Accrual accounting records revenues and expenses when they are earned or incurred, providing a more accurate financial picture by matching income with related expenses. Cash accounting, in contrast, recognizes transactions only when cash is received or paid, offering simplicity but less precise insight into financial health. Explore the differences between accrual and cash accounting to determine which method best suits your business needs.

Main Difference

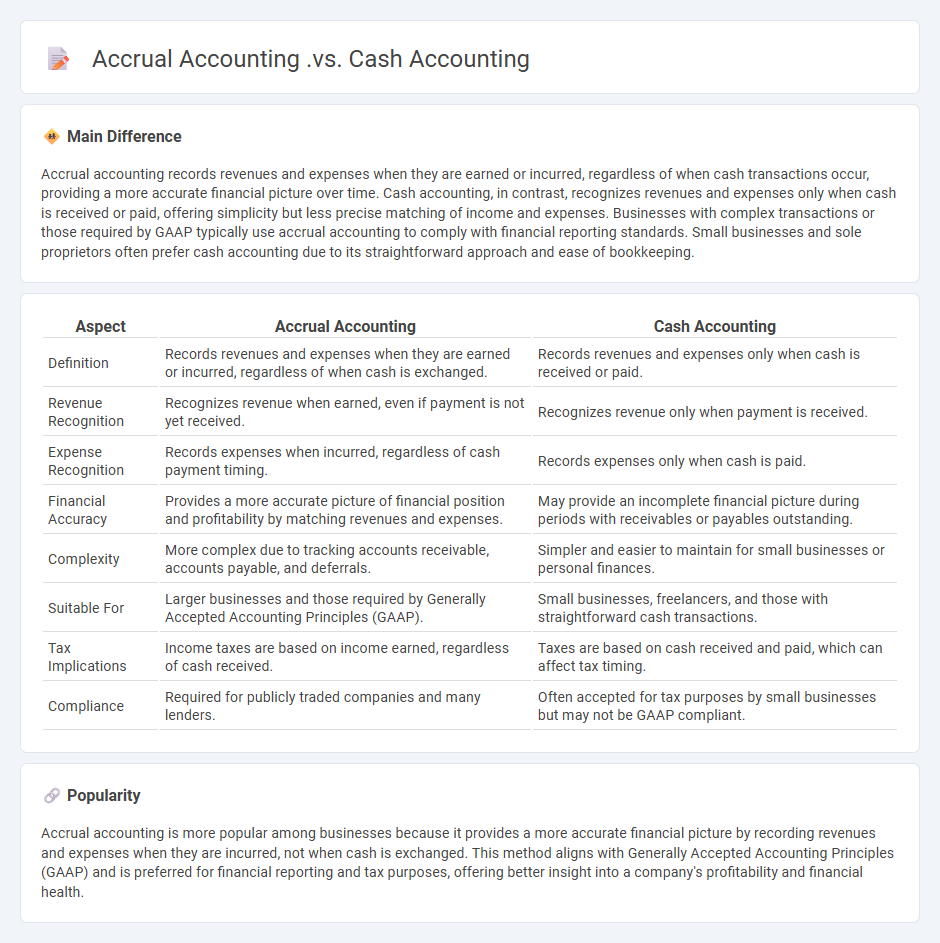

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of when cash transactions occur, providing a more accurate financial picture over time. Cash accounting, in contrast, recognizes revenues and expenses only when cash is received or paid, offering simplicity but less precise matching of income and expenses. Businesses with complex transactions or those required by GAAP typically use accrual accounting to comply with financial reporting standards. Small businesses and sole proprietors often prefer cash accounting due to its straightforward approach and ease of bookkeeping.

Connection

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of cash flow timing, while cash accounting recognizes transactions only when cash is exchanged. Both methods provide distinct financial insights but converge in the overall financial management process by complementing each other for accurate reporting and cash flow analysis. Businesses often use accrual accounting for comprehensive financial statements and cash accounting for managing day-to-day cash flow.

Comparison Table

| Aspect | Accrual Accounting | Cash Accounting |

|---|---|---|

| Definition | Records revenues and expenses when they are earned or incurred, regardless of when cash is exchanged. | Records revenues and expenses only when cash is received or paid. |

| Revenue Recognition | Recognizes revenue when earned, even if payment is not yet received. | Recognizes revenue only when payment is received. |

| Expense Recognition | Records expenses when incurred, regardless of cash payment timing. | Records expenses only when cash is paid. |

| Financial Accuracy | Provides a more accurate picture of financial position and profitability by matching revenues and expenses. | May provide an incomplete financial picture during periods with receivables or payables outstanding. |

| Complexity | More complex due to tracking accounts receivable, accounts payable, and deferrals. | Simpler and easier to maintain for small businesses or personal finances. |

| Suitable For | Larger businesses and those required by Generally Accepted Accounting Principles (GAAP). | Small businesses, freelancers, and those with straightforward cash transactions. |

| Tax Implications | Income taxes are based on income earned, regardless of cash received. | Taxes are based on cash received and paid, which can affect tax timing. |

| Compliance | Required for publicly traded companies and many lenders. | Often accepted for tax purposes by small businesses but may not be GAAP compliant. |

