Zero-Based Budgeting (ZBB) requires justifying every expense from zero, ensuring resources are allocated based on current needs and priorities, while Incremental Budgeting adjusts previous budgets by adding or subtracting a percentage to address changes. ZBB enhances cost efficiency and accountability, particularly useful in dynamic or resource-constrained environments, whereas Incremental Budgeting offers simplicity and stability, favored for its ease of implementation in stable organizations. Explore the key differences and applications of these budgeting methods to optimize your financial planning strategy.

Main Difference

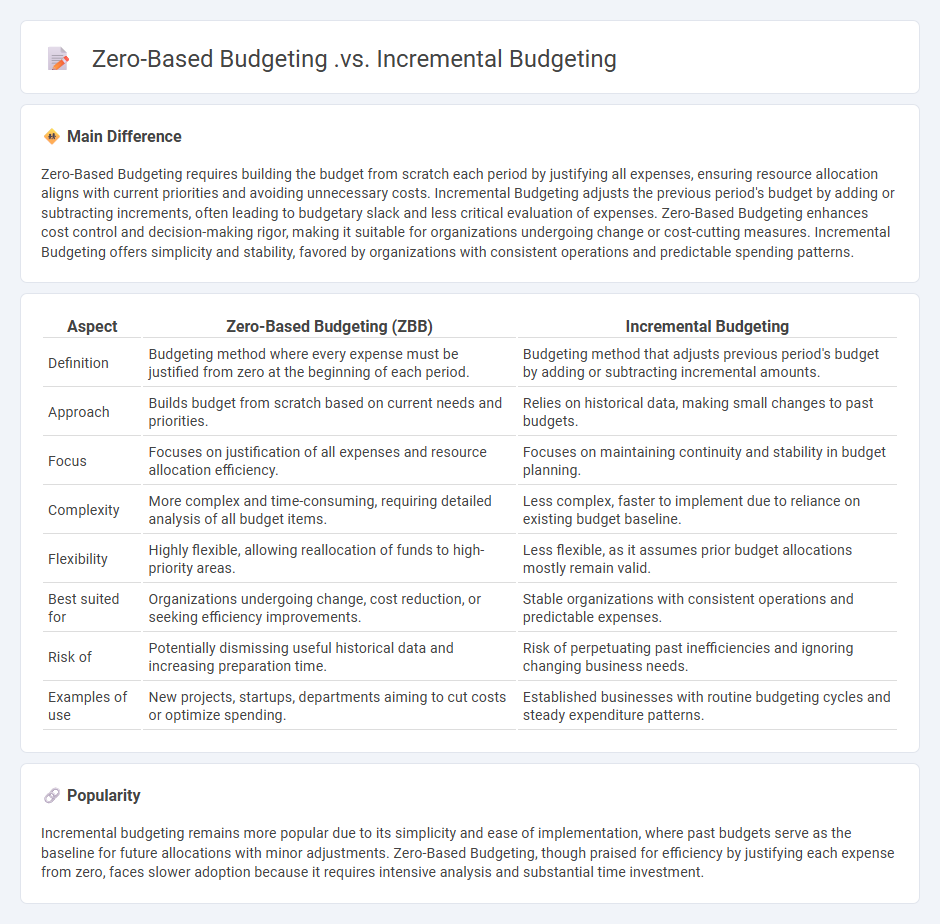

Zero-Based Budgeting requires building the budget from scratch each period by justifying all expenses, ensuring resource allocation aligns with current priorities and avoiding unnecessary costs. Incremental Budgeting adjusts the previous period's budget by adding or subtracting increments, often leading to budgetary slack and less critical evaluation of expenses. Zero-Based Budgeting enhances cost control and decision-making rigor, making it suitable for organizations undergoing change or cost-cutting measures. Incremental Budgeting offers simplicity and stability, favored by organizations with consistent operations and predictable spending patterns.

Connection

Zero-Based Budgeting (ZBB) and Incremental Budgeting are connected through their roles in financial planning and resource allocation within organizations. While Incremental Budgeting adjusts previous budgets by adding or subtracting increments, ZBB requires justifying every expense from scratch, promoting more detailed analysis and efficient use of resources. Both methods aim to control costs but differ in their approach to budget justification and flexibility.

