LIFO (Last In, First Out) and FIFO (First In, First Out) are two fundamental inventory valuation methods used in accounting and supply chain management. LIFO assumes the most recently acquired items are sold first, often leading to lower taxable income during inflationary periods, while FIFO assumes the oldest inventory is sold first, typically reflecting higher net income. Explore the detailed differences and implications of LIFO and FIFO for better financial decision-making.

Main Difference

LIFO (Last In, First Out) inventory accounting method assumes the most recently acquired items are sold first, which can reduce taxable income during inflationary periods. FIFO (First In, First Out) assumes the oldest inventory is sold first, often resulting in higher reported profits when prices rise. LIFO better matches current costs with revenues, while FIFO provides a more accurate valuation of ending inventory on the balance sheet. Businesses choose between LIFO and FIFO based on tax strategy, financial reporting goals, and industry practices.

Connection

LIFO (Last In, First Out) and FIFO (First In, First Out) are inventory valuation methods that impact cost of goods sold and ending inventory differently. LIFO assumes the most recent inventory items are sold first, often matching current costs with current revenues, while FIFO assumes the oldest inventory is sold first, reflecting older costs in cost of goods sold. Businesses choose between LIFO and FIFO based on tax implications, financial reporting, and inventory management strategies.

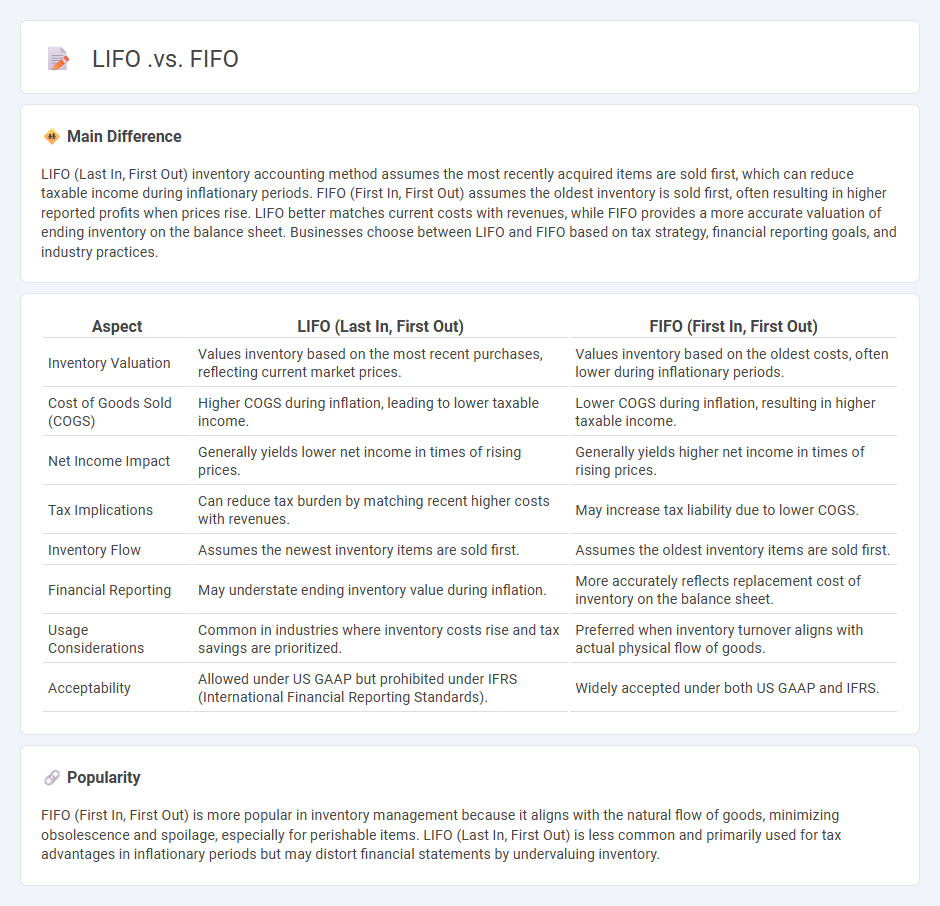

Comparison Table

| Aspect | LIFO (Last In, First Out) | FIFO (First In, First Out) |

|---|---|---|

| Inventory Valuation | Values inventory based on the most recent purchases, reflecting current market prices. | Values inventory based on the oldest costs, often lower during inflationary periods. |

| Cost of Goods Sold (COGS) | Higher COGS during inflation, leading to lower taxable income. | Lower COGS during inflation, resulting in higher taxable income. |

| Net Income Impact | Generally yields lower net income in times of rising prices. | Generally yields higher net income in times of rising prices. |

| Tax Implications | Can reduce tax burden by matching recent higher costs with revenues. | May increase tax liability due to lower COGS. |

| Inventory Flow | Assumes the newest inventory items are sold first. | Assumes the oldest inventory items are sold first. |

| Financial Reporting | May understate ending inventory value during inflation. | More accurately reflects replacement cost of inventory on the balance sheet. |

| Usage Considerations | Common in industries where inventory costs rise and tax savings are prioritized. | Preferred when inventory turnover aligns with actual physical flow of goods. |

| Acceptability | Allowed under US GAAP but prohibited under IFRS (International Financial Reporting Standards). | Widely accepted under both US GAAP and IFRS. |

Inventory Valuation

Inventory valuation determines the cost assigned to goods in stock, directly impacting a company's balance sheet and profit margins. Common methods include First-In, First-Out (FIFO), Last-In, First-Out (LIFO), and Weighted Average Cost, each affecting tax liabilities and financial reporting differently. Accurate inventory valuation supports effective inventory management, cash flow forecasting, and compliance with accounting standards such as GAAP or IFRS. Businesses often use software systems like ERP tools to automate inventory valuation processes and enhance accuracy.

