Convertible bonds offer investors the option to convert debt into equity shares, providing potential upside from stock price appreciation while maintaining fixed income benefits. Callable bonds grant issuers the right to redeem the bond before maturity, often to capitalize on declining interest rates, which can limit investor returns. Explore the key differences, benefits, and risks of convertible and callable bonds to make informed investment decisions.

Main Difference

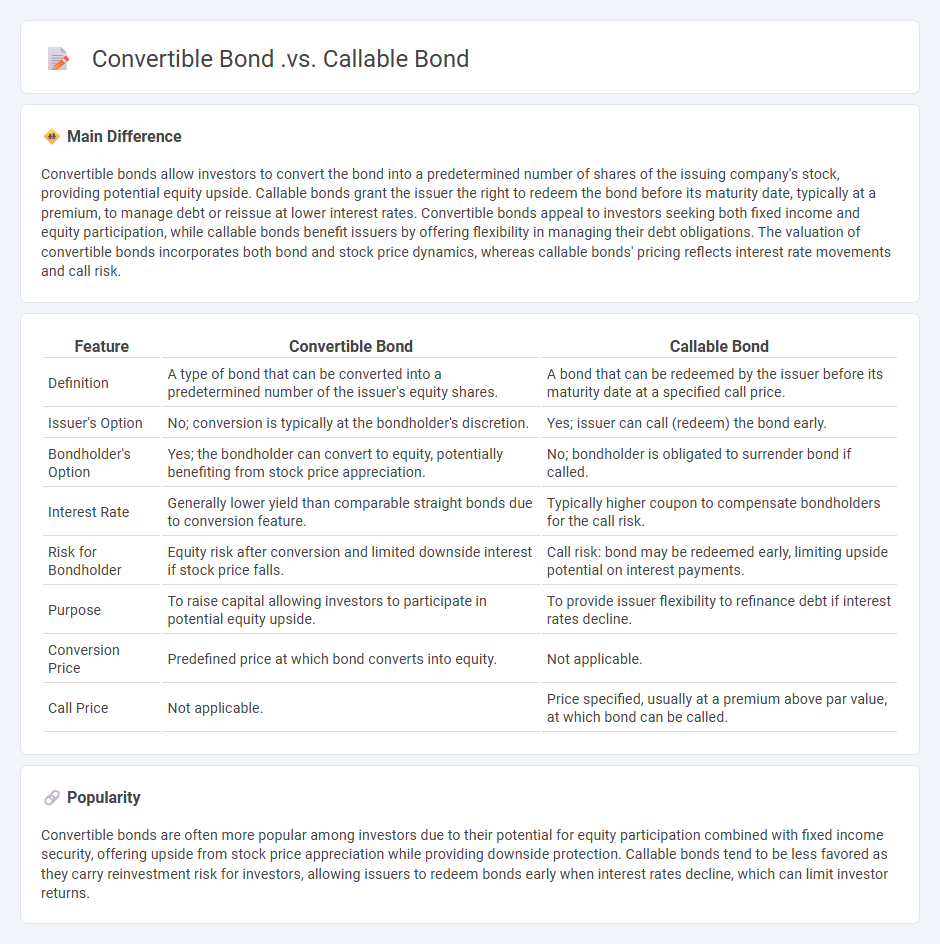

Convertible bonds allow investors to convert the bond into a predetermined number of shares of the issuing company's stock, providing potential equity upside. Callable bonds grant the issuer the right to redeem the bond before its maturity date, typically at a premium, to manage debt or reissue at lower interest rates. Convertible bonds appeal to investors seeking both fixed income and equity participation, while callable bonds benefit issuers by offering flexibility in managing their debt obligations. The valuation of convertible bonds incorporates both bond and stock price dynamics, whereas callable bonds' pricing reflects interest rate movements and call risk.

Connection

Convertible bonds and callable bonds share the characteristic of embedded options that provide flexibility to issuers and investors; a convertible bond includes a conversion option allowing bondholders to convert debt into equity, while a callable bond grants the issuer the right to redeem the bond before maturity, typically to refinance at lower interest rates. Both types of bonds impact valuation and risk profiles, as conversion features can dilute equity and affect bond price volatility, whereas call provisions introduce reinvestment risk and limit price appreciation. Investors assess yield spreads, conversion ratios, call dates, and issuer credit quality to evaluate the trade-offs between potential upside and call risk inherent in these hybrid securities.

