Tranche and slice are financial terms used to describe different portions of structured finance products, particularly in asset-backed securities. Tranches represent segments of debt or securities categorized by risk level, payment priority, and interest rates, while slices refer to divisions of cash flow streams allocated to investors. Explore further to understand the distinctions and applications of tranches and slices in investment portfolios.

Main Difference

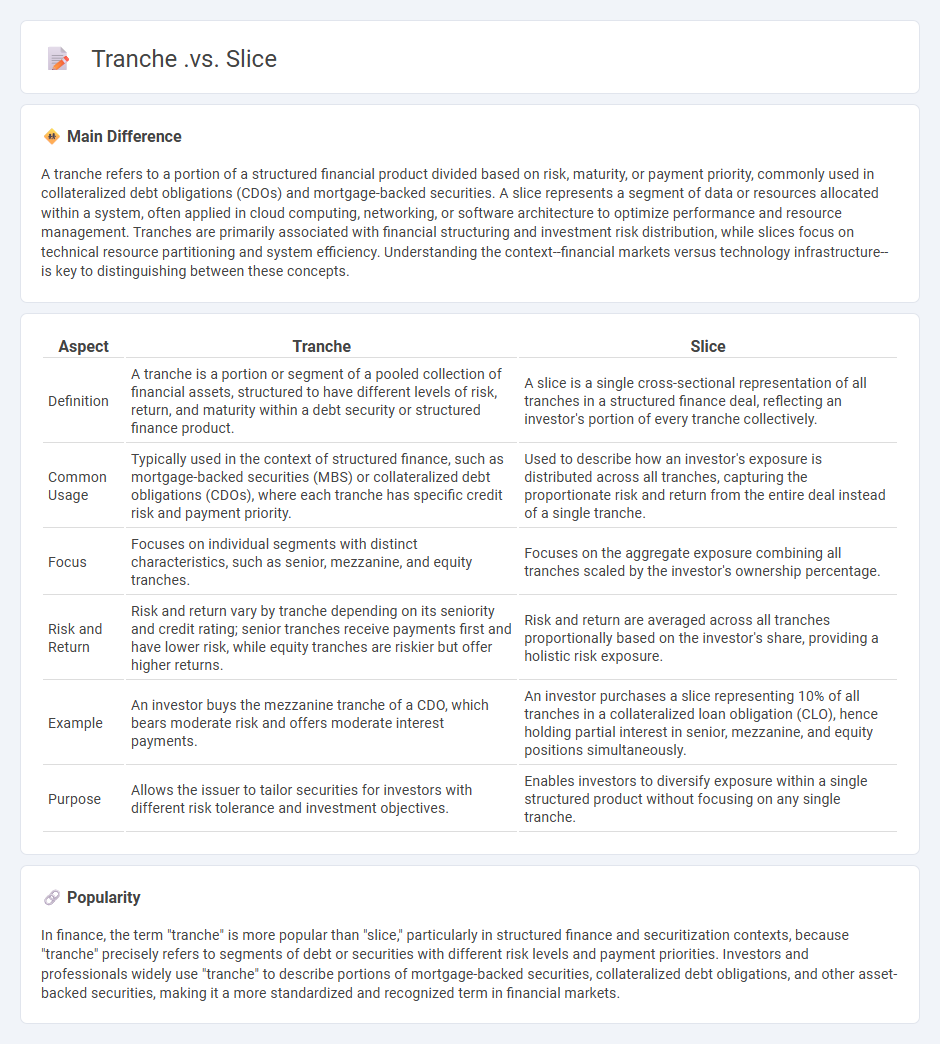

A tranche refers to a portion of a structured financial product divided based on risk, maturity, or payment priority, commonly used in collateralized debt obligations (CDOs) and mortgage-backed securities. A slice represents a segment of data or resources allocated within a system, often applied in cloud computing, networking, or software architecture to optimize performance and resource management. Tranches are primarily associated with financial structuring and investment risk distribution, while slices focus on technical resource partitioning and system efficiency. Understanding the context--financial markets versus technology infrastructure--is key to distinguishing between these concepts.

Connection

A tranche is a portion of a securitized asset, such as a mortgage-backed security, divided based on risk level and maturity. Slices are similar subdivisions within a tranche, representing specific cash flow segments for investors. Both tranches and slices organize structured finance products into risk and return categories to attract varied investor profiles.

