The Baumol-Tobin model focuses on optimal cash management by balancing transaction costs and interest foregone, emphasizing liquidity preferences in monetary economics. Tobin's Q theory centers on investment decisions, relating a firm's market value to replacement cost, guiding capital allocation in financial markets. Explore the distinctions and applications of these foundational economic models to deepen your understanding.

Main Difference

The Baumol-Tobin model focuses on the optimal cash management by balancing transaction costs and opportunity costs associated with holding money. Tobin's Q theory analyzes investment behavior by comparing the market value of a firm's assets to their replacement cost, guiding firms to invest when Q exceeds one. Baumol-Tobin emphasizes liquidity preference and money demand, whereas Tobin's Q centers on investment decisions and capital market valuations. Both models integrate microeconomic principles but address distinct aspects of financial behavior.

Connection

The Baumol-Tobin model explains the demand for money by balancing transaction costs and interest forgone, while Tobin's Q theory assesses investment decisions based on the market value to replacement cost ratio of capital. Both models incorporate the concept of opportunity cost in financial decision-making: Baumol-Tobin focuses on cash management optimizing liquidity versus interest earnings, whereas Tobin's Q relates to firms optimizing capital investment based on market valuations. Their connection lies in modeling economic agents' behavior in allocating resources to maximize returns under constraints of cost and market signals.

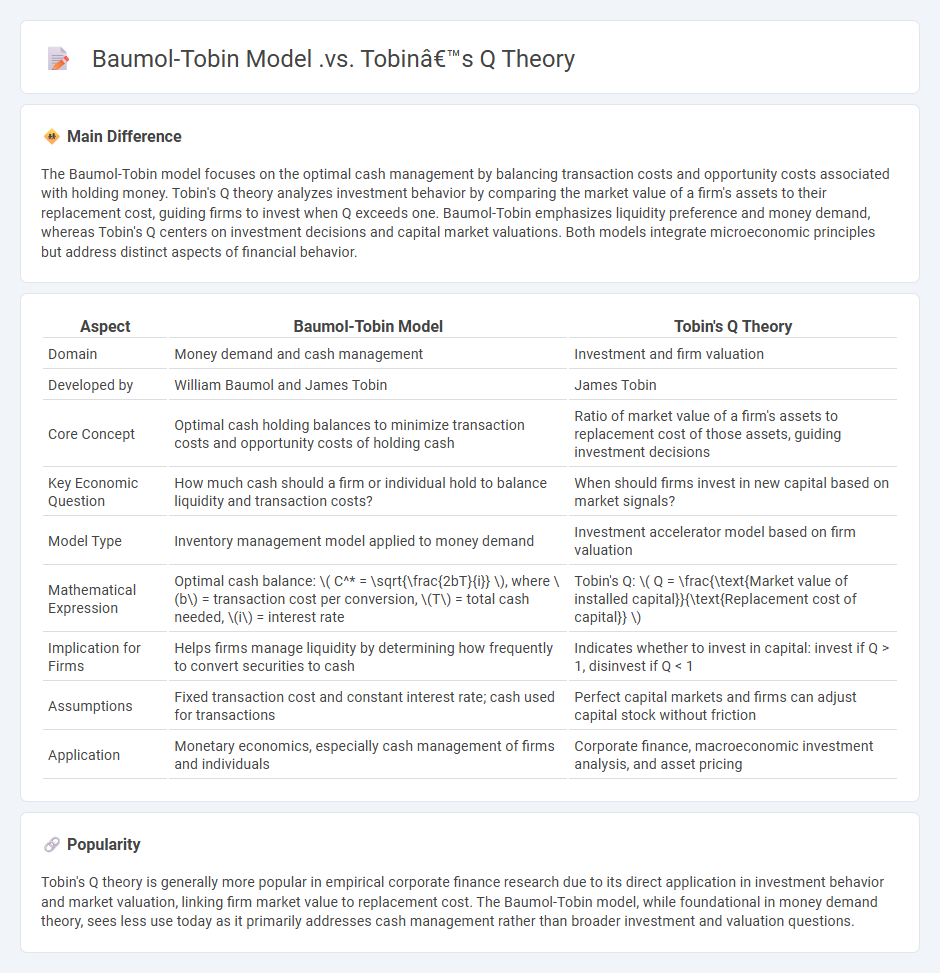

Comparison Table

| Aspect | Baumol-Tobin Model | Tobin's Q Theory |

|---|---|---|

| Domain | Money demand and cash management | Investment and firm valuation |

| Developed by | William Baumol and James Tobin | James Tobin |

| Core Concept | Optimal cash holding balances to minimize transaction costs and opportunity costs of holding cash | Ratio of market value of a firm's assets to replacement cost of those assets, guiding investment decisions |

| Key Economic Question | How much cash should a firm or individual hold to balance liquidity and transaction costs? | When should firms invest in new capital based on market signals? |

| Model Type | Inventory management model applied to money demand | Investment accelerator model based on firm valuation |

| Mathematical Expression | Optimal cash balance: \( C^* = \sqrt{\frac{2bT}{i}} \), where \(b\) = transaction cost per conversion, \(T\) = total cash needed, \(i\) = interest rate | Tobin's Q: \( Q = \frac{\text{Market value of installed capital}}{\text{Replacement cost of capital}} \) |

| Implication for Firms | Helps firms manage liquidity by determining how frequently to convert securities to cash | Indicates whether to invest in capital: invest if Q > 1, disinvest if Q < 1 |

| Assumptions | Fixed transaction cost and constant interest rate; cash used for transactions | Perfect capital markets and firms can adjust capital stock without friction |

| Application | Monetary economics, especially cash management of firms and individuals | Corporate finance, macroeconomic investment analysis, and asset pricing |

