Transfer pricing determines the prices for transactions between related entities within a multinational company, affecting tax liabilities and profit allocation. Arms-length pricing ensures these transactions reflect market conditions as if conducted between independent parties, complying with tax regulations to prevent profit shifting. Explore further to understand the nuances and regulatory implications of both pricing methods.

Main Difference

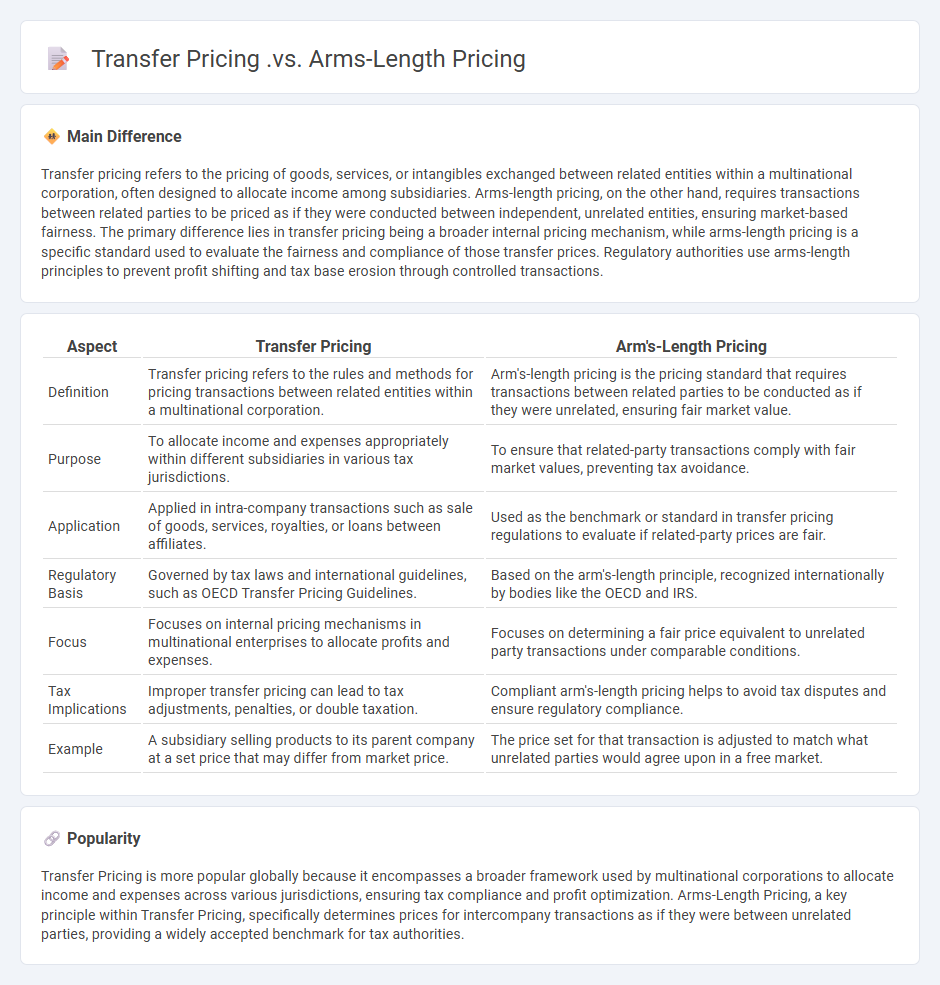

Transfer pricing refers to the pricing of goods, services, or intangibles exchanged between related entities within a multinational corporation, often designed to allocate income among subsidiaries. Arms-length pricing, on the other hand, requires transactions between related parties to be priced as if they were conducted between independent, unrelated entities, ensuring market-based fairness. The primary difference lies in transfer pricing being a broader internal pricing mechanism, while arms-length pricing is a specific standard used to evaluate the fairness and compliance of those transfer prices. Regulatory authorities use arms-length principles to prevent profit shifting and tax base erosion through controlled transactions.

Connection

Transfer pricing and arm's-length pricing are fundamentally connected as transfer pricing relies on the arm's-length principle to set prices between related entities in multinational corporations. The arm's-length pricing ensures that transactions between affiliated companies reflect market conditions as if the parties were unrelated, thereby preventing profit shifting and tax evasion. Compliance with arm's-length standards is essential for accurate transfer pricing documentation and aligns with guidelines established by the OECD and local tax authorities.

Comparison Table

| Aspect | Transfer Pricing | Arm's-Length Pricing |

|---|---|---|

| Definition | Transfer pricing refers to the rules and methods for pricing transactions between related entities within a multinational corporation. | Arm's-length pricing is the pricing standard that requires transactions between related parties to be conducted as if they were unrelated, ensuring fair market value. |

| Purpose | To allocate income and expenses appropriately within different subsidiaries in various tax jurisdictions. | To ensure that related-party transactions comply with fair market values, preventing tax avoidance. |

| Application | Applied in intra-company transactions such as sale of goods, services, royalties, or loans between affiliates. | Used as the benchmark or standard in transfer pricing regulations to evaluate if related-party prices are fair. |

| Regulatory Basis | Governed by tax laws and international guidelines, such as OECD Transfer Pricing Guidelines. | Based on the arm's-length principle, recognized internationally by bodies like the OECD and IRS. |

| Focus | Focuses on internal pricing mechanisms in multinational enterprises to allocate profits and expenses. | Focuses on determining a fair price equivalent to unrelated party transactions under comparable conditions. |

| Tax Implications | Improper transfer pricing can lead to tax adjustments, penalties, or double taxation. | Compliant arm's-length pricing helps to avoid tax disputes and ensure regulatory compliance. |

| Example | A subsidiary selling products to its parent company at a set price that may differ from market price. | The price set for that transaction is adjusted to match what unrelated parties would agree upon in a free market. |