Comparison Table

| Aspect | Tranche | Slice |

|---|---|---|

| Definition | A tranche is a portion or segment of a pooled collection of financial assets, structured to have different levels of risk, return, and maturity within a debt security or structured finance product. | A slice is a single cross-sectional representation of all tranches in a structured finance deal, reflecting an investor's portion of every tranche collectively. |

| Common Usage | Typically used in the context of structured finance, such as mortgage-backed securities (MBS) or collateralized debt obligations (CDOs), where each tranche has specific credit risk and payment priority. | Used to describe how an investor's exposure is distributed across all tranches, capturing the proportionate risk and return from the entire deal instead of a single tranche. |

| Focus | Focuses on individual segments with distinct characteristics, such as senior, mezzanine, and equity tranches. | Focuses on the aggregate exposure combining all tranches scaled by the investor's ownership percentage. |

| Risk and Return | Risk and return vary by tranche depending on its seniority and credit rating; senior tranches receive payments first and have lower risk, while equity tranches are riskier but offer higher returns. | Risk and return are averaged across all tranches proportionally based on the investor's share, providing a holistic risk exposure. |

| Example | An investor buys the mezzanine tranche of a CDO, which bears moderate risk and offers moderate interest payments. | An investor purchases a slice representing 10% of all tranches in a collateralized loan obligation (CLO), hence holding partial interest in senior, mezzanine, and equity positions simultaneously. |

| Purpose | Allows the issuer to tailor securities for investors with different risk tolerance and investment objectives. | Enables investors to diversify exposure within a single structured product without focusing on any single tranche. |

Structured Finance

Structured finance involves complex financial instruments designed to redistribute risk and improve capital efficiency for institutions. Common tools include asset-backed securities (ABS), collateralized debt obligations (CDOs), and mortgage-backed securities (MBS), which pool assets like loans or receivables. Key participants include originators, issuers, investors, and rating agencies such as Moody's, S&P, and Fitch, ensuring transparency and credit assessment. The global structured finance market reached approximately $12 trillion in 2023, driven by demand for diversified investment products and risk management solutions.

Risk Segmentation

Risk segmentation in finance involves categorizing borrowers, investments, or portfolios based on varying levels of credit risk, market risk, or operational risk. Financial institutions utilize advanced analytics and machine learning models to segment risk profiles, improving precision in credit scoring and underwriting processes. Effective risk segmentation supports targeted risk management strategies, enhances regulatory compliance, and optimizes capital allocation according to Basel III guidelines. This practice ultimately reduces default rates and maximizes portfolio returns by aligning risk appetite with investment decisions.

Yield Allocation

Yield allocation refers to the strategic distribution of investment income across various assets to maximize returns and manage risk effectively. In finance, this process involves analyzing fixed-income securities, dividends, and interest payments to optimize the portfolio's overall yield performance. Portfolio managers use yield allocation to balance high-yield opportunities with stable income sources, ensuring alignment with investment goals and risk tolerance. Accurate yield allocation enhances cash flow predictability and supports long-term financial planning.

Investment Vehicles

Investment vehicles encompass a broad range of financial instruments designed to grow capital and generate returns, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), and real estate investment trusts (REITs). Stocks offer equity ownership in public or private companies, while bonds represent debt instruments issued by corporations or governments with fixed interest payments. Mutual funds and ETFs provide diversification by pooling investor capital to invest in a portfolio of assets, reducing individual risk exposure. Real estate investment trusts enable investors to access commercial property markets without direct ownership, often yielding regular income through dividends.

Use Case Differentiation

Use case differentiation in finance involves distinguishing applications based on specific financial functions such as risk management, fraud detection, investment analysis, and regulatory compliance. Risk management use cases focus on identifying, assessing, and mitigating financial risks using predictive analytics and machine learning models. Fraud detection employs algorithms to monitor transactions in real-time, flagging anomalies to prevent financial losses. Investment analysis leverages big data and AI for portfolio optimization and market trend prediction, while regulatory compliance ensures adherence to legal standards through automated reporting and audit trails.

Source and External Links

What are Tranches? - Tranches refer to slices or portions of a deal in structured finance, offering different risks and rewards.

Tranche - The term "tranche" is derived from the French word for "slice" and is used in finance to divide investments into parts with varying risk profiles.

Tranche - Practical Law - The term "tranche," meaning "slice," is commonly used in structured note issuances to refer to slices of financial instruments.

FAQs

What is a tranche?

A tranche is a portion or segment of a financial asset or debt that is divided based on risk, maturity, or priority for investment or repayment purposes.

What is a slice in finance?

A slice in finance refers to a specific portion of a pooled asset or portfolio, often representing distinct risk levels or cash flow priorities in structured finance products like mortgage-backed securities or collateralized debt obligations.

How do tranches and slices differ?

Tranches are different risk or maturity classes within a single security, while slices refer to portions of a capital structure that include multiple tranches combined across securities.

What is the purpose of a tranche structure?

A tranche structure divides financial securities into segments with varying risk, return, and maturity profiles to cater to different investor preferences and enhance capital efficiency.

How are slices used in structured finance?

Slices in structured finance represent segmented portions of a security's cash flows or risk profile, allowing investors to target specific levels of risk and return within asset-backed securities or collateralized debt obligations.

Which types of securities use tranches or slices?

Collateralized debt obligations (CDOs), mortgage-backed securities (MBS), and asset-backed securities (ABS) use tranches or slices to differentiate risk and return.

Why are tranches important in risk management?

Tranches are important in risk management because they allow the partitioning of complex financial products into segments with varying risk levels, enabling investors to choose exposure aligned with their risk tolerance and improving overall portfolio diversification.