Comparison Table

| Feature | Convertible Bond | Callable Bond |

|---|---|---|

| Definition | A type of bond that can be converted into a predetermined number of the issuer's equity shares. | A bond that can be redeemed by the issuer before its maturity date at a specified call price. |

| Issuer's Option | No; conversion is typically at the bondholder's discretion. | Yes; issuer can call (redeem) the bond early. |

| Bondholder's Option | Yes; the bondholder can convert to equity, potentially benefiting from stock price appreciation. | No; bondholder is obligated to surrender bond if called. |

| Interest Rate | Generally lower yield than comparable straight bonds due to conversion feature. | Typically higher coupon to compensate bondholders for the call risk. |

| Risk for Bondholder | Equity risk after conversion and limited downside interest if stock price falls. | Call risk: bond may be redeemed early, limiting upside potential on interest payments. |

| Purpose | To raise capital allowing investors to participate in potential equity upside. | To provide issuer flexibility to refinance debt if interest rates decline. |

| Conversion Price | Predefined price at which bond converts into equity. | Not applicable. |

| Call Price | Not applicable. | Price specified, usually at a premium above par value, at which bond can be called. |

Conversion Feature

Conversion feature in finance refers to the option embedded in convertible securities, such as convertible bonds or preferred shares, allowing investors to exchange these instruments for a predetermined number of common shares. This feature enhances the appeal of hybrid securities by providing potential upside participation in the issuer's equity while offering fixed income benefits. The conversion ratio, conversion price, and conversion period are critical terms defining the mechanics and timing of conversion. Investors analyze these parameters alongside market conditions to optimize valuation and returns from convertible instruments.

Call Provision

Call provision in finance refers to a feature in bonds or preferred stocks that allows the issuer to redeem the security before its maturity date, typically at a specified call price. This provision helps issuers manage debt more efficiently by refinancing at lower interest rates during declining rate environments. Investors face reinvestment risk since the security may be called away when interest rates fall, potentially limiting income. Call provisions are common in corporate bonds and callable preferred shares, influencing yield and pricing dynamics.

Investor Flexibility

Investor flexibility enhances portfolio management by allowing adjustments to asset allocations in response to changing market conditions and personal financial goals. This adaptability supports risk mitigation and capitalizes on emerging investment opportunities, improving overall returns. Flexible investment strategies incorporate diverse financial instruments including stocks, bonds, and alternative assets tailored to investor preferences. Institutional investors and individual traders alike benefit from flexibility to optimize performance across different economic cycles.

Issuer Control

Issuer control in finance refers to the authority and governance exercised by a company or entity that issues securities such as stocks or bonds. This control influences decisions regarding the terms, pricing, and timing of security issuance, impacting capital structure and investor relations. Regulatory frameworks from bodies like the Securities and Exchange Commission (SEC) impose specific disclosure and compliance requirements on issuers to protect market integrity. Effective issuer control ensures transparent communication with shareholders and the alignment of issuance strategies with corporate financial goals.

Risk-Return Profile

The risk-return profile in finance evaluates the potential returns of an investment relative to the level of risk it carries, guiding investors in portfolio allocation and decision-making. Investments with higher expected returns, such as stocks or high-yield bonds, typically present greater volatility and risk of loss compared to safer options like government bonds or savings accounts. Modern Portfolio Theory quantifies risk using metrics like standard deviation and beta, helping investors balance risk tolerance with return objectives. Understanding the risk-return tradeoff is essential for optimizing asset selection and achieving long-term financial goals.

Source and External Links

Bond Features Explained: Callable, Puttable, and Convertible Bonds - A callable bond lets the issuer redeem the bond early to refinance if rates drop, posing reinvestment risk to investors, while a convertible bond can be converted into stock, offering investors upside potential with usually lower coupons.

Types of Bonds - Financial Accounting - Convertible bonds can be converted into equity at a preset price and time, often used in startups, whereas callable bonds give issuers the right to repurchase the bond early at a set price, usually offering higher coupons due to added issuer flexibility.

Bond Basics: Pick Your Type - Convertible bonds can be exchanged for common stock at a fixed ratio, providing a mix of debt and equity features; callable bonds allow issuers to call back bonds before maturity, helping manage interest costs but adding risk for investors.

FAQs

What is a convertible bond?

A convertible bond is a hybrid debt instrument that allows investors to convert the bond into a predetermined number of the issuing company's common shares, combining fixed-income features with equity participation potential.

What is a callable bond?

A callable bond is a debt security that allows the issuer to redeem the bond before its maturity date, typically at a specified call price.

How does a convertible bond work?

A convertible bond is a fixed-income security that can be exchanged for a predetermined number of the issuer's common shares, allowing investors to benefit from potential equity upside while receiving regular interest payments.

How does a callable bond function?

A callable bond allows the issuer to redeem the bond before its maturity date at a specified call price, giving the issuer flexibility to refinance debt if interest rates decline.

What are the main differences between convertible and callable bonds?

Convertible bonds can be converted into a predetermined number of the issuer's shares, offering potential equity upside to investors, while callable bonds allow the issuer to redeem the bonds before maturity at a specified call price, giving the issuer interest cost control.

What are the advantages of investing in convertible bonds?

Convertible bonds offer the advantage of fixed-income returns with the potential for equity appreciation, providing downside protection through bond features and upside gains if the stock price rises.

What are the risks associated with callable bonds?

Callable bonds carry reinvestment risk, as issuers may redeem them when interest rates drop, forcing investors to reinvest at lower yields; they also have price appreciation limits and higher yield volatility.