Cost Flow Assumptions

Cost flow assumptions in business accounting determine how costs are assigned to inventory and cost of goods sold, impacting financial statements and tax liabilities. The primary methods include First-In, First-Out (FIFO), Last-In, First-Out (LIFO), and Weighted Average Cost, each affecting profit margins and inventory valuation differently. FIFO assumes the earliest costs are sold first, often resulting in higher net income during inflation periods, while LIFO assumes the latest costs are sold first, lowering taxable income when prices rise. Weighted Average Cost smooths cost fluctuations by averaging all inventory costs, offering a balanced approach for cost allocation.

Tax Implications

Business tax implications vary based on entity type, revenue, and jurisdiction. Corporations face corporate income tax rates ranging from 21% federally in the United States, while pass-through entities like S corporations and LLCs report income on individual tax returns, subject to personal income tax brackets. Sales tax, payroll tax, and self-employment tax also affect businesses, with compliance mandates depending on state and local laws. Proper tax planning and consulting with a CPA can optimize deductions and credits, reducing overall tax liability.

Gross Profit Margin

Gross Profit Margin measures the percentage of revenue that exceeds the cost of goods sold (COGS), indicating a company's efficiency in producing goods or services. It is calculated as (Revenue - COGS) / Revenue, expressed as a percentage. Industries such as retail and manufacturing typically aim for gross profit margins between 20% and 50%, depending on competition and cost structures. Monitoring this metric helps businesses assess pricing strategies, cost control, and overall profitability.

Financial Reporting

Financial reporting in business involves the systematic process of preparing and presenting accurate financial statements, including balance sheets, income statements, and cash flow statements. These reports comply with accounting standards such as GAAP or IFRS to ensure transparency and comparability for stakeholders. Effective financial reporting supports strategic decision-making, regulatory compliance, and investor confidence by providing a clear view of a company's financial health and operational performance. Advanced technologies like AI and blockchain are increasingly integrated to enhance accuracy, reduce fraud, and streamline report generation.

Source and External Links

FIFO vs LIFO: Comparing Inventory Valuation Methods - FreshBooks - FIFO sells older inventory first leading to higher inventory value and reported income but higher taxes, while LIFO sells newer inventory first resulting in lower inventory value and taxable income, offering tax benefits but possibly less accurate inventory reflection.

FIFO vs. LIFO: Difference Between Inventory Methods - Lightspeed - FIFO aligns with natural inventory flow and typically shows higher profits and inventory value, accepted under both GAAP and IFRS; LIFO matches recent costs with revenues and lowers taxable income during inflation but is only allowed under U.S. GAAP and can lower reported profits and inventory value.

FIFO vs LIFO: What Are They and When to Use Them -- Katana - FIFO offers more accurate cost portrayal and easier management, best when prices rise, while LIFO provides better cost matching in inflation but is harder to manage, may lead to stock issues, and is limited to US usage only.

FAQs

What do LIFO and FIFO mean in inventory management?

LIFO (Last In, First Out) means the most recently acquired inventory is sold or used first; FIFO (First In, First Out) means the oldest inventory is sold or used first.

How does LIFO differ from FIFO?

LIFO (Last In, First Out) inventory method assumes the most recently acquired items are sold first, while FIFO (First In, First Out) assumes the oldest items are sold first.

Which method results in higher taxable income?

The straight-line depreciation method results in higher taxable income compared to the accelerated depreciation method.

How do LIFO and FIFO affect financial statements?

LIFO decreases net income and ending inventory during rising prices by increasing cost of goods sold, lowering taxable income, while FIFO increases net income and ending inventory by matching older, lower costs with current revenues, resulting in higher reported profits.

Which industries prefer LIFO or FIFO?

Retail and manufacturing industries often prefer FIFO for accurate inventory valuation and matching current costs with revenues. Oil, gas, and chemical industries frequently use LIFO to minimize tax liabilities during inflationary periods.

What are the advantages of using FIFO over LIFO?

FIFO provides more accurate inventory valuation during periods of rising prices, results in higher net income, reduces the risk of inventory obsolescence by selling older stock first, and improves cash flow management by aligning cost of goods sold with current market costs.

How does inventory flow impact cost of goods sold?

Inventory flow affects cost of goods sold by determining which inventory costs are matched with sales, influencing reported expenses and profitability.