Fixed costs, such as rent and salaries, remain constant regardless of production levels, providing predictable expense management. Variable costs, including raw materials and direct labor, fluctuate directly with the volume of goods or services produced, impacting overall profitability. Explore the key differences between fixed and variable costs to optimize your business budgeting strategies.

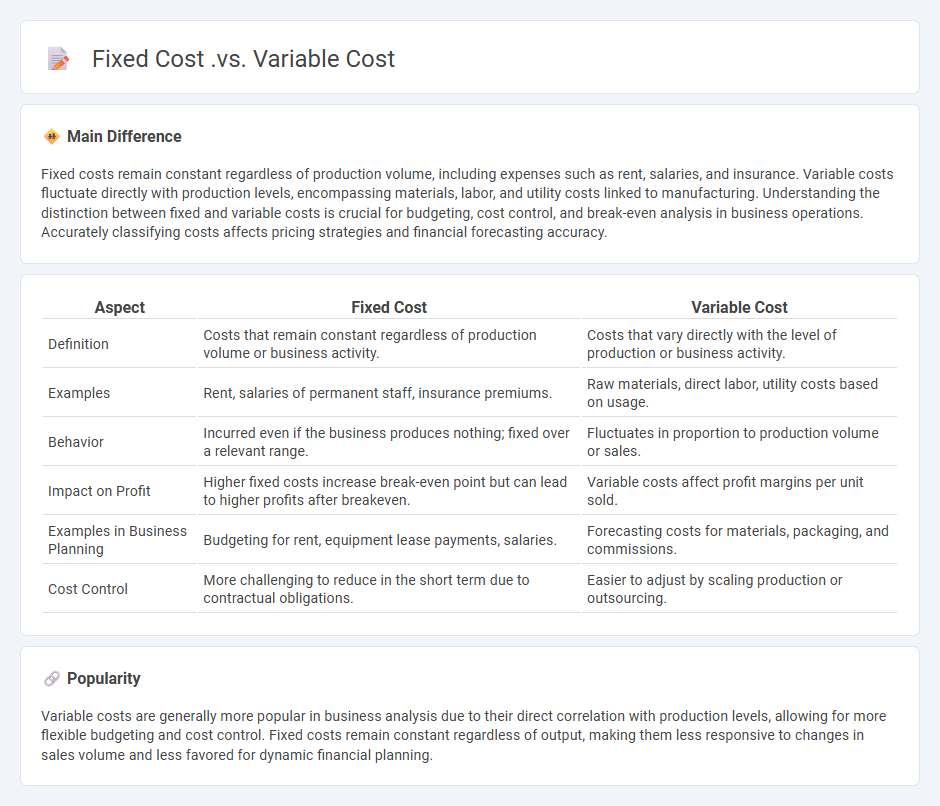

Main Difference

Fixed costs remain constant regardless of production volume, including expenses such as rent, salaries, and insurance. Variable costs fluctuate directly with production levels, encompassing materials, labor, and utility costs linked to manufacturing. Understanding the distinction between fixed and variable costs is crucial for budgeting, cost control, and break-even analysis in business operations. Accurately classifying costs affects pricing strategies and financial forecasting accuracy.

Connection

Fixed cost and variable cost are interconnected components of total production expenses, where fixed costs remain constant regardless of output levels, while variable costs fluctuate with production volume. Understanding their relationship is crucial for calculating the break-even point and optimizing pricing strategies. Accurate cost classification enables better financial forecasting and efficient resource allocation in business operations.

Comparison Table

| Aspect | Fixed Cost | Variable Cost |

|---|---|---|

| Definition | Costs that remain constant regardless of production volume or business activity. | Costs that vary directly with the level of production or business activity. |

| Examples | Rent, salaries of permanent staff, insurance premiums. | Raw materials, direct labor, utility costs based on usage. |

| Behavior | Incurred even if the business produces nothing; fixed over a relevant range. | Fluctuates in proportion to production volume or sales. |

| Impact on Profit | Higher fixed costs increase break-even point but can lead to higher profits after breakeven. | Variable costs affect profit margins per unit sold. |

| Examples in Business Planning | Budgeting for rent, equipment lease payments, salaries. | Forecasting costs for materials, packaging, and commissions. |

| Cost Control | More challenging to reduce in the short term due to contractual obligations. | Easier to adjust by scaling production or outsourcing. |

