The Lucas Critique emphasizes the instability of econometric policy evaluations when structural parameters change due to policy shifts, highlighting the need for models with microfoundations and rational expectations. The Haavelmo Theorem focuses on the probabilistic interpretation of simultaneous equations models, establishing conditions for consistent estimation in structural econometrics. Explore further to understand how these foundational concepts shape modern macroeconomic modeling and policy analysis.

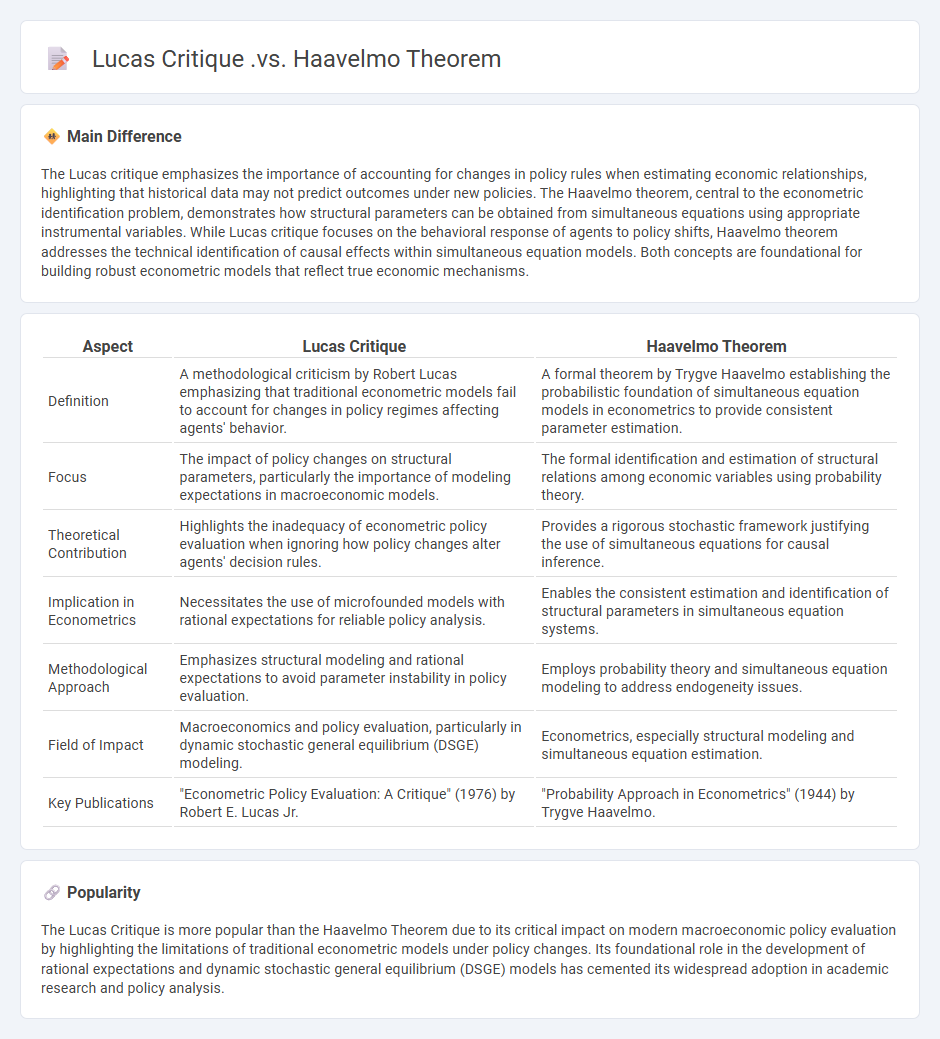

Main Difference

The Lucas critique emphasizes the importance of accounting for changes in policy rules when estimating economic relationships, highlighting that historical data may not predict outcomes under new policies. The Haavelmo theorem, central to the econometric identification problem, demonstrates how structural parameters can be obtained from simultaneous equations using appropriate instrumental variables. While Lucas critique focuses on the behavioral response of agents to policy shifts, Haavelmo theorem addresses the technical identification of causal effects within simultaneous equation models. Both concepts are foundational for building robust econometric models that reflect true economic mechanisms.

Connection

The Lucas critique challenges traditional econometric models by highlighting their failure to account for changes in policy rules affecting agents' behavior, necessitating models with microfoundations. Haavelmo's theorem underpins the importance of specifying structural equations to identify causal relationships in econometrics, which supports building models resilient to policy shifts. Together, they emphasize the need for structural, theory-based econometric models that remain valid under changing economic policies.

Comparison Table

| Aspect | Lucas Critique | Haavelmo Theorem |

|---|---|---|

| Definition | A methodological criticism by Robert Lucas emphasizing that traditional econometric models fail to account for changes in policy regimes affecting agents' behavior. | A formal theorem by Trygve Haavelmo establishing the probabilistic foundation of simultaneous equation models in econometrics to provide consistent parameter estimation. |

| Focus | The impact of policy changes on structural parameters, particularly the importance of modeling expectations in macroeconomic models. | The formal identification and estimation of structural relations among economic variables using probability theory. |

| Theoretical Contribution | Highlights the inadequacy of econometric policy evaluation when ignoring how policy changes alter agents' decision rules. | Provides a rigorous stochastic framework justifying the use of simultaneous equations for causal inference. |

| Implication in Econometrics | Necessitates the use of microfounded models with rational expectations for reliable policy analysis. | Enables the consistent estimation and identification of structural parameters in simultaneous equation systems. |

| Methodological Approach | Emphasizes structural modeling and rational expectations to avoid parameter instability in policy evaluation. | Employs probability theory and simultaneous equation modeling to address endogeneity issues. |

| Field of Impact | Macroeconomics and policy evaluation, particularly in dynamic stochastic general equilibrium (DSGE) modeling. | Econometrics, especially structural modeling and simultaneous equation estimation. |

| Key Publications | "Econometric Policy Evaluation: A Critique" (1976) by Robert E. Lucas Jr. | "Probability Approach in Econometrics" (1944) by Trygve Haavelmo. |