Transaction Demand for Money

Transaction demand for money refers to the amount of money households and businesses hold to carry out everyday financial transactions. It primarily depends on factors such as income levels, the overall price level, and the frequency of transactions within an economy. Money held for transaction purposes is typically in liquid form to ensure immediate purchasing power. Understanding transaction demand helps in analyzing money supply policies and their impact on economic activity.

Inventory Theory of Money

The Inventory Theory of Money explains money demand by modeling money as an inventory that facilitates transactions between income receipts and expenditures. Economic agents hold money to minimize the combined costs of converting other assets into cash and the opportunity cost of holding non-interest-bearing money. This theory formalizes liquidity preference by linking money-holding behavior to transaction timing and uncertainty in income flows. Empirical studies show inventory models help predict money demand elasticity influenced by interest rates and income volatility.

Market Value vs. Replacement Cost

Market value reflects the price at which an asset can be bought or sold in a competitive marketplace, determined by supply and demand factors. Replacement cost measures the expense to reproduce or replace an asset with a similar one at current prices, considering materials, labor, and overhead. In economics, market value often fluctuates due to external economic conditions, while replacement cost provides a baseline for asset valuation and insurance purposes. Understanding both concepts is crucial for investment decisions, asset management, and financial reporting accuracy.

Liquidity Preference

Liquidity preference refers to the demand for money as an asset held for transactions, precautionary, and speculative purposes within an economy. John Maynard Keynes introduced this concept in his 1936 work, "The General Theory of Employment, Interest, and Money," linking it to the determination of interest rates through the money supply and demand balance. Changes in liquidity preference influence short-term interest rates, impacting investment and consumption decisions. Central banks monitor liquidity preference to implement effective monetary policies that stabilize economic activity.

Investment Decision Criterion

Investment decision criterion involves evaluating projects based on metrics like Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to determine their profitability and risk. NPV calculates the difference between the present value of cash inflows and outflows, guiding firms toward value-maximizing investments. IRR identifies the discount rate at which the project's NPV equals zero, serving as a benchmark for acceptable returns. The Payback Period measures the time required to recover the initial investment, emphasizing liquidity and risk exposure.

Source and External Links

Baumol-Tobin model - Wikipedia - The Baumol-Tobin model explains the transactions demand for money as a tradeoff between liquidity (ease of carrying out transactions) and the interest forgone by holding money instead of interest-bearing assets, focusing on income, nominal interest rate, and transaction costs; Tobin's Q theory, by contrast, relates to investment decisions based on the ratio (Q) of market value to asset replacement cost, linking investment with firm valuation rather than money demand.

Keynesian Theory of Demand for Money, Baumol-Tobin Transaction Approach - The Baumol-Tobin model specifically addresses how individuals optimize their money holdings for transactions considering interest rates and transaction costs, whereas Tobin's Q theory concerns the investment behavior of firms by linking investment to the market valuation of firms relative to replacement costs of capital.

JAMES TOBIN - Tobin contributed to both models, with the Baumol-Tobin model focusing on individual money demand driven by transaction and precautionary motives influenced by interest rates, while Tobin's Q theory addresses the relationship between a firm's stock market valuation and its investment decisions, confirming the link between the Q coefficient and investment levels.

FAQs

What is the Baumol-Tobin model?

The Baumol-Tobin model explains the optimal cash management strategy by balancing transaction costs and the opportunity cost of holding non-interest-bearing cash.

What is Tobin’s Q theory?

Tobin's Q theory measures the ratio of a firm's market value to the replacement cost of its assets, indicating investment attractiveness when Q is greater than 1.

How do the Baumol-Tobin model and Tobin’s Q theory differ?

The Baumol-Tobin model explains cash management optimizing transaction and holding costs, while Tobin's Q theory assesses firm investment decisions based on the market value-to-replacement cost ratio of capital.

What are the main assumptions in the Baumol-Tobin model?

The Baumol-Tobin model assumes a fixed transaction cost for converting bonds to cash, a constant interest rate, a predictable steady cash expenditure rate, and instantaneous transactions with no risk or uncertainty.

What are the implications of Tobin’s Q for investment decisions?

Tobin's Q ratio, when greater than 1, signals that a firm's market value exceeds replacement costs, encouraging increased investment; if less than 1, it suggests undervaluation, leading firms to reduce investment.

How do both theories relate to money demand and investment behavior?

The Keynesian theory links money demand to interest rates affecting investment, while the Classical theory views money demand as a function of income with investment driven by savings and capital return.

Why are these models important in economic analysis?

Economic models are important because they simplify complex real-world economic processes, enabling analysts to predict outcomes, evaluate policies, and understand relationships between variables.