Greenmail involves a hostile investor purchasing a substantial stake in a company to threaten a takeover, then demanding a premium buyback to relinquish control. White Knight refers to a friendly investor or company that acquires a target firm to counteract a hostile takeover attempt and protect the target's interests. Explore the strategic roles of Greenmail and White Knights in corporate takeover defense.

Main Difference

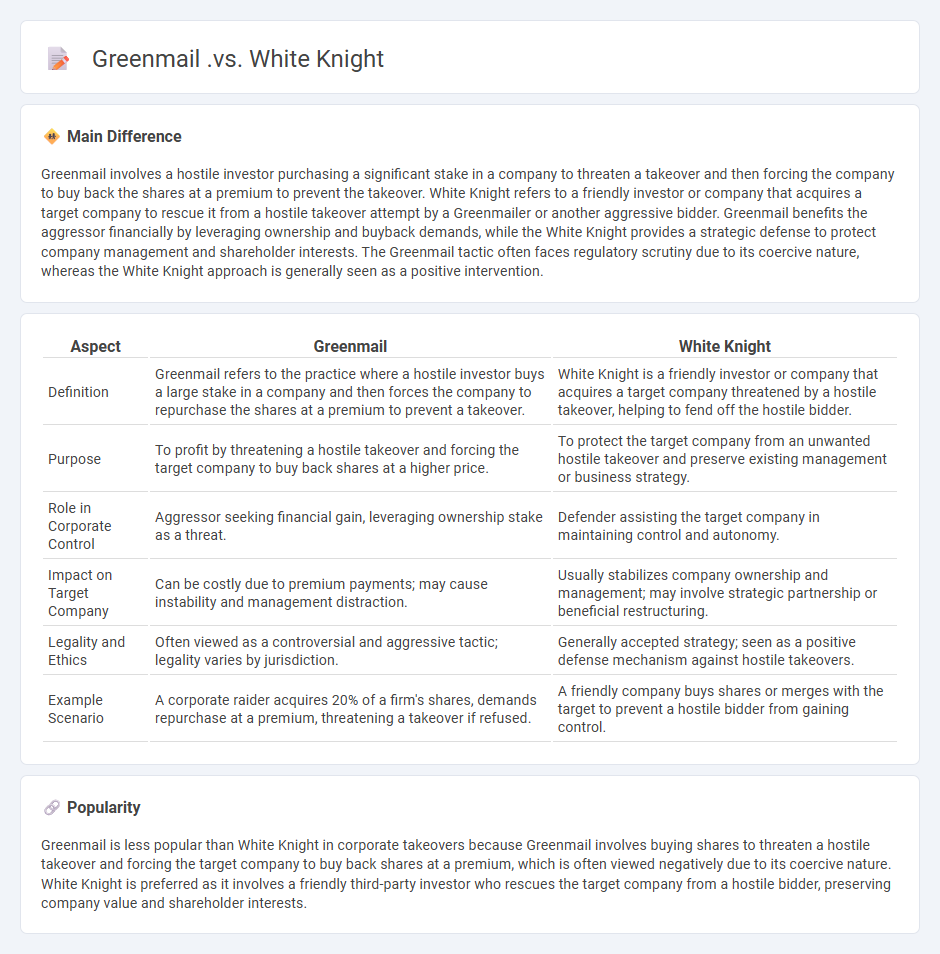

Greenmail involves a hostile investor purchasing a significant stake in a company to threaten a takeover and then forcing the company to buy back the shares at a premium to prevent the takeover. White Knight refers to a friendly investor or company that acquires a target company to rescue it from a hostile takeover attempt by a Greenmailer or another aggressive bidder. Greenmail benefits the aggressor financially by leveraging ownership and buyback demands, while the White Knight provides a strategic defense to protect company management and shareholder interests. The Greenmail tactic often faces regulatory scrutiny due to its coercive nature, whereas the White Knight approach is generally seen as a positive intervention.

Connection

Greenmail involves a hostile entity acquiring a significant stake in a company to force a buyback at a premium, benefiting the attacker financially. White Knight acts as a friendly investor who intervenes by purchasing shares to thwart the Greenmailer's hostile takeover attempt. This defensive strategy preserves company control and deters Greenmail tactics by providing a preferable acquisition alternative.

Comparison Table

| Aspect | Greenmail | White Knight |

|---|---|---|

| Definition | Greenmail refers to the practice where a hostile investor buys a large stake in a company and then forces the company to repurchase the shares at a premium to prevent a takeover. | White Knight is a friendly investor or company that acquires a target company threatened by a hostile takeover, helping to fend off the hostile bidder. |

| Purpose | To profit by threatening a hostile takeover and forcing the target company to buy back shares at a higher price. | To protect the target company from an unwanted hostile takeover and preserve existing management or business strategy. |

| Role in Corporate Control | Aggressor seeking financial gain, leveraging ownership stake as a threat. | Defender assisting the target company in maintaining control and autonomy. |

| Impact on Target Company | Can be costly due to premium payments; may cause instability and management distraction. | Usually stabilizes company ownership and management; may involve strategic partnership or beneficial restructuring. |

| Legality and Ethics | Often viewed as a controversial and aggressive tactic; legality varies by jurisdiction. | Generally accepted strategy; seen as a positive defense mechanism against hostile takeovers. |

| Example Scenario | A corporate raider acquires 20% of a firm's shares, demands repurchase at a premium, threatening a takeover if refused. | A friendly company buys shares or merges with the target to prevent a hostile bidder from gaining control. |

