

What is forfaiting in trade?

Forfaiting in trade is the purchase of export receivables by a forfaiter at a discount, providing exporters immediate cash flow by eliminating credit risk.

What is the difference between factoring and forfaiting?

Factoring is a financial transaction where a business sells its accounts receivable to a factor at a discount for immediate cash, while forfaiting involves selling medium- to long-term export receivables without recourse to a forfaiter, typically used in international trade finance.

How does factoring work?

Factoring involves expressing a polynomial or number as a product of its factors, simplifying expressions, solving equations, or finding common divisors.

How does forfaiting work?

Forfaiting works by converting export receivables into cash through the purchase of medium to long-term promissory notes or bills of exchange by a forfaiter at a discount, eliminating the exporter's credit risk and accelerating cash flow.

What are the benefits of factoring?

Factoring improves cash flow by converting accounts receivable into immediate funds, reduces credit risk by transferring collection responsibilities to the factor, enhances working capital without incurring debt, and supports business growth by providing quick access to funds.

What are the benefits of forfaiting?

Forfaiting benefits include eliminating credit risk, improving cash flow by converting receivables into immediate cash, providing non-recourse financing, and facilitating international trade by offering flexible payment terms.