Sunk costs represent past expenses that cannot be recovered, such as non-refundable investments in a project or asset. Opportunity costs reflect the potential benefits lost when choosing one alternative over another, guiding decision-makers to evaluate the trade-offs between options. Explore further to understand how distinguishing these costs can improve financial and strategic choices.

Main Difference

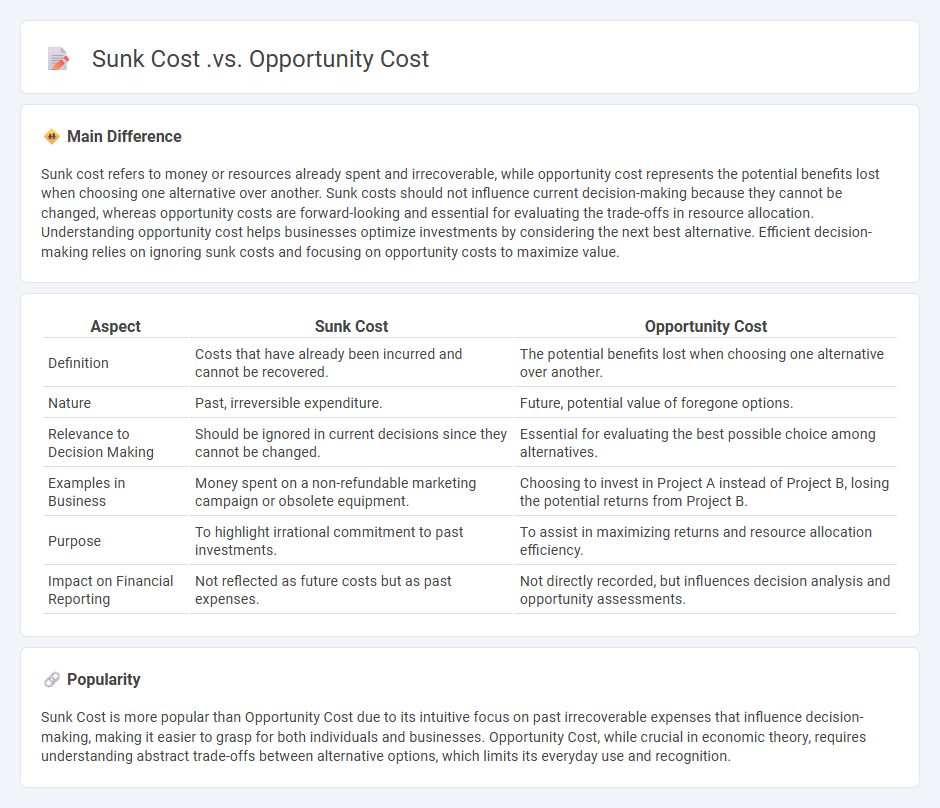

Sunk cost refers to money or resources already spent and irrecoverable, while opportunity cost represents the potential benefits lost when choosing one alternative over another. Sunk costs should not influence current decision-making because they cannot be changed, whereas opportunity costs are forward-looking and essential for evaluating the trade-offs in resource allocation. Understanding opportunity cost helps businesses optimize investments by considering the next best alternative. Efficient decision-making relies on ignoring sunk costs and focusing on opportunity costs to maximize value.

Connection

Sunk cost represents expenses already incurred and irreversible, while opportunity cost signifies the potential benefits missed by choosing one option over another. Both concepts influence economic decision-making by encouraging individuals to ignore past expenses and focus on future gains. Recognizing the relationship between sunk costs and opportunity costs improves resource allocation and minimizes irrational financial behavior.

Comparison Table

| Aspect | Sunk Cost | Opportunity Cost |

|---|---|---|

| Definition | Costs that have already been incurred and cannot be recovered. | The potential benefits lost when choosing one alternative over another. |

| Nature | Past, irreversible expenditure. | Future, potential value of foregone options. |

| Relevance to Decision Making | Should be ignored in current decisions since they cannot be changed. | Essential for evaluating the best possible choice among alternatives. |

| Examples in Business | Money spent on a non-refundable marketing campaign or obsolete equipment. | Choosing to invest in Project A instead of Project B, losing the potential returns from Project B. |

| Purpose | To highlight irrational commitment to past investments. | To assist in maximizing returns and resource allocation efficiency. |

| Impact on Financial Reporting | Not reflected as future costs but as past expenses. | Not directly recorded, but influences decision analysis and opportunity assessments. |

