Neoclassical economics emphasizes rational decision-making, market equilibrium, and utility maximization, relying on mathematical models to predict economic behavior. Behavioral economics integrates psychological insights into economic theory, highlighting cognitive biases, heuristics, and irrational behaviors influencing market outcomes. Explore these frameworks to understand their impact on economic policy and consumer behavior.

Main Difference

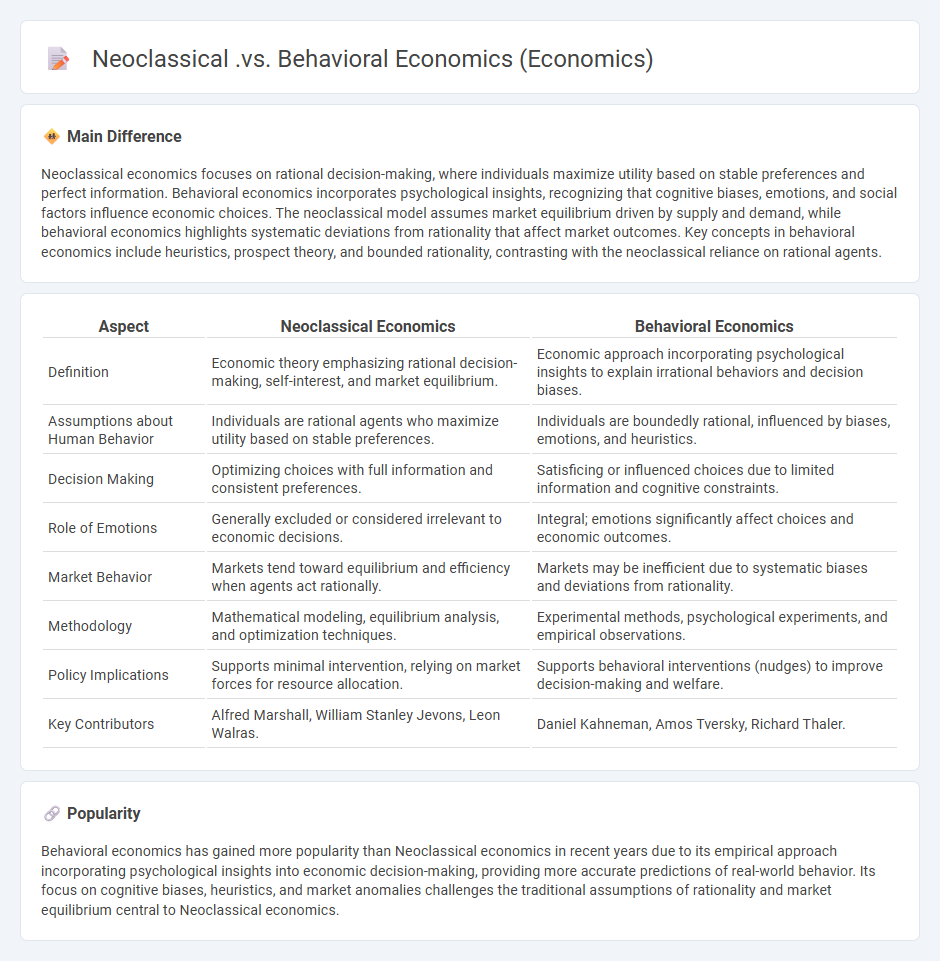

Neoclassical economics focuses on rational decision-making, where individuals maximize utility based on stable preferences and perfect information. Behavioral economics incorporates psychological insights, recognizing that cognitive biases, emotions, and social factors influence economic choices. The neoclassical model assumes market equilibrium driven by supply and demand, while behavioral economics highlights systematic deviations from rationality that affect market outcomes. Key concepts in behavioral economics include heuristics, prospect theory, and bounded rationality, contrasting with the neoclassical reliance on rational agents.

Connection

Neoclassical economics focuses on rational decision-making models and market equilibrium, while behavioral economics incorporates psychological insights to explain deviations from rational behavior. Both fields intersect by analyzing how individuals make economic choices, with behavioral economics expanding on neoclassical assumptions to include cognitive biases and emotions. This connection enriches economic theory by providing a more comprehensive understanding of real-world decision processes.