Fixed Cost

Fixed costs represent business expenses that remain constant regardless of production volume or sales levels, such as rent, salaries, and insurance premiums. These costs must be covered even when the company's output is zero, impacting the overall break-even point. Understanding fixed costs is essential for accurate budgeting, forecasting, and pricing strategies in sectors like manufacturing, retail, and services. According to financial management principles, controlling fixed costs enhances profitability by reducing the total cost base.

Variable Cost

Variable cost in business refers to expenses that fluctuate directly with production volume, such as raw materials, direct labor, and utility costs tied to manufacturing. These costs increase as output rises and decrease when production slows, influencing the overall cost structure and profitability of a company. Understanding variable costs is essential for pricing strategies, budgeting, and profit margin analysis. Firms in industries like manufacturing and retail closely monitor variable costs to optimize operational efficiency and ensure competitive pricing.

Break-even Point

The break-even point in business represents the sales level where total revenues equal total costs, resulting in zero profit. Calculating the break-even point involves fixed costs, variable costs per unit, and the selling price per unit, enabling companies to determine the minimum sales volume required to avoid losses. This metric is crucial for financial planning and decision-making, helping businesses assess profitability and set realistic sales targets. Precise break-even analysis supports cost control and strategic pricing strategies to enhance overall business performance.

Cost Structure

Cost structure in business refers to the categorization and analysis of all expenses involved in operating a company, including fixed costs like rent and salaries, and variable costs such as raw materials and production supplies. Understanding the cost structure is crucial for optimizing profitability, managing budgets, and setting competitive pricing strategies. Common cost structures include fixed costs, variable costs, semi-variable costs, and operating expenses, each impacting cash flow and financial planning differently. Companies often use cost structure analysis to identify cost drivers and implement cost reduction strategies that improve overall efficiency.

Scalability

Scalability in business refers to a company's ability to grow and manage increased demand without compromising performance or losing revenue potential. Scalable businesses efficiently expand operations by leveraging technology, optimizing processes, and increasing production capacity while maintaining cost-effectiveness. Key indicators of scalability include sustainable profit margins, flexible infrastructure, and adaptable workforce management. Companies like Amazon and Uber exemplify scalable business models, rapidly adjusting to market changes and customer needs.

Source and External Links

Fixed vs. Variable Costs: What's the Difference - Fixed costs, like rent and salaries, stay constant regardless of production volume, while variable costs, such as raw materials and commission, change directly with output.

Fixed cost vs Variable Cost: Examples - Fixed costs remain unchanged with production levels, but their per-unit cost decreases as output rises, whereas variable costs fluctuate with each additional unit produced.

Fixed and Variable Costs - Regardless of how much a business produces, fixed costs do not vary, while variable costs show a direct, linear relationship with the volume of production.

FAQs

What is a fixed cost?

A fixed cost is a business expense that remains constant regardless of production or sales volume, such as rent, salaries, and insurance.

What is a variable cost?

A variable cost is an expense that changes in direct proportion to the level of production or sales volume, such as raw materials and direct labor.

How do fixed and variable costs differ in business operations?

Fixed costs remain constant regardless of production levels, while variable costs change directly with the volume of goods or services produced.

What are common examples of fixed costs?

Common examples of fixed costs include rent, salaries, insurance premiums, property taxes, and depreciation expenses.

What are typical examples of variable costs?

Typical examples of variable costs include raw materials, direct labor, sales commissions, and utility expenses that fluctuate with production volume.

How do fixed and variable costs impact pricing strategies?

Fixed costs set a baseline for pricing to ensure profitability, while variable costs influence price adjustments based on production volume and market demand.

Why is understanding fixed and variable costs important for financial planning?

Understanding fixed and variable costs is important for financial planning because it enables accurate budgeting, cost control, and profit forecasting by distinguishing between consistent expenses and those that fluctuate with production levels.