Corporate Takeover

Corporate takeover refers to the acquisition of one company by another, often through purchasing a controlling share of stock. Hostile takeovers occur when the target company's management opposes the acquisition, leading the bidder to bypass executives and appeal directly to shareholders. Leveraged buyouts (LBOs) use significant amounts of borrowed money to finance the acquisition, frequently restructuring the target company's assets post-takeover. This process impacts market competition, corporate governance, and shareholder value in the broader business landscape.

Greenmail

Greenmail is a corporate finance tactic where a company repurchases its own shares at a premium from a hostile bidder to prevent a takeover. This strategy became prominent in the 1980s, often involving leveraged buyouts and activist investors seeking control. Companies involved in greenmail transactions typically pay above-market prices to shareholders, leading to short-term gains for the greenmailer but potential long-term value erosion. Regulatory changes and shareholder activism have reduced the prevalence of greenmail in modern business practices.

White Knight

A White Knight in business refers to a friendly investor or company that acquires a target firm facing a hostile takeover, preserving its existing management and operations. These investors often offer better terms than hostile bidders, maintaining the company's strategic vision and employee welfare. White Knights play a crucial role in mergers and acquisitions by providing a more acceptable alternative to hostile takeovers. Prominent examples include Warren Buffett's Berkshire Hathaway acting as a White Knight in various acquisition scenarios.

Hostile Bid

A hostile bid in business refers to an acquisition attempt where the acquiring company directly offers to buy shares from the target company's shareholders, bypassing the target's management. This strategy often involves a tender offer at a premium price to incentivize shareholders to sell against the wishes of the company's board. Hostile bids are common in merger and acquisition activities, particularly in competitive industries such as technology and pharmaceuticals. The process can trigger defensive tactics like poison pills or shareholder rights plans to prevent unwanted takeovers.

Shareholder Value

Shareholder value represents the financial worth delivered to investors through dividends and stock price appreciation, reflecting a company's profitability and growth potential. Strategies to enhance shareholder value often focus on efficient capital allocation, cost management, and revenue growth to maximize return on equity (ROE) and earnings per share (EPS). Companies like Apple and Microsoft have consistently increased shareholder value by innovating products and maintaining strong balance sheets. Market metrics such as total shareholder return (TSR) quantify performance by combining capital gains and dividends over a specific period.

Source and External Links

White knight: White Knights vs: Greenmail: Rescuing Companies or ... - White knights are friendly buyers who acquire a target company to preserve its operations, while greenmail involves hostile bidders buying shares to force the company to repurchase them at a premium to prevent takeover, benefiting the bidder financially.

White Knight: Riding in to Rescue Companies from Greenmail ... - White knights prevent greenmail by providing a favorable acquisition alternative to hostile bidders, protecting the company from paying premiums to aggressive investors and preserving long-term shareholder value.

The 5 Defenses Against a Hostile Takeover - Fmi.online - Greenmail is a defense where a company pays a hostile bidder a premium to stop a takeover attempt, whereas a white knight is a friendly third party that acquires the company to fend off hostile bidders and preserve company control.

FAQs

What is greenmail in corporate takeovers?

Greenmail in corporate takeovers is the practice where an investor buys a significant block of a company's shares and threatens a hostile takeover, prompting the company to repurchase the shares at a premium to prevent the takeover.

How does a white knight strategy work in mergers and acquisitions?

A white knight strategy in mergers and acquisitions involves a friendly third-party company acquiring a target firm to prevent a hostile takeover by an undesirable bidder.

What are the key differences between greenmail and a white knight?

Greenmail involves acquiring a large stake in a company to threaten a hostile takeover and force the company to buy back shares at a premium, while a white knight is a friendly third party that acquires a company to prevent a hostile takeover, preserving management and shareholder value.

Why do companies use greenmail as a defense tactic?

Companies use greenmail as a defense tactic to prevent hostile takeovers by buying back shares from a potential acquirer at a premium price, deterring the acquisition attempt.

How does the presence of a white knight affect a hostile takeover attempt?

The presence of a white knight deters a hostile takeover by offering a friendly acquisition alternative, preserving the target company's management and enhancing shareholder value.

What are the legal and ethical concerns of greenmail and white knight strategies?

Greenmail raises legal concerns due to potential violations of securities laws and ethical issues involving coercive tactics exploiting company vulnerabilities; white knight strategies face ethical concerns related to conflicts of interest and possible manipulation of shareholder interests, while legally they must comply with fiduciary duties and antitrust regulations.

Are there real-world examples of companies using greenmail or a white knight?

Yes, in 1980, Procter & Gamble used a white knight defense by inviting White Knight investor, Warren Buffett's Berkshire Hathaway, to counter T. Boone Pickens' greenmail hostile takeover attempt.