Pigovian tax imposes a direct fee on activities generating negative externalities, effectively internalizing social costs to reduce harmful behaviors like pollution. Coase theorem highlights how private negotiation between parties can resolve externalities efficiently, provided property rights are well-defined and transaction costs are low. Explore more to understand the differences and applications of Pigovian tax and Coase theorem in addressing market failures.

Main Difference

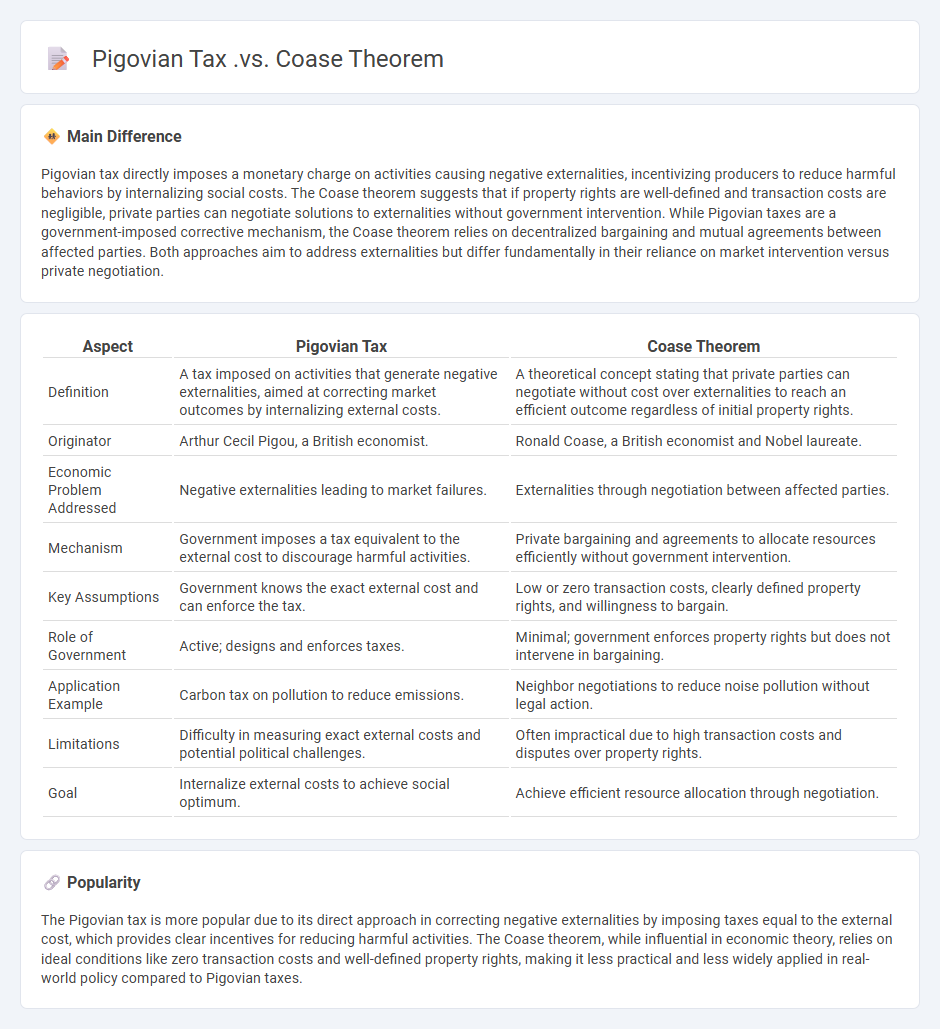

Pigovian tax directly imposes a monetary charge on activities causing negative externalities, incentivizing producers to reduce harmful behaviors by internalizing social costs. The Coase theorem suggests that if property rights are well-defined and transaction costs are negligible, private parties can negotiate solutions to externalities without government intervention. While Pigovian taxes are a government-imposed corrective mechanism, the Coase theorem relies on decentralized bargaining and mutual agreements between affected parties. Both approaches aim to address externalities but differ fundamentally in their reliance on market intervention versus private negotiation.

Connection

Pigovian tax and Coase theorem both address externalities by promoting efficient resource allocation. Pigovian tax internalizes external costs through government-imposed taxes equal to the external damage, incentivizing producers to reduce negative externalities. The Coase theorem emphasizes private negotiation between affected parties to achieve efficient outcomes without government intervention, provided property rights are well-defined and transaction costs are low.