Comparison Table

| Aspect | Neoclassical Economics | Behavioral Economics |

|---|---|---|

| Definition | Economic theory emphasizing rational decision-making, self-interest, and market equilibrium. | Economic approach incorporating psychological insights to explain irrational behaviors and decision biases. |

| Assumptions about Human Behavior | Individuals are rational agents who maximize utility based on stable preferences. | Individuals are boundedly rational, influenced by biases, emotions, and heuristics. |

| Decision Making | Optimizing choices with full information and consistent preferences. | Satisficing or influenced choices due to limited information and cognitive constraints. |

| Role of Emotions | Generally excluded or considered irrelevant to economic decisions. | Integral; emotions significantly affect choices and economic outcomes. |

| Market Behavior | Markets tend toward equilibrium and efficiency when agents act rationally. | Markets may be inefficient due to systematic biases and deviations from rationality. |

| Methodology | Mathematical modeling, equilibrium analysis, and optimization techniques. | Experimental methods, psychological experiments, and empirical observations. |

| Policy Implications | Supports minimal intervention, relying on market forces for resource allocation. | Supports behavioral interventions (nudges) to improve decision-making and welfare. |

| Key Contributors | Alfred Marshall, William Stanley Jevons, Leon Walras. | Daniel Kahneman, Amos Tversky, Richard Thaler. |

Rationality

Rationality refers to the quality of being based on or in accordance with reason and logic, allowing individuals to make decisions that maximize expected utility or achieve specific goals efficiently. In cognitive science, rationality is often categorized into bounded rationality, which accounts for cognitive limitations, and perfect rationality, which assumes optimal decision-making given complete information. Economic models frequently incorporate rationality to predict behavior, assuming agents act to maximize their preferences under constraints. Advances in artificial intelligence further explore rationality by designing algorithms that simulate human-like decision-making processes.

Utility Maximization

Utility maximization is a fundamental concept in microeconomics where consumers allocate their income to purchase goods and services that yield the highest satisfaction or utility. This behavior is modeled using utility functions that quantify preferences, subject to budget constraints. The principle assumes rational decision-making, aiming to achieve the optimal consumption bundle that maximizes total utility. Applications include consumer choice theory, revealed preference, and demand curve analysis.

Bounded Rationality

Bounded rationality refers to the concept that decision-makers operate under cognitive limitations and incomplete information, which restrict their ability to make fully rational choices. Introduced by Herbert A. Simon in the 1950s, this theory challenges the classical economic assumption of perfect rationality. Individuals use heuristics and satisficing strategies to make satisfactory rather than optimal decisions within these constraints. Bounded rationality is widely applied in behavioral economics, cognitive psychology, and organizational theory to understand real-world decision processes.

Market Equilibrium

Market equilibrium occurs when the quantity of goods supplied equals the quantity demanded at a specific price point, resulting in a stable market condition. This balance ensures that there is no surplus or shortage, allowing resources to be efficiently allocated. Prices tend to adjust in response to shifts in demand or supply until the market reaches a new equilibrium. Real-world examples include agricultural markets where equilibrium prices respond to seasonal changes and consumer demand fluctuations.

Cognitive Biases

Cognitive biases are systematic patterns of deviation from norm or rationality in judgment, often influencing decision-making and perception. Common examples include confirmation bias, where individuals favor information confirming their beliefs, and anchoring bias, which causes reliance on the first piece of information encountered. These biases impact various domains such as finance, healthcare, and social interactions, leading to suboptimal outcomes. Understanding cognitive biases is essential for improving critical thinking and reducing errors in reasoning.

Source and External Links

Neoclassical Economics And Behavioral Economics - Neoclassical economics assumes individuals are perfectly rational utility maximizers, while behavioral economics challenges this by incorporating psychological insights to explain real-world decision-making inconsistencies.

Neo-classical vs Behavioural economics - Neo-classical economics relies on mathematical models assuming rational actors maximizing utility with perfect information, whereas behavioral economics draws from psychology and neuroscience to understand human behavior as complex and often irrational.

Classical versus Behavioral Economics: Environmental Applications - Unlike neoclassical economics' belief in rational self-interest guiding choices, behavioral economics shows that humans often act irrationally and against their own long-term benefits, explaining why traditional models fail to predict real human behavior in contexts like environmental policy.

FAQs

What is economics?

Economics is the social science that studies the production, distribution, and consumption of goods and services.

What is neoclassical economics?

Neoclassical economics is an economic theory focusing on supply and demand as drivers of price and production in markets, centered on rational decision-making, utility maximization, and equilibrium analysis.

What is behavioral economics?

Behavioral economics studies how psychological, social, and cognitive factors influence individuals' economic decisions, deviating from traditional rational choice theory.

How does neoclassical economics explain decision-making?

Neoclassical economics explains decision-making as a rational process where individuals maximize utility by making choices based on preferences, constraints, and available information.

How does behavioral economics explain human behavior?

Behavioral economics explains human behavior by integrating psychological insights with economic theory, highlighting cognitive biases, heuristics, and emotions that cause deviations from rational decision-making.

What are the key differences between neoclassical and behavioral economics?

Neoclassical economics relies on rational agents, utility maximization, and equilibrium models, while behavioral economics incorporates psychological insights, irrational behaviors, cognitive biases, and bounded rationality into economic decision-making.

Why is understanding these differences important in real-world economics?

Understanding these differences is crucial in real-world economics because it enables accurate market analysis, informs effective policy-making, predicts consumer behavior, and optimizes resource allocation.