Microeconomic theory analyzes individual agents' behaviors and decision-making processes in markets, focusing on supply, demand, and price mechanisms. Macroeconomic theory examines aggregate economic phenomena such as inflation, unemployment, and GDP growth to understand overall economic health and policy impacts. Explore more to uncover how these complementary frameworks shape economic insights and strategies.

Main Difference

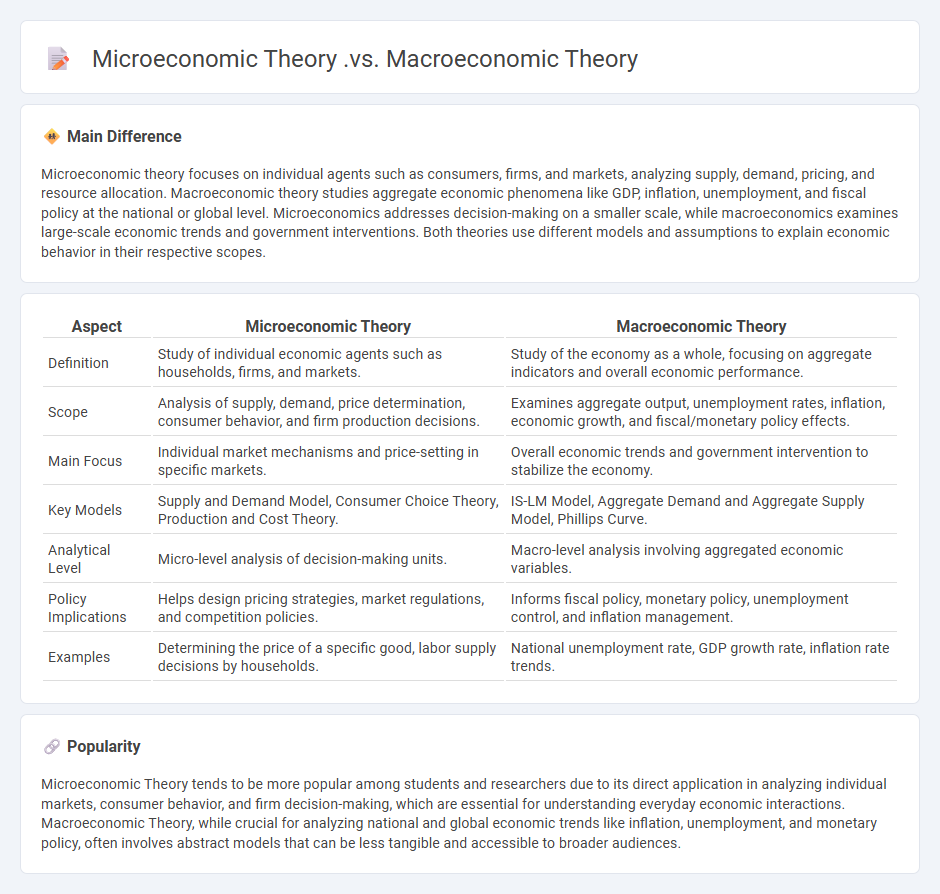

Microeconomic theory focuses on individual agents such as consumers, firms, and markets, analyzing supply, demand, pricing, and resource allocation. Macroeconomic theory studies aggregate economic phenomena like GDP, inflation, unemployment, and fiscal policy at the national or global level. Microeconomics addresses decision-making on a smaller scale, while macroeconomics examines large-scale economic trends and government interventions. Both theories use different models and assumptions to explain economic behavior in their respective scopes.

Connection

Microeconomic theory, which analyzes individual agents such as households and firms, provides the foundational behavior models that aggregate to macroeconomic phenomena like GDP growth, inflation, and unemployment. Macroeconomic theory uses these aggregate relationships to study overall economic trends, policy impacts, and market fluctuations at the national or global level. The interaction between micro-level decisions and macro-level outcomes creates a dynamic framework that links consumer preferences and firm production with fiscal and monetary policy effects.

