Intangible assets include non-physical resources such as patents, trademarks, and goodwill, while tangible assets consist of physical items like machinery, buildings, and inventory. Both asset types hold significant value on a company's balance sheet and influence financial analysis and investment decisions. Explore the key differences and implications of intangible assets versus tangible assets to enhance your understanding.

Main Difference

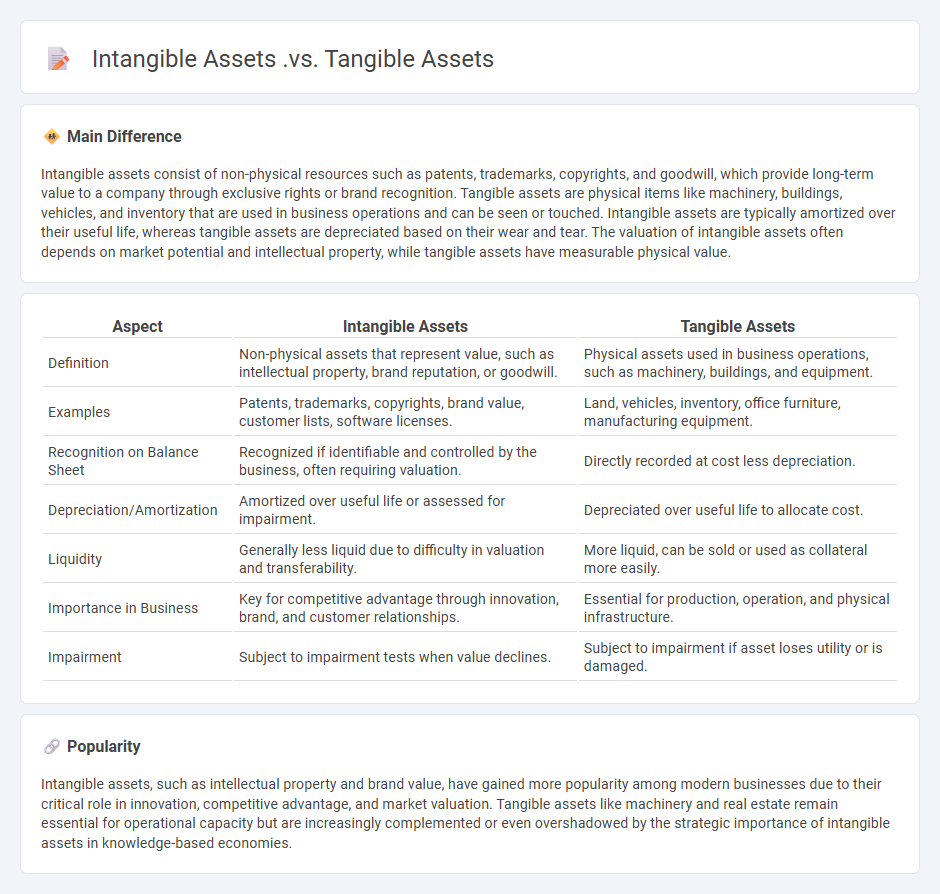

Intangible assets consist of non-physical resources such as patents, trademarks, copyrights, and goodwill, which provide long-term value to a company through exclusive rights or brand recognition. Tangible assets are physical items like machinery, buildings, vehicles, and inventory that are used in business operations and can be seen or touched. Intangible assets are typically amortized over their useful life, whereas tangible assets are depreciated based on their wear and tear. The valuation of intangible assets often depends on market potential and intellectual property, while tangible assets have measurable physical value.

Connection

Intangible assets like patents, trademarks, and goodwill complement tangible assets such as machinery, buildings, and inventory by enhancing overall business value and competitive advantage. Effective management of both asset types drives innovation, operational efficiency, and brand recognition, contributing to sustained financial performance. Integration of intangible and tangible assets is critical for accurate company valuation and strategic investment decisions.

