Greenmail involves purchasing a significant block of company shares to pressure the target firm into buying back those shares at a premium, often as a defense against hostile takeovers. Stock buybacks occur when a company repurchases its own shares from the market to reduce supply, increase share value, or improve financial ratios. Explore the strategic implications and financial effects of greenmail versus stock buybacks to understand their roles in corporate finance.

Main Difference

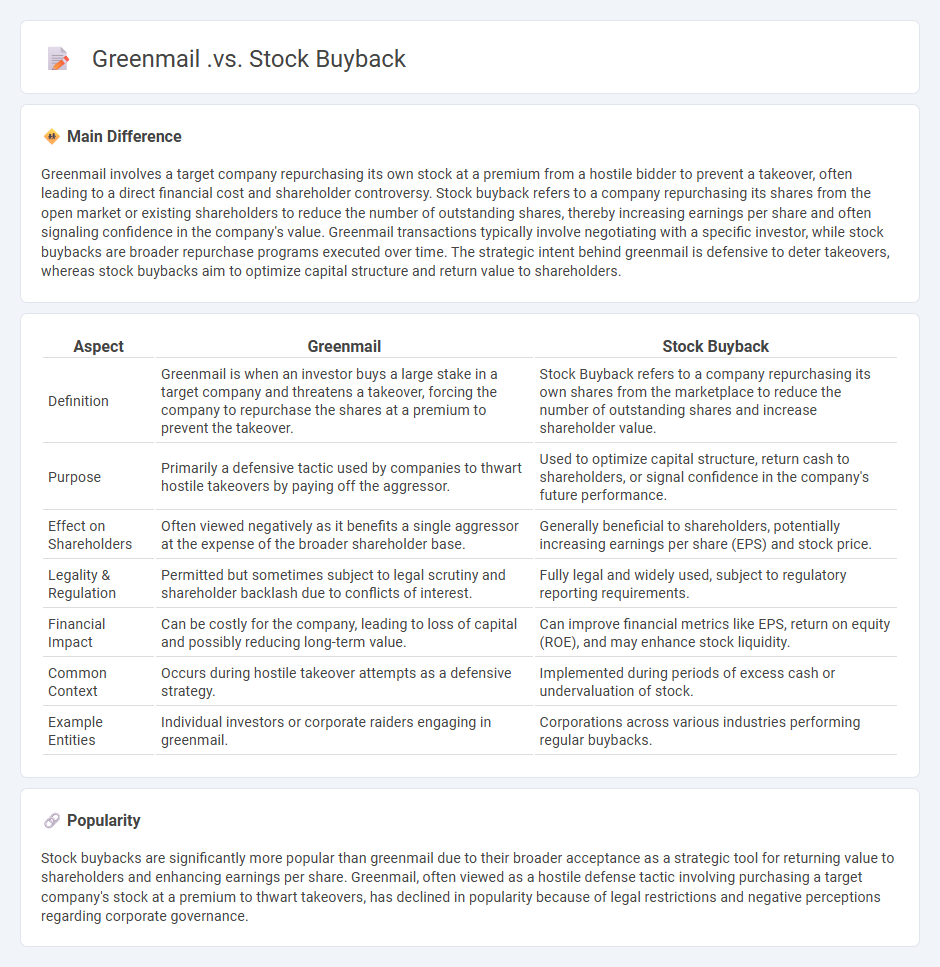

Greenmail involves a target company repurchasing its own stock at a premium from a hostile bidder to prevent a takeover, often leading to a direct financial cost and shareholder controversy. Stock buyback refers to a company repurchasing its shares from the open market or existing shareholders to reduce the number of outstanding shares, thereby increasing earnings per share and often signaling confidence in the company's value. Greenmail transactions typically involve negotiating with a specific investor, while stock buybacks are broader repurchase programs executed over time. The strategic intent behind greenmail is defensive to deter takeovers, whereas stock buybacks aim to optimize capital structure and return value to shareholders.

Connection

Greenmail involves a target company repurchasing its stock at a premium from a hostile bidder to prevent a takeover, effectively a specific form of stock buyback. Stock buyback, in general, is a corporate strategy where a company repurchases its outstanding shares to reduce supply and boost shareholder value. The connection lies in greenmail being a targeted buyback tactic employed defensively in merger and acquisition scenarios.

Comparison Table

| Aspect | Greenmail | Stock Buyback |

|---|---|---|

| Definition | Greenmail is when an investor buys a large stake in a target company and threatens a takeover, forcing the company to repurchase the shares at a premium to prevent the takeover. | Stock Buyback refers to a company repurchasing its own shares from the marketplace to reduce the number of outstanding shares and increase shareholder value. |

| Purpose | Primarily a defensive tactic used by companies to thwart hostile takeovers by paying off the aggressor. | Used to optimize capital structure, return cash to shareholders, or signal confidence in the company's future performance. |

| Effect on Shareholders | Often viewed negatively as it benefits a single aggressor at the expense of the broader shareholder base. | Generally beneficial to shareholders, potentially increasing earnings per share (EPS) and stock price. |

| Legality & Regulation | Permitted but sometimes subject to legal scrutiny and shareholder backlash due to conflicts of interest. | Fully legal and widely used, subject to regulatory reporting requirements. |

| Financial Impact | Can be costly for the company, leading to loss of capital and possibly reducing long-term value. | Can improve financial metrics like EPS, return on equity (ROE), and may enhance stock liquidity. |

| Common Context | Occurs during hostile takeover attempts as a defensive strategy. | Implemented during periods of excess cash or undervaluation of stock. |

| Example Entities | Individual investors or corporate raiders engaging in greenmail. | Corporations across various industries performing regular buybacks. |

