The Fisher separation theorem explains how investment decisions are independent of individual preferences, focusing solely on maximizing firm value through efficient capital allocation. The Modigliani-Miller theorem highlights the irrelevance of a firm's capital structure in determining its overall value under perfect market conditions. Explore deeper insights into their economic implications and applications in corporate finance.

Main Difference

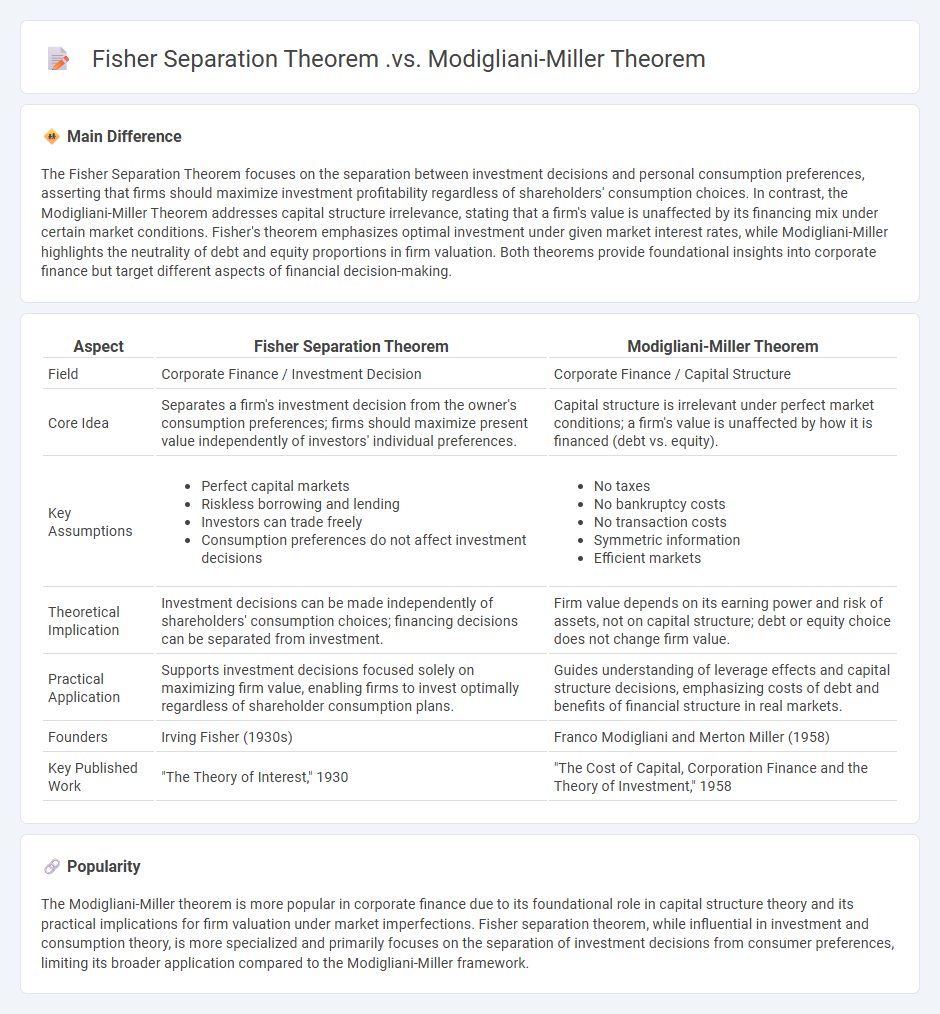

The Fisher Separation Theorem focuses on the separation between investment decisions and personal consumption preferences, asserting that firms should maximize investment profitability regardless of shareholders' consumption choices. In contrast, the Modigliani-Miller Theorem addresses capital structure irrelevance, stating that a firm's value is unaffected by its financing mix under certain market conditions. Fisher's theorem emphasizes optimal investment under given market interest rates, while Modigliani-Miller highlights the neutrality of debt and equity proportions in firm valuation. Both theorems provide foundational insights into corporate finance but target different aspects of financial decision-making.

Connection

The Fisher separation theorem and the Modigliani-Miller theorem both emphasize the independence of corporate financial decisions from personal preferences or market imperfections. Fisher's theorem separates investment decisions from consumption preferences by assuming perfect capital markets, while Modigliani-Miller extends this concept by asserting that a firm's value remains unaffected by its capital structure under ideal conditions. Both theorems rely on the premise of efficient markets and rational investors, reinforcing the principle that financing choices do not influence the fundamental valuation of investments.

Comparison Table

| Aspect | Fisher Separation Theorem | Modigliani-Miller Theorem |

|---|---|---|

| Field | Corporate Finance / Investment Decision | Corporate Finance / Capital Structure |

| Core Idea | Separates a firm's investment decision from the owner's consumption preferences; firms should maximize present value independently of investors' individual preferences. | Capital structure is irrelevant under perfect market conditions; a firm's value is unaffected by how it is financed (debt vs. equity). |

| Key Assumptions |

|

|

| Theoretical Implication | Investment decisions can be made independently of shareholders' consumption choices; financing decisions can be separated from investment. | Firm value depends on its earning power and risk of assets, not on capital structure; debt or equity choice does not change firm value. |

| Practical Application | Supports investment decisions focused solely on maximizing firm value, enabling firms to invest optimally regardless of shareholder consumption plans. | Guides understanding of leverage effects and capital structure decisions, emphasizing costs of debt and benefits of financial structure in real markets. |

| Founders | Irving Fisher (1930s) | Franco Modigliani and Merton Miller (1958) |

| Key Published Work | "The Theory of Interest," 1930 | "The Cost of Capital, Corporation Finance and the Theory of Investment," 1958 |