Irrecoverable Expenditure

Irrecoverable expenditure refers to costs that cannot be recovered once incurred, often classified as sunk costs in business accounting. These expenses include marketing campaigns, research and development, or specialized equipment that lose their value if a project is abandoned. Accurate identification of irrecoverable expenditures is crucial for effective decision-making, preventing companies from investing further in unprofitable ventures. Understanding these costs helps businesses allocate resources efficiently and evaluate project viability based on future returns rather than past losses.

Foregone Alternatives

Foregone alternatives in business refer to the potential opportunities or investments that a company sacrifices when choosing one course of action over another. This concept is crucial for assessing opportunity costs, helping businesses allocate resources efficiently to maximize returns. Quantifying foregone alternatives allows firms to evaluate the true cost of decision-making beyond explicit expenditures. Strategic planning incorporates this analysis to optimize profitability and competitive advantage in dynamic markets.

Rational Decision-Making

Rational decision-making in business involves systematically analyzing available data and alternatives to select the most effective course of action that maximizes organizational goals. This process relies on quantitative techniques such as cost-benefit analysis, risk assessment, and predictive modeling to minimize biases and improve decision quality. Key factors include defining clear objectives, gathering accurate information, evaluating options logically, and implementing decisions with measurable outcomes. Companies like Toyota and IBM use rational decision-making models to enhance operational efficiency and strategic planning.

Marginal Analysis

Marginal analysis in business evaluates the additional benefits and costs incurred from producing one more unit of a good or service. It helps firms determine the optimal production level by comparing marginal revenue and marginal cost. Companies use this approach to maximize profit and allocate resources efficiently in competitive markets. Understanding marginal analysis supports better decision-making in pricing, output adjustments, and cost management.

Resource Allocation

Resource allocation in business involves strategically distributing financial, human, and physical assets to optimize operational efficiency and achieve organizational goals. Effective resource allocation enhances productivity by aligning available resources with priority projects based on data-driven analysis and performance metrics. Advanced tools such as enterprise resource planning (ERP) systems and project management software facilitate precise tracking and reallocation of resources in real time. Companies that master resource allocation report up to 20% higher project success rates and improved return on investment (ROI).

Source and External Links

Sunk Cost vs Opportunity Cost - Vintti - Sunk costs are actual amounts spent and unrecoverable from past investments, while opportunity costs represent the potential value lost by choosing one option over an alternative in future decisions.

Sunk Cost vs. Opportunity Cost: What's the Difference? | Indeed.com - Sunk costs are explicit past expenditures that cannot be recovered and do not affect future choices, whereas opportunity costs are implicit, notional costs reflecting the benefits foregone from alternative decisions.

Sunk Cost Vs Opportunity Cost: What's The Difference? - Planergy - Sunk costs have objective, documented values and appear on financial statements but should be ignored in future decisions; opportunity costs are subjective estimates of foregone benefits crucial for guiding future business decisions.

FAQs

What is a sunk cost?

A sunk cost is a past expense that cannot be recovered and should not influence current or future financial decisions.

What is an opportunity cost?

Opportunity cost is the value of the next best alternative foregone when making a decision.

How are sunk cost and opportunity cost different?

Sunk cost refers to past expenses that cannot be recovered, while opportunity cost represents the potential benefits lost when choosing one alternative over another.

Why should sunk costs be ignored in decision making?

Sunk costs should be ignored in decision making because they are past expenses that cannot be recovered and do not affect the future benefits or costs of any decision.

How do opportunity costs impact business choices?

Opportunity costs influence business choices by quantifying the potential benefits lost when selecting one option over alternatives, guiding resource allocation to maximize profitability and strategic advantage.

What are common examples of sunk cost and opportunity cost?

Common examples of sunk cost include non-refundable airline tickets and past research expenses; opportunity cost examples are choosing between working overtime for extra pay or spending time with family, and deciding between investing in stocks or bonds.

Can opportunity cost be measured accurately?

Opportunity cost cannot be measured accurately due to its reliance on subjective estimates and the unpredictability of alternative outcomes.