Comparison Table

| Aspect | Microeconomic Theory | Macroeconomic Theory |

|---|---|---|

| Definition | Study of individual economic agents such as households, firms, and markets. | Study of the economy as a whole, focusing on aggregate indicators and overall economic performance. |

| Scope | Analysis of supply, demand, price determination, consumer behavior, and firm production decisions. | Examines aggregate output, unemployment rates, inflation, economic growth, and fiscal/monetary policy effects. |

| Main Focus | Individual market mechanisms and price-setting in specific markets. | Overall economic trends and government intervention to stabilize the economy. |

| Key Models | Supply and Demand Model, Consumer Choice Theory, Production and Cost Theory. | IS-LM Model, Aggregate Demand and Aggregate Supply Model, Phillips Curve. |

| Analytical Level | Micro-level analysis of decision-making units. | Macro-level analysis involving aggregated economic variables. |

| Policy Implications | Helps design pricing strategies, market regulations, and competition policies. | Informs fiscal policy, monetary policy, unemployment control, and inflation management. |

| Examples | Determining the price of a specific good, labor supply decisions by households. | National unemployment rate, GDP growth rate, inflation rate trends. |

Individual Decision-Making

Individual decision-making involves the cognitive process where a person evaluates information, weighs alternatives, and selects a course of action to resolve uncertainty or achieve goals. This process is influenced by factors such as personal preferences, risk tolerance, cognitive biases, and available information. Techniques like cost-benefit analysis, heuristics, and decision trees assist individuals in structuring and optimizing their choices. Understanding psychological theories, including prospect theory and bounded rationality, enhances the effectiveness of individual decision-making.

Aggregate Economy

The aggregate economy encompasses the total economic activity within a nation, including the sum of all goods and services produced, known as Gross Domestic Product (GDP). Key indicators such as unemployment rates, inflation, consumer spending, and investment levels are crucial for assessing economic health. Central banks use monetary policies like interest rate adjustments to influence aggregate demand and stabilize the economy. Economic growth is driven by factors such as technological innovation, labor force expansion, and capital investment.

Market Equilibrium

Market equilibrium occurs when the quantity of goods supplied matches the quantity demanded at a specific price. This balance ensures no surplus or shortage exists, stabilizing the market. Shifts in supply or demand curves, influenced by factors like consumer preferences or production costs, can disrupt this equilibrium, prompting price adjustments. Understanding equilibrium helps predict market responses and optimize resource allocation efficiently.

Fiscal Policy

Fiscal policy involves government decisions on taxation and public spending to influence a country's economy. Governments use fiscal measures to manage economic growth, control inflation, and reduce unemployment rates. Key tools include adjusting income tax rates, increasing public infrastructure investments, and providing social welfare programs. Effective fiscal policy aims to stabilize the economy by balancing budget deficits and surpluses according to economic conditions.

Resource Allocation

Effective resource allocation maximizes organizational efficiency by strategically distributing financial, human, and technological assets to high-impact projects. Tools like project management software and data analytics enable precise tracking and optimization of resources, reducing waste and enhancing productivity. Agile methodologies support adaptive reallocation in dynamic environments, ensuring alignment with shifting business priorities. Transparent communication and continuous performance evaluation foster accountability and improve decision-making across departments.

Source and External Links

Micro and Macro: The Economic Divide - Microeconomics examines the decisions and behavior of individual consumers and firms, focusing on specific markets and issues like pricing and competition, while macroeconomics analyzes broad economic aggregates such as national income, inflation, and growth, looking at the economy as a whole.

1.2 Microeconomics and Macroeconomics - Principles of Economics - Microeconomics studies the actions of individual agents like households and businesses, whereas macroeconomics looks at the entire economy, addressing issues like unemployment, inflation, and national production.

Macro, Micro and Econometrics | University of Bath - Microeconomics deals with the economic decisions of individual consumers and companies, while macroeconomics uses a top-down approach to analyze overall economic trends and inform government policy and strategic decision-making.

FAQs

What is economics?

Economics is the social science that studies the production, distribution, and consumption of goods and services to understand how individuals, businesses, and governments allocate scarce resources.

What is microeconomic theory?

Microeconomic theory studies how individuals and firms make decisions regarding resource allocation, production, and consumption within markets.

What is macroeconomic theory?

Macroeconomic theory studies the behavior, structure, and performance of an economy as a whole, focusing on aggregate indicators like GDP, inflation, unemployment, and fiscal policies.

How does microeconomic theory differ from macroeconomic theory?

Microeconomic theory analyzes individual agents' behaviors and market mechanisms, focusing on supply and demand, pricing, and resource allocation; macroeconomic theory examines aggregate economic indicators like GDP, inflation, unemployment, and fiscal policy to understand overall economic growth and stability.

What topics does microeconomic theory focus on?

Microeconomic theory focuses on topics such as consumer behavior, demand and supply analysis, production and costs, market structures, price determination, labor economics, and resource allocation.

What issues does macroeconomic theory address?

Macroeconomic theory addresses issues such as inflation, unemployment, economic growth, aggregate demand and supply, fiscal and monetary policy, business cycles, and international trade balance.

Why is understanding both theories important?

Understanding both theories is important because it provides a comprehensive perspective, enables critical comparison, and enhances problem-solving by integrating diverse insights.