Job costing tracks expenses for individual projects or jobs, making it ideal for customized work with distinct cost accumulation. Process costing averages costs over continuous production processes, suitable for large-scale manufacturing of uniform products. Explore detailed comparisons to determine the best costing method for your business needs.

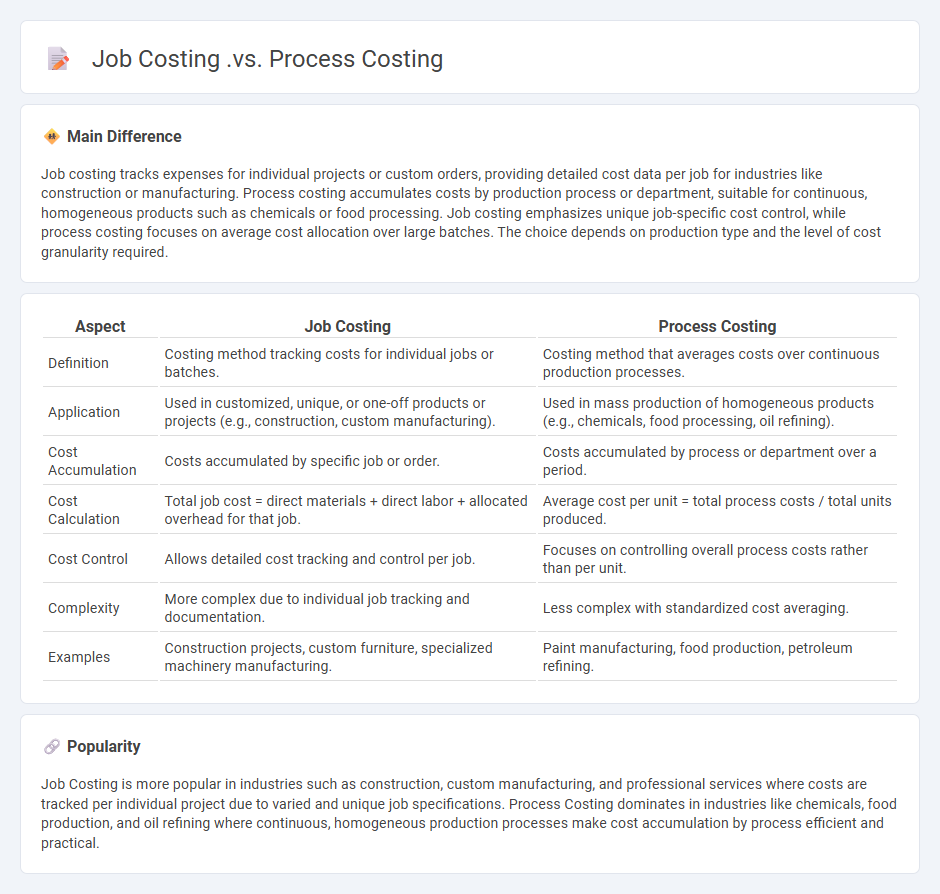

Main Difference

Job costing tracks expenses for individual projects or custom orders, providing detailed cost data per job for industries like construction or manufacturing. Process costing accumulates costs by production process or department, suitable for continuous, homogeneous products such as chemicals or food processing. Job costing emphasizes unique job-specific cost control, while process costing focuses on average cost allocation over large batches. The choice depends on production type and the level of cost granularity required.

Connection

Job costing and process costing are interconnected cost accounting methods used to allocate manufacturing expenses accurately. Both systems gather and assign costs to products, with job costing focusing on specific, customizable projects, while process costing distributes costs across continuous production processes. Integration of these methods enhances cost control and financial analysis in industries producing both unique and homogeneous goods.