Revenue Recognition

Revenue recognition in business refers to the precise determination of when and how revenue is recorded in financial statements. It follows standards such as the IFRS 15 or ASC 606, which require identifying contract performance obligations and recognizing revenue as these obligations are satisfied. Accurate revenue recognition ensures compliance, reflects true business performance, and impacts financial analysis, investor decisions, and tax reporting. Companies in industries like software, construction, and manufacturing often face complex criteria due to long-term contracts and multiple deliverables.

Expense Matching

Expense matching aligns costs with revenues in the same accounting period to accurately reflect profitability, adhering to the matching principle under Generally Accepted Accounting Principles (GAAP). This practice ensures expenses like salaries, rent, and utilities are recognized when associated revenues are earned, rather than when cash is paid. Accurate expense matching enhances financial statement reliability and supports effective business decision-making and performance evaluation. Companies using accrual accounting typically implement expense matching to comply with regulatory standards and improve financial transparency.

Timing of Transactions

Precise timing of transactions is crucial in business to optimize cash flow and enhance operational efficiency. To maintain liquidity, companies schedule payments and receipts strategically, ensuring obligations are met without incurring penalties or missed discounts. Real-time transaction processing, enabled by technologies like blockchain and payment gateways, accelerates settlement and boosts transparency. Accurate timing also supports financial forecasting and inventory management, reducing risks associated with market volatility.

Financial Reporting Accuracy

Financial reporting accuracy is crucial for maintaining investor trust and regulatory compliance, significantly impacting a company's market valuation. Companies that implement rigorous internal controls and adhere to Generally Accepted Accounting Principles (GAAP) reduce the risk of errors and fraudulent financial statements. According to the U.S. Securities and Exchange Commission, accurate financial disclosures improve transparency and facilitate informed decision-making by stakeholders. Enhanced financial reporting accuracy also supports efficient capital allocation and strengthens overall corporate governance.

Tax Implications

Businesses face various tax implications based on their legal structure, including sole proprietorships, partnerships, corporations, and LLCs, each subject to different tax rates and regulations. Corporate entities are typically subject to corporate income tax, while pass-through entities such as LLCs and S-corporations report income on personal tax returns, avoiding double taxation. Deductions for business expenses, depreciation, and credits significantly impact taxable income and overall tax liability. Staying compliant with IRS guidelines and making use of tax planning strategies can optimize financial outcomes and mitigate risks of penalties.

Source and External Links

Cash Vs. Accrual Accounting: What's the Difference? - Clio - Accrual accounting records income and expenses when they are earned or incurred, regardless of cash movement, while cash accounting records transactions only when cash is received or paid, making accrual better for larger businesses or those with inventory, and cash better for small, cash-based businesses.

Choose between cash and accrual accounting | business.gov.au - Cash accounting tracks actual cash flow with transactions recorded only when money changes hands, whereas accrual accounting records income and expenses at the time they occur, providing a more accurate view of financial position especially for businesses with delayed payments.

Cash vs. Accrual Accounting: Differences Explained - NerdWallet - Accrual accounting matches income and expenses to the period they relate to, regardless of payment timing, providing a clearer profitability picture, while cash basis accounting records transactions based only on when cash is received or paid.

FAQs

What is accrual accounting?

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of cash flow timing, providing a more accurate financial position.

What is cash accounting?

Cash accounting records revenue and expenses only when cash transactions occur, reflecting actual cash flow.

How do accrual and cash accounting differ?

Accrual accounting records revenues and expenses when they are earned or incurred, while cash accounting records them only when cash is received or paid.

What are the advantages of accrual accounting?

Accrual accounting provides accurate financial performance by recognizing revenues and expenses when they occur, improves matching of income and expenses, enhances financial visibility for better decision-making, ensures compliance with GAAP and IFRS standards, and supports more reliable forecasting and budgeting.

What are the disadvantages of cash accounting?

Cash accounting disadvantages include inaccurate financial position during credit transactions, delayed expense recognition affecting profitability analysis, unsuitability for large businesses requiring accrual adjustments, and limited compliance with Generally Accepted Accounting Principles (GAAP).

Which businesses should use accrual accounting?

Businesses with inventories, large accounts receivable or payable, complex financial transactions, or those required by GAAP or IRS regulations should use accrual accounting.

How does each method affect financial statements?

The cash method records revenues and expenses only when cash is exchanged, affecting cash flow statements directly while delaying income and expense recognition on the income statement. The accrual method records revenues when earned and expenses when incurred, matching income and expenses in the same period, thus providing a more accurate representation of profitability on the income statement and affecting accounts receivable, accounts payable, and net income on the balance sheet.