Structural Parameters

Structural parameters in economics quantify fundamental relationships within economic models, such as preference elasticities, technology coefficients, and productivity levels. These parameters remain stable across different policy environments, allowing economists to predict outcomes under varying conditions. Estimating structural parameters typically involves econometric techniques applied to microdata or macroeconomic time series, ensuring identification and consistency. Understanding these parameters is crucial for policy analysis, growth modeling, and forecasting economic behavior accurately.

Policy Invariance

Policy invariance in economics refers to the principle that structural economic relationships remain stable under different policy regimes. This concept is crucial in econometric modeling, ensuring that estimated parameters reflect true causal mechanisms rather than policy-specific responses. For instance, the Lucas Critique highlights that traditional econometric models may fail if agents adjust their behavior when policies change. Reliable policy analysis depends on models that capture these invariant structural relationships across varying policy environments.

Simultaneity (Haavelmo)

Simultaneity in economics, particularly as developed by economist Trygve Haavelmo, refers to situations where variables mutually influence each other within a system of simultaneous equations, such as supply and demand models. Haavelmo's contributions helped formalize the econometric analysis of simultaneous relationships, emphasizing the need for identification strategies to estimate causal effects accurately. This concept underpins the structure of modern simultaneous equation models used in macroeconomic and microeconomic contexts. Understanding simultaneity is crucial for avoiding biased estimations in regression analysis when dependent variables are jointly determined.

Rational Expectations

Rational expectations theory asserts that individuals form forecasts about the future based on all available information, including government policies and economic models. This concept plays a crucial role in modern macroeconomics, influencing models such as the New Classical and Real Business Cycle theories. Empirical studies show that rational expectations can lead to policy ineffectiveness, particularly in predicting inflation trends. Understanding rational expectations helps explain economic phenomena like wage rigidity and market adjustments in response to shocks.

Model Consistency

Model consistency in economics ensures that theoretical frameworks and empirical data align accurately to produce reliable predictions. It involves validating that economic models maintain internal logic while reflecting real-world behaviors and market dynamics. Robust model consistency improves policy analysis, risk assessment, and forecasting by minimizing errors arising from contradictory assumptions. Empirical testing and calibration against historical data remain critical for sustaining model validity over time.

Source and External Links

Nobel Laureate: Trygve Haavelmo - American Economic Association - The Lucas critique is a special case of Haavelmo's broader criticism that policy simulations based on relations lacking the required autonomy are unreliable, highlighting Haavelmo's pioneering work on simultaneous equations that addressed econometric identification problems before Lucas's insight.

Main research areas - Department of Economics - UiO - Haavelmo's theorem states that a balanced budget increase in taxes and public spending can increase aggregate demand, explaining how government expenditure financed by equivalent taxes boosts gross income and employment without reducing private demand.

A Lucas Critique - World Economics Association - Haavelmo raised the problem of econometric stability and parameter identification well before Lucas, who notably enhanced this by formalizing how policy changes alter economic model parameters due to agents' rational expectations, thus leading to the "Lucas critique" in macroeconomic policy evaluation.

FAQs

What is the Lucas Critique?

The Lucas Critique states that traditional economic policy evaluations fail when they ignore changes in agents' behavior and expectations caused by policy shifts, emphasizing the need for models with micro-founded, forward-looking agents.

What is the Haavelmo Theorem?

The Haavelmo Theorem establishes the probabilistic foundation for simultaneous equations in econometrics, demonstrating that error terms must be uncorrelated with explanatory variables to ensure consistent parameter estimation.

How does the Lucas Critique challenge traditional macroeconomic models?

The Lucas Critique challenges traditional macroeconomic models by arguing that policy evaluations based on historical data are unreliable because agents adjust their behavior in response to changes in policy rules, rendering past relationships unstable.

What role does the Haavelmo Theorem play in econometrics?

The Haavelmo Theorem establishes the foundation for interpreting econometric models probabilistically, ensuring that economic relationships can be analyzed using statistical methods.

How do policy evaluations differ under Lucas Critique and Haavelmo Theorem?

Policy evaluations under the Lucas Critique focus on the failure of traditional models to account for changes in agents' expectations and behavior following policy shifts, emphasizing the need for models incorporating microfoundations and rational expectations. The Haavelmo Theorem supports causal interpretation in econometrics by ensuring that structural parameters remain stable under policy interventions, enabling consistent estimation of policy effects from observed data.

Why is structural modeling important according to the Lucas Critique?

Structural modeling is important according to the Lucas Critique because it captures deep, policy-invariant relationships between economic variables, allowing reliable prediction of policy impacts by accounting for changes in agents' behavior.

How did the Haavelmo Theorem influence the development of econometric methodology?

The Haavelmo Theorem established the probabilistic foundation of simultaneous equations models, leading to the formalization of identification conditions and consistent estimation methods in econometrics.