Securitization transforms illiquid assets into tradable securities, enabling lenders to free up capital and distribute risk among investors. Syndication involves multiple lenders jointly providing a loan to a single borrower, sharing the credit exposure and funding requirements. Explore the key differences and benefits of securitization and syndication to enhance your financial strategy.

Main Difference

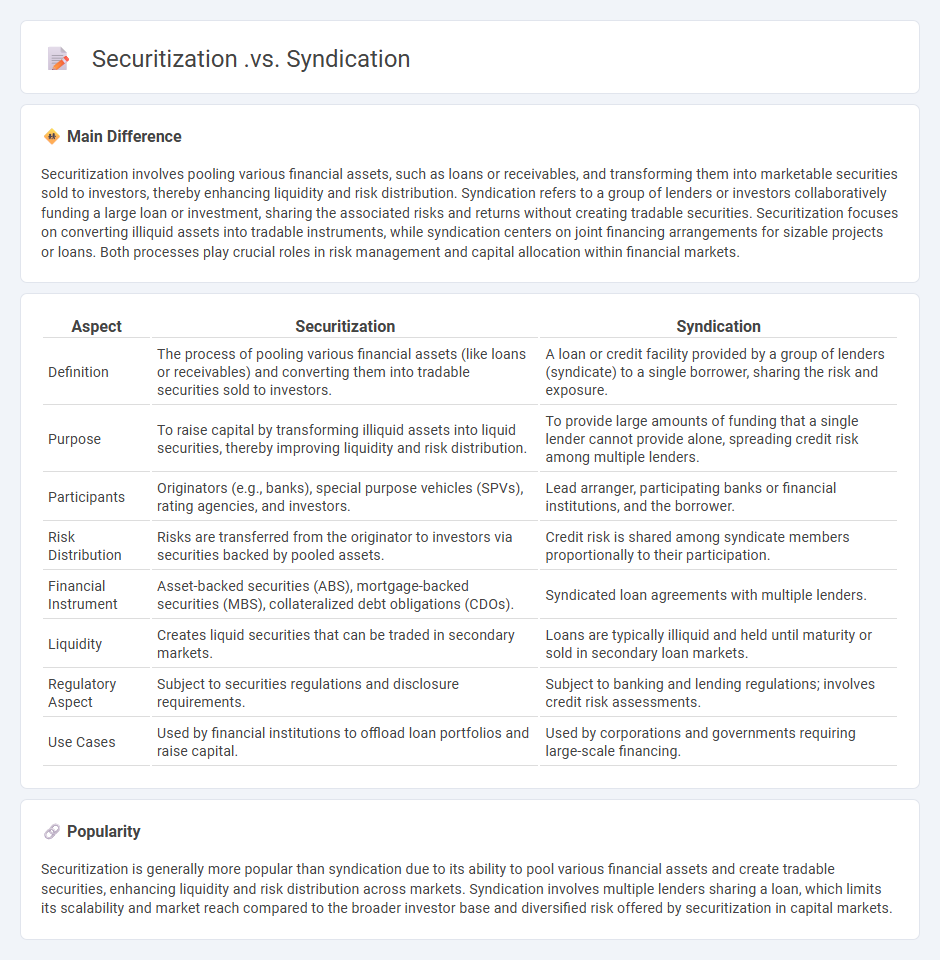

Securitization involves pooling various financial assets, such as loans or receivables, and transforming them into marketable securities sold to investors, thereby enhancing liquidity and risk distribution. Syndication refers to a group of lenders or investors collaboratively funding a large loan or investment, sharing the associated risks and returns without creating tradable securities. Securitization focuses on converting illiquid assets into tradable instruments, while syndication centers on joint financing arrangements for sizable projects or loans. Both processes play crucial roles in risk management and capital allocation within financial markets.

Connection

Securitization transforms financial assets into marketable securities, enabling investors to buy interest in pooled loans, while syndication involves multiple lenders jointly financing a single large loan to share risk. Both processes distribute financial risk and increase capital access by dividing exposure among multiple parties. Banks often use syndication to originate loans that can later be securitized for broader investor participation.

Comparison Table

| Aspect | Securitization | Syndication |

|---|---|---|

| Definition | The process of pooling various financial assets (like loans or receivables) and converting them into tradable securities sold to investors. | A loan or credit facility provided by a group of lenders (syndicate) to a single borrower, sharing the risk and exposure. |

| Purpose | To raise capital by transforming illiquid assets into liquid securities, thereby improving liquidity and risk distribution. | To provide large amounts of funding that a single lender cannot provide alone, spreading credit risk among multiple lenders. |

| Participants | Originators (e.g., banks), special purpose vehicles (SPVs), rating agencies, and investors. | Lead arranger, participating banks or financial institutions, and the borrower. |

| Risk Distribution | Risks are transferred from the originator to investors via securities backed by pooled assets. | Credit risk is shared among syndicate members proportionally to their participation. |

| Financial Instrument | Asset-backed securities (ABS), mortgage-backed securities (MBS), collateralized debt obligations (CDOs). | Syndicated loan agreements with multiple lenders. |

| Liquidity | Creates liquid securities that can be traded in secondary markets. | Loans are typically illiquid and held until maturity or sold in secondary loan markets. |

| Regulatory Aspect | Subject to securities regulations and disclosure requirements. | Subject to banking and lending regulations; involves credit risk assessments. |

| Use Cases | Used by financial institutions to offload loan portfolios and raise capital. | Used by corporations and governments requiring large-scale financing. |