Related Party Transactions

Related party transactions refer to business deals or arrangements between two parties with a pre-existing relationship, such as affiliates, subsidiaries, or key management personnel. These transactions are subject to strict regulatory scrutiny to ensure transparency and prevent conflicts of interest, with standards outlined by bodies like the Financial Accounting Standards Board (FASB) and the International Financial Reporting Standards (IFRS). Accurate disclosure in financial statements is mandatory under regulations like the Sarbanes-Oxley Act and SEC rules, aimed at protecting shareholders and maintaining market integrity. Proper management of related party transactions helps mitigate risks associated with favoritism, mispricing, and financial misstatement in corporate governance.

Market Value Benchmarking

Market value benchmarking in business evaluates a company's market capitalization against industry peers to identify valuation gaps and growth opportunities. This process involves analyzing financial metrics such as price-to-earnings (P/E) ratios, revenue multiples, and EBITDA margins across competitors to assess relative market positioning. Accurate benchmarking aids strategic decision-making by highlighting strengths and weaknesses in market perception and operational efficiency. Companies leveraging real-time market data and sector trends achieve more precise valuation insights and competitive advantages.

Intra-group Pricing

Intra-group pricing refers to the strategy used by multinational corporations to set prices for transactions between their affiliated entities across different countries. This practice impacts tax liabilities, as it determines how profits are allocated within the group, influencing transfer pricing compliance with regulations such as OECD guidelines. Accurate intra-group pricing ensures fair market value exchange, preventing profit shifting and tax base erosion. Effective management of these prices supports regulatory adherence and optimizes the overall financial performance of the business.

Independent Entity Principle

The Independent Entity Principle in business accounting mandates that a company's financial records and activities must be separately maintained from those of its owners or other businesses. This principle ensures accurate financial reporting by treating the business as a distinct economic unit. It facilitates clear accountability and helps in compliance with regulatory standards such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Adhering to this principle is essential for investors, creditors, and management to make well-informed decisions based on the company's true financial position.

Tax Compliance

Tax compliance in business ensures adherence to local, state, and federal tax regulations, minimizing the risk of penalties and audits. Accurate record-keeping and timely filing of income, sales, and payroll taxes are essential components for operational success. Leveraging tax software and consulting certified public accountants (CPAs) enhances accuracy and strategic tax planning. Businesses that prioritize tax compliance improve financial transparency and maintain a strong reputation with regulatory authorities.

Source and External Links

Arm's Length Principle in Transfer Pricing - Arintass - Transfer pricing between related parties is governed by the arm's length principle, which requires that the price agreed in the transaction be the same as it would be if the parties were unrelated, ensuring fair taxation and preventing profit shifting.

Section 482 & the Arm's-Length Standard | Tax Laws & Regulations - Section 482 of the U.S. tax code mandates that controlled entities set prices for intercompany transactions as if they were unrelated parties, so the price is not influenced by the relationship and reflects true market value.

What is an arm's length transaction in transfer pricing? - RoyaltyRange - An arm's length transaction in transfer pricing means the price charged between related entities should be the same as it would be between unrelated entities, ensuring tax compliance and that no special conditions apply due to the relationship.

FAQs

What is transfer pricing?

Transfer pricing is the setting of prices for transactions between related entities within a multinational corporation to allocate income and expenses across different tax jurisdictions.

What is arms-length pricing?

Arms-length pricing refers to setting prices for transactions between related parties based on market conditions as if the parties were unrelated, ensuring fair value and compliance with transfer pricing regulations.

How does transfer pricing differ from arms-length pricing?

Transfer pricing refers to the prices set for transactions between related entities within a multinational company, while arms-length pricing involves setting prices as if the transactions occurred between unrelated, independent parties in an open market.

Why is arms-length principle important in transfer pricing?

The arms-length principle ensures transfer prices between related entities reflect market conditions, preventing tax avoidance and ensuring fair allocation of taxable income.

What are the risks of incorrect transfer pricing?

Incorrect transfer pricing risks include IRS audits, substantial penalties, double taxation, damaged corporate reputation, and disrupted intercompany cash flows.

How do tax authorities evaluate transfer pricing?

Tax authorities evaluate transfer pricing by analyzing the arm's length principle, comparing related-party transaction prices with comparable uncontrolled transactions, reviewing documentation for compliance, and using methods such as the Comparable Uncontrolled Price (CUP) method, Resale Price Method, and Cost Plus Method to ensure prices reflect market conditions.

What methods are used to determine arms-length prices?

Methods to determine arm's-length prices include Comparable Uncontrolled Price (CUP), Resale Price Method (RPM), Cost Plus Method (CPM), Transactional Net Margin Method (TNMM), and Profit Split Method (PSM).