Investment and Financing Decisions

Investment and financing decisions are critical components in corporate economics, directly impacting a firm's capital structure and growth potential. Investment decisions involve allocating resources to projects expected to yield returns exceeding the cost of capital, often evaluated using methods such as net present value (NPV) and internal rate of return (IRR). Financing decisions determine the optimal mix of debt and equity to minimize the weighted average cost of capital (WACC) while maintaining financial flexibility and risk management. Efficient decision-making in these areas enhances shareholder value and supports sustainable economic development.

Capital Structure Irrelevance

Capital structure irrelevance, a principle central to modern corporate finance, asserts that a firm's value remains unaffected by its debt-to-equity ratio under perfect market conditions. This theory, pioneered by Franco Modigliani and Merton Miller in 1958, assumes no taxes, bankruptcy costs, or asymmetric information, ensuring that financing decisions do not alter total firm value. Empirical studies challenge these assumptions by highlighting factors such as tax shields, agency costs, and market imperfections that influence optimal capital structure. Understanding capital structure irrelevance is vital for economists analyzing firm behavior and financial decision-making in real-world markets.

Firm Value Maximization

Firm value maximization focuses on increasing a company's market value by optimizing financial performance, capital structure, and investment decisions. Key metrics include market capitalization, discounted cash flows (DCF), and return on invested capital (ROIC). Strategies involve enhancing operational efficiency, managing risk, and maximizing shareholder wealth through dividends and stock buybacks. Understanding economic factors such as market competition, interest rates, and inflation is crucial for sustained value creation.

Risk and Return

Risk and return are fundamental concepts in economics, representing the trade-off between potential reward and the possibility of loss in investments. Higher risk investments, such as stocks or commodities, typically offer greater expected returns to compensate investors for bearing uncertainty. Conversely, low-risk assets like government bonds provide more stable but generally lower returns. Understanding the relationship between risk and return guides decision-making in portfolio management, asset allocation, and economic forecasting.

Separation Principle

The Separation Principle in economics states that investment decisions can be made independently of an investor's consumption preferences or personal utility functions. This principle is fundamental to modern portfolio theory, allowing firms to separate investment policy from financing decisions. It implies that firms should focus solely on maximizing value through optimal investment strategies, while investors can achieve their desired risk-return profile through personal portfolio adjustments. Real-world applications include capital budgeting and efficient market hypothesis frameworks.

Source and External Links

Virginia Law & Business Review - Fisher's separation theorem establishes that, in a perfect market, a firm's value is independent of shareholder consumption preferences and financing decisions, but this is a foundational concept for the later Modigliani-Miller theorem, which directly shows that a firm's value is unaffected by its capital structure (debt vs. equity ratio) under similar idealized conditions.

Atlantis Press - Fisher's separation theorem states that a firm's investment decisions (i.e., which projects to undertake) are separate from both shareholder preferences and the firm's financing choices, while the Modigliani-Miller theorem extends this logic to show that, in perfect markets, the way a firm finances itself (debt, equity, or cash) does not affect its overall value.

Fisher separation theorem - Wikipedia - The Fisher separation theorem asserts that corporate investment decisions should aim solely to maximize the firm's present value, independent of owners' consumption preferences or financing methods, whereas the Modigliani-Miller theorem further generalizes this result, stating that, in frictionless markets, the firm's total value is unaffected by its financing mix (debt or equity).

FAQs

What is the Fisher Separation Theorem?

The Fisher Separation Theorem states that a firm's investment decision is independent of its owner's consumption preferences and is determined solely by maximizing the firm's net present value, separating investment decisions from financing and consumption choices.

What is the Modigliani-Miller Theorem?

The Modigliani-Miller Theorem states that, in a perfect market without taxes, bankruptcy costs, or asymmetric information, a firm's value is unaffected by its capital structure or debt-equity mix.

How does the Fisher Separation Theorem relate to investment and consumption decisions?

The Fisher Separation Theorem states that a firm's investment decision is independent of the owner's consumption preferences and can be made solely based on maximizing investment returns, while consumption decisions are made separately by individual investors through borrowing or lending at the market interest rate.

What does the Modigliani-Miller Theorem say about capital structure?

The Modigliani-Miller Theorem states that in a perfect market without taxes, bankruptcy costs, or asymmetric information, a firm's capital structure is irrelevant to its overall value and cost of capital.

How do these theorems assume market conditions and perfect information?

These theorems assume market conditions with perfect competition, complete information, no transaction costs, and rational agents to guarantee equilibrium outcomes.

What are the key similarities and differences between the two theorems?

The key similarity between the two theorems is that both establish foundational principles in their respective fields, providing critical insights and formal proofs. The key difference lies in their application: one theorem addresses properties of continuous functions in real analysis, while the other focuses on discrete structures in combinatorics.

Why are these theorems important for modern financial theory?

These theorems provide the mathematical foundation for asset pricing, risk management, and portfolio optimization in modern financial theory.