Greenmail

Greenmail refers to the practice where a company's stock is bought in large quantities by an investor, often an activist or corporate raider, with the intention of forcing the company to buy back those shares at a premium to prevent a hostile takeover. This strategy capitalizes on the fear of losing control, extracting significant financial gains from the target firm without pursuing a full acquisition. Regulatory frameworks and anti-greenmail provisions have been established to limit this practice, including poison pills and shareholder rights plans. Historical examples include the 1980s corporate battles involving firms like Texaco and Pennzoil.

Stock Buyback

Stock buybacks increase a company's earnings per share by reducing the number of outstanding shares, often signaling confidence in the company's financial health. Firms like Apple and Microsoft have repurchased billions of dollars in shares to optimize capital structure and return value to shareholders. Buybacks can influence stock price positively by creating demand and limiting supply, further benefiting investors. Regulatory guidelines from the SEC ensure transparency and prevent market manipulation during repurchase programs.

Shareholder Value

Shareholder value represents the financial worth delivered to investors through stock price appreciation and dividends, reflecting a company's operational performance and strategic decisions. It is a key metric in business valuation, often influenced by return on equity (ROE), earnings per share (EPS), and cash flow generation. Companies prioritize maximizing shareholder value by increasing profitability, managing risks, and optimizing capital allocation. Financial analysts and corporate managers use tools like discounted cash flow (DCF) models and economic value added (EVA) to assess and enhance this value.

Corporate Control

Corporate control refers to the mechanisms, processes, and structures through which shareholders, boards of directors, and management influence and direct a company's operations and strategic decisions. Concentrated ownership, such as institutional investors or majority shareholders, often plays a significant role in exercising corporate control. Effective corporate control ensures alignment between management's actions and shareholder interests, promoting transparency, accountability, and long-term value creation. Regulatory frameworks like the Sarbanes-Oxley Act in the United States also enhance corporate governance standards to prevent fraud and protect investors.

Anti-Takeover Strategy

An effective anti-takeover strategy protects a company from hostile acquisition attempts by implementing measures such as poison pills, golden parachutes, and staggered board elections. These tactics increase the cost or complexity for potential acquirers, deterring unwanted bids and preserving managerial control. Publicly traded companies often adopt anti-takeover provisions in their corporate charters or bylaws to safeguard shareholder interests and maintain long-term strategic goals. According to a 2023 study by the Harvard Law School Forum on Corporate Governance, nearly 40% of large-cap firms in the S&P 500 have at least one robust anti-takeover mechanism in place.

Source and External Links

Greenmail - Overview, How it Works, Challenges, Example - Greenmail is when investors buy a large share of a company to threaten a hostile takeover, forcing the company to buy back the shares at a premium to prevent that takeover, while a stock buyback is the company repurchasing its own shares, often to counter such threats or improve share value.

Greenmail - Wikipedia - Greenmail involves investors threatening a takeover with a significant share purchase, leading the target firm to repurchase those shares at a premium, whereas a stock buyback more generally refers to a company's repurchase of its own shares for varied strategic reasons.

Greenmail Playbook: Strategic Buybacks to Ward Off Hostile ... - Greenmail specifically describes a company paying a premium to buy back shares from a hostile bidder to avoid a takeover, contrasting with stock buybacks which may be broader corporate strategies not necessarily linked to deterrence of hostile bids.

FAQs

What is greenmail in corporate finance?

Greenmail in corporate finance is the practice where a company repurchases its own shares at a premium from a hostile bidder to prevent a takeover.

What is a stock buyback?

A stock buyback is a corporate action where a company repurchases its own shares from the open market to reduce the number of outstanding shares and increase shareholder value.

How does greenmail differ from stock buyback?

Greenmail involves a company repurchasing its own shares at a premium to prevent a hostile takeover, whereas stock buyback is a regular repurchase of shares to reduce supply and increase shareholder value.

Why do companies use greenmail strategies?

Companies use greenmail strategies to prevent hostile takeovers by repurchasing shares from potential acquirers at a premium, thereby deterring unwanted acquisition attempts.

What are the advantages of stock buybacks for shareholders?

Stock buybacks increase earnings per share (EPS), boost stock price, provide tax-efficient returns, and signal company confidence to investors.

What are the drawbacks of greenmail for a company?

Greenmail forces a company to repurchase its shares at a premium, resulting in significant financial loss, damages shareholder value, invites management distraction, and encourages hostile takeover attempts.

How do regulatory bodies view greenmail and stock buybacks?

Regulatory bodies generally view greenmail as an aggressive and potentially manipulative practice subject to restrictions or penalties, while stock buybacks are regulated to prevent market manipulation but are broadly accepted as a tool for returning capital to shareholders.