Comparison Table

| Aspect | Job Costing | Process Costing |

|---|---|---|

| Definition | Costing method tracking costs for individual jobs or batches. | Costing method that averages costs over continuous production processes. |

| Application | Used in customized, unique, or one-off products or projects (e.g., construction, custom manufacturing). | Used in mass production of homogeneous products (e.g., chemicals, food processing, oil refining). |

| Cost Accumulation | Costs accumulated by specific job or order. | Costs accumulated by process or department over a period. |

| Cost Calculation | Total job cost = direct materials + direct labor + allocated overhead for that job. | Average cost per unit = total process costs / total units produced. |

| Cost Control | Allows detailed cost tracking and control per job. | Focuses on controlling overall process costs rather than per unit. |

| Complexity | More complex due to individual job tracking and documentation. | Less complex with standardized cost averaging. |

| Examples | Construction projects, custom furniture, specialized machinery manufacturing. | Paint manufacturing, food production, petroleum refining. |

Cost Allocation

Cost allocation in business involves assigning indirect costs to different departments, products, or projects based on predefined criteria to ensure accurate financial reporting and profitability analysis. Common methods include activity-based costing, where expenses are allocated according to activities driving costs, and traditional costing, which distributes overhead evenly. Effective cost allocation enhances budgeting accuracy, supports strategic decision-making, and improves resource management. Accurate allocation is essential for pricing, cost control, and evaluating business unit performance.

Job Order Costing

Job Order Costing allocates manufacturing costs to specific jobs or batches, enabling precise tracking of expenses for customized products. This costing method records direct materials, direct labor, and allocated overhead for each job, facilitating accurate cost control and pricing strategies. Businesses in industries such as construction, aerospace, and custom manufacturing rely extensively on job order costing to manage complex production processes. Accurate job costing enhances profitability analysis and financial reporting, supporting better decision-making.

Process Costing

Process costing is a cost accounting method used predominantly in manufacturing industries where production is continuous, such as chemical, textile, and food processing industries. It assigns average costs to each unit by accumulating costs over a specific period and dividing by total units produced, facilitating accurate cost control and pricing decisions. Key components include direct materials, direct labor, and manufacturing overhead costs, tracked through work-in-process accounts during each production stage. Leading software solutions like SAP ERP and Oracle E-Business Suite integrate process costing modules to enhance real-time cost monitoring and financial reporting.

Customization Level

Customization level in business refers to the degree to which products or services are tailored to meet individual customer preferences and requirements. High customization levels enable companies to enhance customer satisfaction by offering personalized solutions, which can lead to increased loyalty and higher profit margins. Businesses in industries such as technology, fashion, and automotive often invest in advanced manufacturing and data analytics tools to optimize customization processes. According to a 2023 Gartner report, 72% of consumers expect personalized products and experiences, making customization a critical competitive advantage.

Industry Application

Business industries leverage advanced data analytics to drive strategic decision-making and enhance operational efficiency. Integration of artificial intelligence (AI) streamlines customer relationship management, leading to increased customer retention and personalized marketing campaigns. Supply chain optimization through machine learning models reduces costs and improves delivery timelines, boosting overall profitability. Digital transformation efforts focus on cloud computing and automation technologies to support scalable growth and competitive advantage.

Source and External Links

Job Costing vs Process Costing Explained | PLANERGY Software - Job costing is best for small, customized production units where costs are calculated per job with detailed record-keeping, while process costing suits large, standardized mass production with costs averaged per process and efficient record management.

The difference between job costing and process costing - Job costing tracks costs for unique, small production runs requiring extensive record keeping and is customer-focused, whereas process costing is used for large volume, standardized products with aggregated cost records and less detailed billing.

Job Order Costing vs. Process Costing: What's the Difference? - Job order costing calculates costs individually for customized jobs often billed by detailed estimates, while process costing averages costs over large production runs of standardized items, reflecting minimal variation among units.

FAQs

What is job costing?

Job costing is a cost accounting method that tracks expenses and revenues for individual projects or jobs to determine their profitability.

What is process costing?

Process costing is a cost accounting method used to allocate production costs to identical or similar units in continuous manufacturing processes.

How does job costing work?

Job costing works by tracking and accumulating all direct materials, direct labor, and overhead costs for a specific job or project to determine its total cost and profitability.

How does process costing work?

Process costing allocates total production costs evenly across all units produced by dividing accumulated costs by the number of units, tracking costs for each production department or process stage.

What types of companies use job costing?

Construction, manufacturing, engineering, consulting, and custom fabrication companies commonly use job costing.

What types of companies use process costing?

Companies in industries such as chemicals, pharmaceuticals, food and beverage, petroleum, textiles, and paper manufacturing typically use process costing.

What are the main differences between job costing and process costing?

Job costing tracks costs for specific, customized projects or jobs, while process costing accumulates costs for continuous, homogeneous production processes.