Comparison Table

| Aspect | Pigovian Tax | Coase Theorem |

|---|---|---|

| Definition | A tax imposed on activities that generate negative externalities, aimed at correcting market outcomes by internalizing external costs. | A theoretical concept stating that private parties can negotiate without cost over externalities to reach an efficient outcome regardless of initial property rights. |

| Originator | Arthur Cecil Pigou, a British economist. | Ronald Coase, a British economist and Nobel laureate. |

| Economic Problem Addressed | Negative externalities leading to market failures. | Externalities through negotiation between affected parties. |

| Mechanism | Government imposes a tax equivalent to the external cost to discourage harmful activities. | Private bargaining and agreements to allocate resources efficiently without government intervention. |

| Key Assumptions | Government knows the exact external cost and can enforce the tax. | Low or zero transaction costs, clearly defined property rights, and willingness to bargain. |

| Role of Government | Active; designs and enforces taxes. | Minimal; government enforces property rights but does not intervene in bargaining. |

| Application Example | Carbon tax on pollution to reduce emissions. | Neighbor negotiations to reduce noise pollution without legal action. |

| Limitations | Difficulty in measuring exact external costs and potential political challenges. | Often impractical due to high transaction costs and disputes over property rights. |

| Goal | Internalize external costs to achieve social optimum. | Achieve efficient resource allocation through negotiation. |

Externalities

Externalities in economics refer to the positive or negative effects of a transaction experienced by third parties not directly involved in the market exchange. Negative externalities, such as pollution from manufacturing plants, result in social costs that exceed private costs, leading to market inefficiencies. Positive externalities, like the benefits of education or vaccination, generate social benefits that are not reflected in market prices. Governments often intervene through taxes, subsidies, or regulations to correct these market failures and promote social welfare.

Market Failure

Market failure occurs when the allocation of goods and services by a free market is not efficient, leading to a net social welfare loss. Common causes include externalities like pollution, public goods such as national defense, information asymmetry, and market power concentration through monopolies. Government intervention through policies like taxation, subsidies, or regulation aims to correct these inefficiencies and improve resource allocation. Studies show that unaddressed market failures can reduce economic growth and increase inequality across societies.

Pigovian Tax

A Pigovian tax is a levy imposed on activities generating negative externalities, aimed at correcting market inefficiencies by internalizing social costs. This tax aligns private costs with social costs, incentivizing producers and consumers to reduce harmful behaviors such as pollution or congestion. Developed by economist Arthur Pigou in the early 20th century, it is widely applied in environmental economics to address issues like carbon emissions and traffic congestion. Empirical studies demonstrate that appropriately set Pigovian taxes can effectively reduce externalities and promote sustainable economic outcomes.

Property Rights

Property rights in economics define the legal ownership and control over resources, enabling efficient allocation through market mechanisms. Well-defined property rights reduce transaction costs and mitigate conflicts, fostering investment and economic growth. Empirical studies show countries with secure property rights experience higher GDP per capita and innovation rates. Enforcement mechanisms and clear legal frameworks are critical for sustaining property rights and supporting economic development.

Transaction Costs

Transaction costs in economics refer to the expenses incurred during the process of buying or selling goods and services, beyond the price of the product itself. These costs include search and information costs, bargaining and decision costs, and policing and enforcement costs. High transaction costs can hinder market efficiency by limiting the frequency or size of trades, impacting overall economic welfare. Understanding and minimizing transaction costs is crucial for improving market functionality and reducing economic friction.

Source and External Links

Coase versus Pigou: A Still Difficult Debate after Fifty Years - SSRN - Coase emphasizes efficiency evaluation in total and voluntary negotiations to enhance welfare, while Pigou advocates government-imposed taxes (Pigovian taxes) to correct externalities and achieve marginal efficiency.

Coase theorem - Wikipedia - The Coase theorem argues that with clear property rights and zero transaction costs, private negotiation can solve externalities more efficiently than Pigovian taxes, although combining bargaining with Pigovian taxation may improve outcomes under some conditions.

Difference between Coasean and Pigouvian Solution to an Environmental Problem - UK Essays - Pigouvian solutions rely on government intervention via taxes to internalize external costs, while Coasean solutions focus on voluntary bargaining based on clearly defined property rights, with Coase criticizing Pigouvian taxes especially when transaction costs are low or property rights are disputed.

FAQs

What is a Pigovian tax?

A Pigovian tax is a tax imposed on activities that generate negative externalities, such as pollution, to correct market inefficiencies and align private costs with social costs.

What is the Coase theorem?

The Coase theorem states that if property rights are well-defined and transaction costs are negligible, private parties can negotiate to resolve externalities efficiently without government intervention.

How do Pigovian taxes address externalities?

Pigovian taxes address externalities by imposing a tax equal to the external cost of a negative externality, incentivizing producers or consumers to reduce harmful activities and align private costs with social costs.

How does the Coase theorem resolve externalities?

The Coase theorem resolves externalities by asserting that if property rights are well-defined and transaction costs are negligible, private parties can negotiate mutually beneficial agreements that internalize externalities and allocate resources efficiently.

What are the advantages of Pigovian taxes over the Coase theorem?

Pigovian taxes effectively internalize externalities by pricing negative external costs, ensuring efficient resource allocation without requiring clear property rights or costly negotiations, unlike the Coase theorem which depends on well-defined property rights and low transaction costs for bargaining.

What are the limitations of the Coase theorem compared to Pigovian taxes?

The Coase theorem's limitations include the necessity of clearly defined property rights, low transaction costs, and few parties involved, while Pigovian taxes directly internalize externalities regardless of transaction costs or number of stakeholders.

When is a Pigovian tax preferable to the Coase theorem?

A Pigovian tax is preferable to the Coase theorem when transaction costs are high, property rights are difficult to define or enforce, and there are multiple affected parties.