Behavioral finance explores how psychological factors and cognitive biases influence investors' financial decisions, contrasting with traditional finance's reliance on rational models and efficient market theory. This field examines patterns like overconfidence, herd behavior, and loss aversion that explain market anomalies beyond classical assumptions. Discover deeper insights into how human behavior reshapes financial strategies and market dynamics.

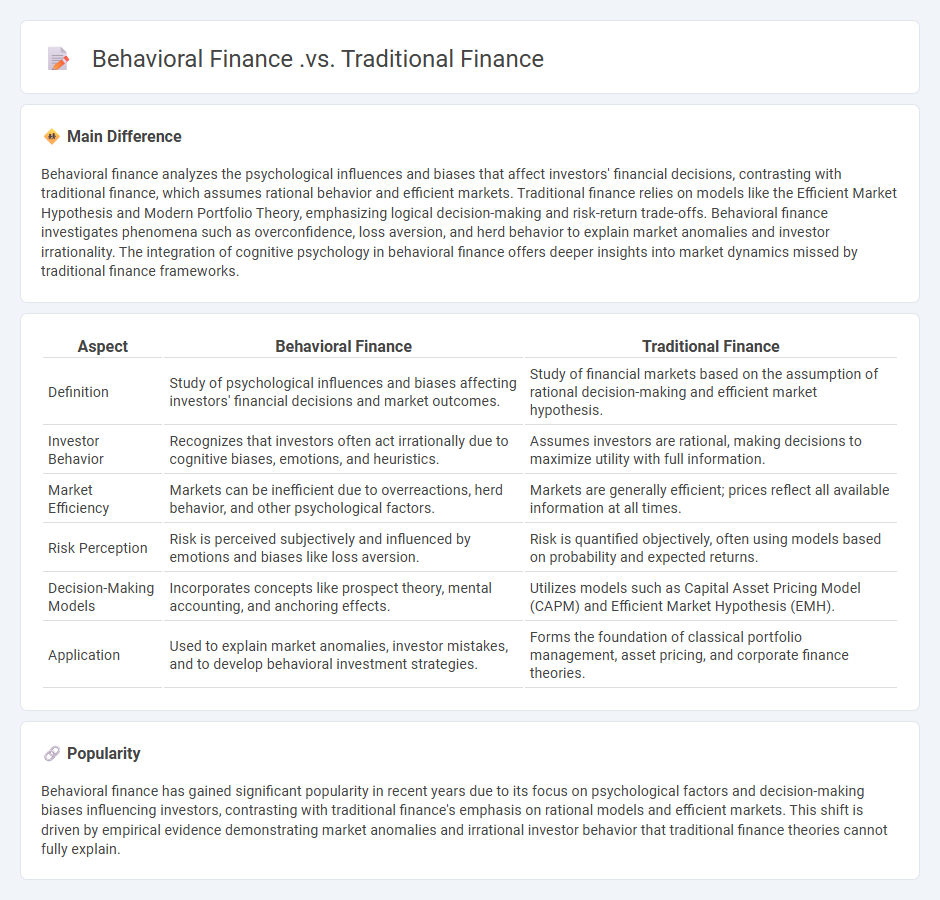

Main Difference

Behavioral finance analyzes the psychological influences and biases that affect investors' financial decisions, contrasting with traditional finance, which assumes rational behavior and efficient markets. Traditional finance relies on models like the Efficient Market Hypothesis and Modern Portfolio Theory, emphasizing logical decision-making and risk-return trade-offs. Behavioral finance investigates phenomena such as overconfidence, loss aversion, and herd behavior to explain market anomalies and investor irrationality. The integration of cognitive psychology in behavioral finance offers deeper insights into market dynamics missed by traditional finance frameworks.

Connection

Behavioral finance complements traditional finance by incorporating psychological factors and cognitive biases into the analysis of financial markets and investor behavior. Traditional finance relies on the efficient market hypothesis and rational decision-making models, while behavioral finance explains anomalies and market inefficiencies through concepts like herd behavior, overconfidence, and loss aversion. Together, these fields provide a comprehensive understanding of market dynamics, enhancing investment strategies and risk management.