Asset Pooling

Asset pooling in business involves combining multiple assets from different investors into a single, diversified investment portfolio. This strategy enhances risk management by spreading exposure across various asset classes such as stocks, bonds, and real estate. Institutional investors like pension funds and mutual funds commonly use asset pooling to achieve economies of scale, reduce transaction costs, and improve portfolio returns. Effective asset pooling leverages advanced analytics and portfolio management software to optimize asset allocation and performance.

Risk Transfer

Risk transfer in business involves shifting potential financial losses from one party to another, often through insurance policies or contractual agreements. Companies commonly utilize risk transfer mechanisms such as liability insurance, surety bonds, and outsourcing to mitigate exposure to operational and legal risks. Effective risk transfer enables businesses to stabilize cash flow, protect assets, and enhance strategic planning by minimizing unexpected costs. This approach supports overall risk management frameworks by allocating risk to entities better equipped to handle specific uncertainties.

Tranche Structure

Tranche structure in business refers to dividing financial instruments, such as loans or securities, into multiple segments with varying risk levels, maturities, and returns. This approach allows investors to select tranches aligned with their risk tolerance and investment goals. Commonly utilized in structured finance products like collateralized debt obligations (CDOs) and mortgage-backed securities (MBS), tranche structuring enhances capital efficiency and risk distribution. Each tranche carries specific credit ratings, influencing pricing and investor demand in capital markets.

Investor Participation

Investor participation in business significantly enhances capital infusion, driving growth and innovation across sectors. Active investors contribute strategic guidance, industry expertise, and governance oversight, elevating company performance and market competitiveness. Data from the National Bureau of Economic Research indicates firms with engaged investors exhibit a 20% higher return on assets compared to those with passive stakeholders. Enhanced shareholder involvement also facilitates improved risk management and long-term value creation.

Origination Process

The origination process in business involves the steps taken to initiate and establish a loan or credit agreement, starting from the loan application to approval and funding. It includes screening potential borrowers, verifying financial documents, assessing creditworthiness using criteria such as credit scores and income verification, and complying with regulatory requirements. Efficient origination processes leverage automated underwriting systems to reduce processing time and errors. Major financial institutions like JPMorgan Chase and Wells Fargo utilize advanced data analytics to optimize origination workflows and increase loan approval accuracy.

Source and External Links

Answer for Hi Gurus, Can you explain the difference between Syndication and Securitization and how is this concept used in the leasing industry? - Securitization involves pooling financial assets and creating tradable securities from them to promote liquidity, while syndication involves multiple lenders jointly providing portions of a single loan or lease, allowing shared risk exposure.

The Syndicate Structure of Securitized Corporate Loans - Securitized loans are syndicated loans financed by multiple banks and investors, combining characteristics of both securitization and syndication, with lead banks holding varying shares depending on securitization status.

Understanding Securitized Products - PIMCO - Securitization pools similar loans to issue bonds through a trust structure, enabling originators to remove loans from balance sheets and investors to buy slices of loan pools, unlike syndication which involves shared direct financing of a specific loan.

FAQs

What is securitization?

Securitization is the financial process of pooling various types of debt--such as mortgages, auto loans, or credit card receivables--and converting them into tradable securities to raise capital.

What is syndication in finance?

Syndication in finance is the process where multiple lenders or investors collaborate to fund a single large loan or investment, sharing risks and returns.

How do securitization and syndication differ?

Securitization transforms financial assets into marketable securities sold to investors, while syndication involves multiple lenders jointly providing a large loan to a single borrower.

What assets are commonly securitized?

Commonly securitized assets include mortgages, auto loans, credit card receivables, student loans, commercial loans, and equipment leases.

What are the main steps in a syndication process?

The main steps in a syndication process are originator selection, loan underwriting, syndicate formation, document preparation, distribution to investors, and loan administration.

What are the benefits of securitization versus syndication?

Securitization offers benefits such as improved liquidity, risk transfer to investors, diversification of funding sources, and off-balance-sheet financing, while syndication primarily enables risk sharing among lenders, larger loan capacity, and relationship management with borrowers.

What risks are associated with both securitization and syndication?

Securitization risks include credit risk, liquidity risk, and regulatory risk; syndication risks involve credit risk, coordination risk, and reputational risk.