Comparison Table

| Aspect | Zero-Based Budgeting (ZBB) | Incremental Budgeting |

|---|---|---|

| Definition | Budgeting method where every expense must be justified from zero at the beginning of each period. | Budgeting method that adjusts previous period's budget by adding or subtracting incremental amounts. |

| Approach | Builds budget from scratch based on current needs and priorities. | Relies on historical data, making small changes to past budgets. |

| Focus | Focuses on justification of all expenses and resource allocation efficiency. | Focuses on maintaining continuity and stability in budget planning. |

| Complexity | More complex and time-consuming, requiring detailed analysis of all budget items. | Less complex, faster to implement due to reliance on existing budget baseline. |

| Flexibility | Highly flexible, allowing reallocation of funds to high-priority areas. | Less flexible, as it assumes prior budget allocations mostly remain valid. |

| Best suited for | Organizations undergoing change, cost reduction, or seeking efficiency improvements. | Stable organizations with consistent operations and predictable expenses. |

| Risk of | Potentially dismissing useful historical data and increasing preparation time. | Risk of perpetuating past inefficiencies and ignoring changing business needs. |

| Examples of use | New projects, startups, departments aiming to cut costs or optimize spending. | Established businesses with routine budgeting cycles and steady expenditure patterns. |

Budget Allocation

Effective budget allocation in business involves strategically distributing financial resources across departments to optimize operational efficiency and drive growth. Data from the U.S. Small Business Administration shows that companies allocating at least 20% of their budget to marketing tend to see revenue growth rates 30% higher than their competitors. Prioritizing investments in technology and employee development can increase productivity by up to 40%, according to McKinsey & Company studies. Continuous monitoring and adjusting budget allocations based on key performance indicators ensures alignment with business goals and maximizes return on investment.

Cost Justification

Cost justification in business involves analyzing expenses to demonstrate the financial benefits of a project or purchase relative to its cost. This process often includes calculating return on investment (ROI), net present value (NPV), and payback period to quantify economic impact. Companies rely on cost justification to secure budget approvals and ensure resource allocation aligns with strategic goals. Effective cost justification combines accurate data and clear, impactful metrics tailored to stakeholder priorities.

Baseline Evaluation

Baseline evaluation in business serves as a critical benchmark for measuring organizational performance and progress over time. It involves collecting initial data on key performance indicators (KPIs) such as revenue, customer satisfaction, and operational efficiency before implementing new strategies or projects. This process enables companies to quantify improvements and identify gaps by comparing future results against the established baseline. Accurate baseline evaluations support informed decision-making and enhance strategic planning in competitive markets.

Resource Optimization

Resource optimization in business involves maximizing the efficient use of assets such as capital, labor, and technology to improve productivity and reduce operational costs. Implementing advanced data analytics and automation tools enables companies to forecast demand accurately and allocate resources dynamically. Industries like manufacturing and logistics benefit significantly by minimizing waste and enhancing supply chain management through resource optimization techniques. Effective resource optimization directly contributes to higher profit margins and sustainable competitive advantages.

Decision-Making Criteria

Effective decision-making in business hinges on analyzing financial performance, market trends, and customer behavior to identify profitable opportunities. Data-driven insights, such as return on investment (ROI), cost-benefit analysis, and risk assessment, guide strategic choices that enhance competitive advantage. Leadership teams prioritize scalability, stakeholder impact, and regulatory compliance to ensure sustainable growth. Integrating advanced analytics and AI tools streamlines complex decisions and improves accuracy.

Source and External Links

Comparing Incremental and Zero-Based Budgeting - Firmbase - Zero-based budgeting starts from zero each period and requires justifying all expenses, promoting cost efficiency, while incremental budgeting adjusts the previous budget by increments, making the choice dependent on company needs rather than a strict better method.

Comparing budgeting techniques (Incremental v ZBB) - ACCA Global - Incremental budgeting uses the previous budget as a base with increments added, whereas zero-based budgeting starts from zero every time requiring all expenditure approvals, which promotes a more comprehensive review.

4 Types of Budgeting Methods and their Pros and Cons - Zero-based budgeting demands justification for every dollar each budget period, increasing accountability and adaptability, but is very time-consuming, while incremental budgeting offers stability and predictability by tweaking prior budgets.

FAQs

What is budgeting in financial management?

Budgeting in financial management is the process of creating a detailed plan that outlines an organization's expected income and expenses over a specific period to allocate resources efficiently and achieve financial goals.

What is the difference between zero-based budgeting and incremental budgeting?

Zero-based budgeting starts from a "zero base" each period, requiring all expenses to be justified and approved, while incremental budgeting adjusts previous budgets by adding or subtracting incremental amounts based on expected changes.

How does zero-based budgeting work?

Zero-based budgeting requires starting each budget cycle from zero, justifying every expense based on current needs rather than relying on previous budgets.

What are the advantages of zero-based budgeting?

Zero-based budgeting improves resource allocation by requiring justification for all expenses, enhances cost control by identifying and eliminating unnecessary spending, encourages efficient use of funds, promotes transparency in financial planning, and aligns budget with organizational goals.

How does incremental budgeting work?

Incremental budgeting allocates funds based on previous budgets, adjusting for expected changes like inflation or new initiatives to set the new budget.

What are the advantages of incremental budgeting?

Incremental budgeting simplifies financial planning by using previous budgets as a baseline, enhances stability and consistency in resource allocation, reduces time and effort in budget preparation, and promotes easier identification of variances and control over expenditures.

Which budgeting method is better for organizations?

Zero-based budgeting is better for organizations as it requires justifying all expenses, promoting cost-efficiency and resource optimization.