Comparison Table

| Aspect | Behavioral Finance | Traditional Finance |

|---|---|---|

| Definition | Study of psychological influences and biases affecting investors' financial decisions and market outcomes. | Study of financial markets based on the assumption of rational decision-making and efficient market hypothesis. |

| Investor Behavior | Recognizes that investors often act irrationally due to cognitive biases, emotions, and heuristics. | Assumes investors are rational, making decisions to maximize utility with full information. |

| Market Efficiency | Markets can be inefficient due to overreactions, herd behavior, and other psychological factors. | Markets are generally efficient; prices reflect all available information at all times. |

| Risk Perception | Risk is perceived subjectively and influenced by emotions and biases like loss aversion. | Risk is quantified objectively, often using models based on probability and expected returns. |

| Decision-Making Models | Incorporates concepts like prospect theory, mental accounting, and anchoring effects. | Utilizes models such as Capital Asset Pricing Model (CAPM) and Efficient Market Hypothesis (EMH). |

| Application | Used to explain market anomalies, investor mistakes, and to develop behavioral investment strategies. | Forms the foundation of classical portfolio management, asset pricing, and corporate finance theories. |

Rationality vs. Irrationality

Rationality in business drives decision-making through data analysis, logical reasoning, and evidence-based strategies to maximize efficiency and profitability. Irrationality often leads to biased judgments, emotional decisions, and risk-taking behaviors that can result in financial losses or missed opportunities. Companies like Amazon exemplify rational decision-making by leveraging big data and artificial intelligence to optimize operations and customer experiences. Conversely, irrational decisions, such as overconfidence or herd behavior, have contributed to business failures like the 2008 financial crisis.

Efficient Market Hypothesis

The Efficient Market Hypothesis (EMH) asserts that financial markets are informationally efficient, meaning asset prices fully reflect all available information at any given time. According to EMH, it is impossible to consistently achieve higher returns than average market returns on a risk-adjusted basis through stock selection or market timing. The hypothesis is categorized into three forms: weak, semi-strong, and strong, each reflecting varying degrees of market efficiency based on the type of information incorporated into prices. Empirical studies, such as those analyzing stock price movements on the New York Stock Exchange, provide mixed evidence regarding the validity of EMH in real-world business environments.

Cognitive Biases

Cognitive biases significantly impact business decision-making, often leading to systematic errors that can affect strategies and outcomes. Confirmation bias causes managers to favor information that supports their preconceptions, while anchoring bias skews financial forecasts based on initial values. Understanding biases such as overconfidence and availability heuristic improves risk assessment and enhances strategic planning. Companies like Google employ behavioral economics principles to design better products and promote rational decision-making.

Emotional Influence

Emotional influence in business significantly impacts decision-making, leadership effectiveness, and customer relationships by shaping perceptions and motivating actions. Research shows that emotionally intelligent leaders achieve 20% higher employee engagement and 15% increased productivity. Consumer behavior studies reveal that emotions drive up to 80% of purchasing decisions, underlining the critical role of emotional marketing strategies. Companies investing in emotional intelligence training often report improved team collaboration and higher retention rates.

Heuristics

Heuristics in business refer to practical decision-making strategies that simplify complex problems through experience-based techniques and rule-of-thumb methods. These approaches enable managers to make quick, efficient decisions in uncertain conditions, often improving operational efficiency and risk management. Common business heuristics include satisficing, anchoring, and availability bias, which influence consumer behavior, marketing strategies, and financial forecasting. Companies leveraging data-driven heuristics can optimize resource allocation and enhance strategic planning outcomes.

Source and External Links

Behavioral finance vs. traditional finance | Chapters - Vocal Media - Behavioral finance highlights the importance of emotions and psychological biases in financial decisions, challenging the traditional finance assumption of market efficiency and rational decision-making based solely on risk and return analysis.

Behavioral Finance: Investor Psychology & Market Anomalies - Traditional finance assumes rational decision-making aligning with best interests, while behavioral finance studies how psychological biases cause irrational financial choices and market anomalies.

What Is Behavioral Finance? - UNCP Online - Traditional finance assumes logical decisions based on data and risk aversion, whereas behavioral finance incorporates cognitive and emotional biases that lead individuals to make seemingly irrational financial decisions.

FAQs

What is traditional finance?

Traditional finance refers to conventional financial systems and institutions such as banks, stock exchanges, insurance companies, and investment firms that operate under established regulations and centralized control.

What is behavioral finance?

Behavioral finance studies the impact of psychological factors and cognitive biases on investors' financial decisions and market outcomes.

How does behavioral finance differ from traditional finance?

Behavioral finance incorporates psychological insights and cognitive biases to explain investor behavior, while traditional finance assumes rational decision-making and efficient markets.

What are the key assumptions of traditional finance?

Key assumptions of traditional finance include investor rationality, market efficiency, risk-return tradeoff, and the existence of perfect information.

What psychological factors influence behavioral finance?

Cognitive biases, emotions, overconfidence, herd behavior, loss aversion, mental accounting, and framing effects are key psychological factors influencing behavioral finance.

How do emotions impact financial decision-making?

Emotions such as fear and greed significantly influence financial decision-making by causing biases like overconfidence, loss aversion, and herd behavior, leading to suboptimal investment choices and market volatility.

Why is behavioral finance important in understanding market anomalies?

Behavioral finance explains market anomalies by identifying cognitive biases and emotional factors that lead to irrational investor behavior, which traditional finance models often overlook.