Gross margin measures the profitability of a company after subtracting the cost of goods sold (COGS) from total revenue, reflecting the efficiency in production and pricing strategies. Contribution margin calculates the amount remaining from sales revenue after variable costs are deducted, indicating how much is available to cover fixed costs and generate profit. Explore deeper insights into how these metrics influence financial decision-making and operational strategies.

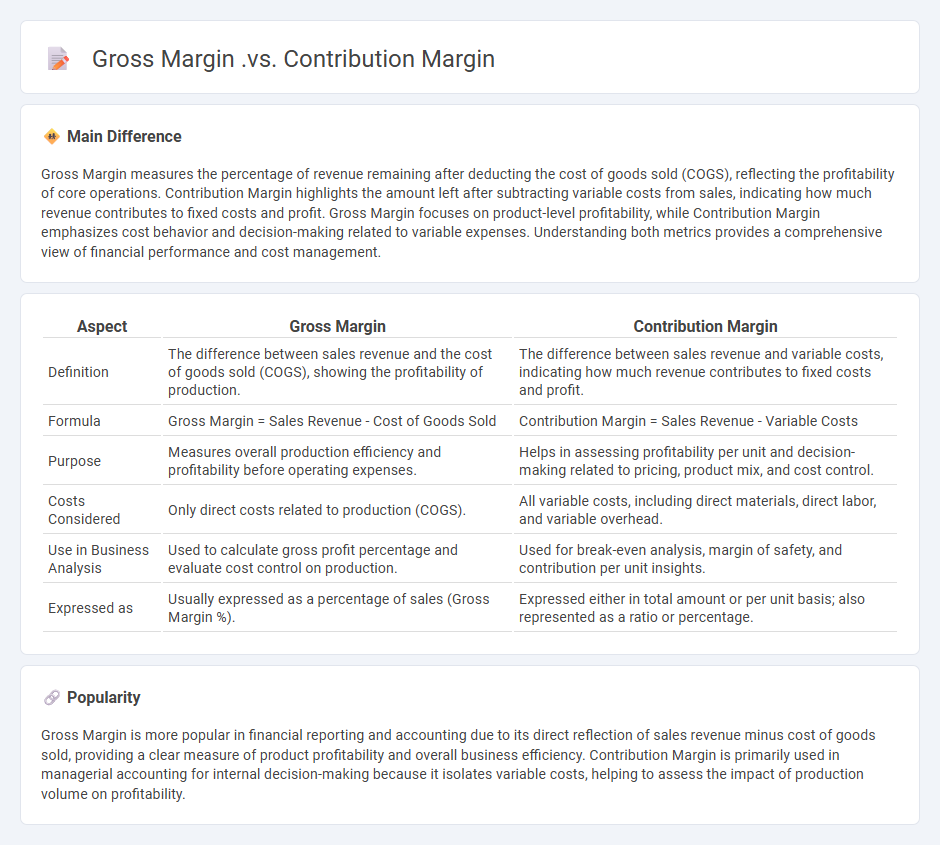

Main Difference

Gross Margin measures the percentage of revenue remaining after deducting the cost of goods sold (COGS), reflecting the profitability of core operations. Contribution Margin highlights the amount left after subtracting variable costs from sales, indicating how much revenue contributes to fixed costs and profit. Gross Margin focuses on product-level profitability, while Contribution Margin emphasizes cost behavior and decision-making related to variable expenses. Understanding both metrics provides a comprehensive view of financial performance and cost management.

Connection

Gross margin measures the percentage of revenue remaining after deducting the cost of goods sold (COGS), highlighting product profitability. Contribution margin calculates the amount remaining from sales revenue after variable costs, indicating how much contributes to fixed costs and profit. Both metrics interrelate by showing different layers of cost impact on overall profitability, with gross margin focused on direct production costs and contribution margin extending to variable operating expenses.