Comparison Table

| Aspect | Intangible Assets | Tangible Assets |

|---|---|---|

| Definition | Non-physical assets that represent value, such as intellectual property, brand reputation, or goodwill. | Physical assets used in business operations, such as machinery, buildings, and equipment. |

| Examples | Patents, trademarks, copyrights, brand value, customer lists, software licenses. | Land, vehicles, inventory, office furniture, manufacturing equipment. |

| Recognition on Balance Sheet | Recognized if identifiable and controlled by the business, often requiring valuation. | Directly recorded at cost less depreciation. |

| Depreciation/Amortization | Amortized over useful life or assessed for impairment. | Depreciated over useful life to allocate cost. |

| Liquidity | Generally less liquid due to difficulty in valuation and transferability. | More liquid, can be sold or used as collateral more easily. |

| Importance in Business | Key for competitive advantage through innovation, brand, and customer relationships. | Essential for production, operation, and physical infrastructure. |

| Impairment | Subject to impairment tests when value declines. | Subject to impairment if asset loses utility or is damaged. |

Physical Presence

Physical presence in business refers to having a tangible location where operations occur, such as offices, stores, or warehouses. It enables direct customer interaction, supports local market penetration, and fosters community trust. Companies with physical locations often see improved brand recognition and logistical advantages. Incorporating physical presence complements digital strategies, enhancing overall business effectiveness.

Valuation Methods

Valuation methods in business are essential for determining the economic value of a company or its assets. Common approaches include discounted cash flow (DCF), comparable company analysis (CCA), and precedent transactions, each offering unique insights based on cash flow projections, market multiples, or historical deal prices. DCF focuses on forecasting free cash flows and discounting them to present value using the weighted average cost of capital (WACC). Comparable company analysis evaluates trading multiples such as EV/EBITDA or P/E ratios against peer firms to estimate relative value accurately.

Depreciation vs. Amortization

Depreciation allocates the cost of tangible assets like machinery, vehicles, and buildings over their useful life to reflect wear and tear. Amortization applies to intangible assets such as patents, trademarks, and goodwill, systematically reducing their book value over time. Both methods are essential for accurate financial reporting, tax deductions, and assessing asset value on balance sheets. Companies typically use straight-line depreciation and amortization methods for consistent expense recognition.

Intellectual Property

Intellectual property in business encompasses patents, trademarks, copyrights, and trade secrets that protect innovations, brand identity, and creative works. Companies invest heavily in securing these rights to maintain competitive advantage, foster innovation, and generate revenue through licensing or sales. Effective IP management mitigates risks of infringement lawsuits and safeguards proprietary technology essential for market differentiation. Global frameworks such as the World Intellectual Property Organization (WIPO) facilitate cross-border protection for businesses operating internationally.

Financial Reporting

Financial reporting in business involves the systematic preparation and presentation of financial statements, including the balance sheet, income statement, and cash flow statement, to provide stakeholders with accurate insights into a company's financial performance. Regulatory frameworks such as the Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) ensure consistency, reliability, and transparency in financial disclosures. Companies leverage financial reporting to comply with statutory requirements and assist investors, creditors, and management in making informed decisions. The Securities and Exchange Commission (SEC) mandates periodic filings like 10-K and 10-Q reports for publicly traded companies in the United States.

Source and External Links

Tangible vs. Intangible Assets | What's the Difference? - Tangible assets are physical items (like cash, land, equipment), while intangible assets are non-physical (like patents, trademarks, copyrights).

What are tangible and intangible assets? | BDC.ca - Tangible assets have physical substance (e.g., inventory, buildings, machinery), whereas intangible assets cannot be seen or touched (e.g., patents, goodwill).

5 Differences Between Tangible and Intangible Assets - CFO Hub - Tangible assets (buildings, inventory, machines) carry physical value and are often less liquid, while intangible assets (brand recognition, intellectual property, patents) have no physical form but can be extremely valuable to a company.

FAQs

What are assets in business?

Assets in business are resources owned or controlled by a company that have economic value and can generate future benefits.

What is the difference between tangible and intangible assets?

Tangible assets are physical items like machinery, buildings, and inventory, while intangible assets include non-physical resources such as patents, trademarks, copyrights, and goodwill.

What are examples of intangible assets?

Examples of intangible assets include patents, trademarks, copyrights, goodwill, brand recognition, and customer lists.

What are examples of tangible assets?

Examples of tangible assets include machinery, buildings, vehicles, inventory, land, and equipment.

How are intangible assets valued?

Intangible assets are valued using methods like the income approach, cost approach, and market approach, focusing on expected future cash flows, replacement cost, or comparable market transactions.

How are tangible assets recorded on the balance sheet?

Tangible assets are recorded on the balance sheet at their historical cost minus accumulated depreciation.

Why are intangible assets important for a company?

Intangible assets like patents, trademarks, and goodwill enhance a company's competitive advantage, increase market value, and generate long-term revenue streams.