Comparison Table

| Aspect | Gross Margin | Contribution Margin |

|---|---|---|

| Definition | The difference between sales revenue and the cost of goods sold (COGS), showing the profitability of production. | The difference between sales revenue and variable costs, indicating how much revenue contributes to fixed costs and profit. |

| Formula | Gross Margin = Sales Revenue - Cost of Goods Sold | Contribution Margin = Sales Revenue - Variable Costs |

| Purpose | Measures overall production efficiency and profitability before operating expenses. | Helps in assessing profitability per unit and decision-making related to pricing, product mix, and cost control. |

| Costs Considered | Only direct costs related to production (COGS). | All variable costs, including direct materials, direct labor, and variable overhead. |

| Use in Business Analysis | Used to calculate gross profit percentage and evaluate cost control on production. | Used for break-even analysis, margin of safety, and contribution per unit insights. |

| Expressed as | Usually expressed as a percentage of sales (Gross Margin %). | Expressed either in total amount or per unit basis; also represented as a ratio or percentage. |

Gross Margin

Gross margin measures the difference between revenue and the cost of goods sold (COGS), expressed as a percentage of total sales. It indicates a company's efficiency in producing goods or services and ability to control production costs. For example, a gross margin of 40% means that 40 cents of every dollar in sales is available to cover operating expenses and profit. Businesses in industries like software often have higher gross margins compared to manufacturing companies due to lower variable costs.

Contribution Margin

Contribution Margin measures the difference between sales revenue and variable costs directly associated with product production. It indicates how much revenue contributes to covering fixed costs and generating profit after variable expenses are paid. Businesses use this metric to evaluate product profitability, pricing strategies, and cost management. Companies with high contribution margins typically have greater flexibility to invest in growth and sustain operations.

Fixed Costs

Fixed costs refer to business expenses that remain constant regardless of production levels or sales volume, such as rent, salaries, and insurance. These costs must be paid regularly, even when the business experiences zero output or sales. Understanding fixed costs is crucial for accurate break-even analysis and financial forecasting. Businesses often separate fixed costs from variable costs to optimize budgeting and profitability strategies.

Variable Costs

Variable costs in business refer to expenses that fluctuate directly with production volume or sales activity, such as raw materials, direct labor, and utility costs tied to manufacturing. These costs are critical for financial planning and break-even analysis because they impact profit margins and pricing strategies. Monitoring variable costs enables businesses to optimize operational efficiency and adjust output levels in response to market demand. Effective management of variable expenses supports scalability and helps maintain competitive advantage in dynamic markets.

Profitability Analysis

Profitability analysis in business measures a company's ability to generate earnings relative to its revenue, operating costs, and equity. Key financial metrics include gross profit margin, net profit margin, return on assets (ROA), and return on equity (ROE), which help assess operational efficiency and financial health. Analyzing profitability trends supports strategic decision-making, cost control, and investment evaluation. Tools such as financial statements, ratio analysis, and benchmarking against industry standards enhance the accuracy of profitability assessments.

Source and External Links

What is Contribution Margin: Profitability Analysis - Saras Analytics - Contribution margin is sales revenue minus variable costs, showing how much is available to cover fixed costs and profit, while gross margin is sales revenue minus total cost of goods sold (both fixed and variable costs), reflecting the profit after production costs.

Contribution Margin vs. Gross Margin: What's the Difference? - Shopify - Contribution margin considers only variable costs to measure profitability per product, helping decide product investment, while gross margin includes all direct production costs to assess overall profitability.

Gross Margin vs. Contribution Margin: How They Differ | Indeed.com - Gross margin is a total profit metric subtracting cost of goods sold from revenue to measure overall profitability, whereas contribution margin is a per-item metric subtracting variable expenses to show product-level profit potential.

FAQs

What is gross margin?

Gross margin is the percentage difference between revenue and the cost of goods sold (COGS), calculated as (Revenue - COGS) / Revenue, indicating the profitability of core business activities.

What is contribution margin?

Contribution margin is the amount remaining from sales revenue after deducting variable costs, used to cover fixed costs and generate profit.

How do gross margin and contribution margin differ?

Gross margin measures the percentage of revenue remaining after deducting cost of goods sold (COGS), reflecting product profitability, while contribution margin represents the amount left from sales revenue after variable costs, indicating how much contributes to fixed costs and profit.

Why is gross margin important for a business?

Gross margin is important for a business because it measures profitability by showing the percentage of revenue remaining after covering the cost of goods sold, enabling effective pricing strategies and cost control.

Why is contribution margin useful for decision-making?

Contribution margin is useful for decision-making because it shows how much revenue exceeds variable costs, helping businesses evaluate product profitability, set prices, and determine break-even points.

How are gross margin and contribution margin calculated?

Gross margin is calculated as (Revenue - Cost of Goods Sold) / Revenue x 100%. Contribution margin is calculated as (Sales Revenue - Variable Costs) / Sales Revenue x 100%.

When should a company use gross margin vs contribution margin?

Use gross margin to evaluate overall profitability by measuring revenue minus cost of goods sold; use contribution margin to assess the impact of variable costs on profitability and to make decisions about pricing, product lines, or production levels.