The Bertrand paradox challenges classical economic theory by demonstrating how firms can sustain prices above marginal cost despite competing in price. In contrast, the Chamberlin model introduces product differentiation as a key factor, allowing firms to maintain market power and positive markups. Explore the nuances of these models to understand their implications on market competition and pricing strategies.

Main Difference

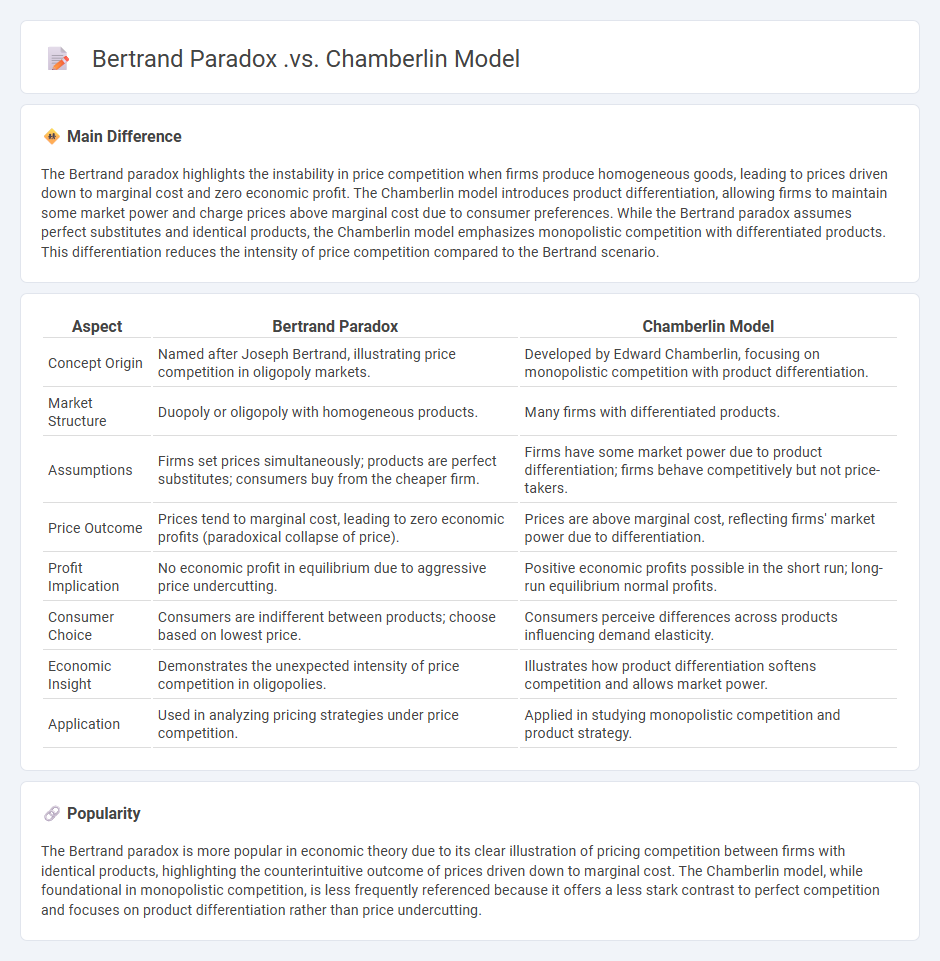

The Bertrand paradox highlights the instability in price competition when firms produce homogeneous goods, leading to prices driven down to marginal cost and zero economic profit. The Chamberlin model introduces product differentiation, allowing firms to maintain some market power and charge prices above marginal cost due to consumer preferences. While the Bertrand paradox assumes perfect substitutes and identical products, the Chamberlin model emphasizes monopolistic competition with differentiated products. This differentiation reduces the intensity of price competition compared to the Bertrand scenario.

Connection

The Bertrand paradox illustrates inconsistencies in probability outcomes when different methods define randomness on geometric objects, revealing the ambiguity in selecting uniform distributions. Chamberlin's model, focusing on consumer choice within differentiated product markets, implicitly relies on probabilistic assumptions to predict preferences and market equilibrium. Their connection lies in the interpretation of randomness and probability distributions, highlighting the impact of modeling choices on theoretical predictions in economics and decision theory.

Comparison Table

| Aspect | Bertrand Paradox | Chamberlin Model |

|---|---|---|

| Concept Origin | Named after Joseph Bertrand, illustrating price competition in oligopoly markets. | Developed by Edward Chamberlin, focusing on monopolistic competition with product differentiation. |

| Market Structure | Duopoly or oligopoly with homogeneous products. | Many firms with differentiated products. |

| Assumptions | Firms set prices simultaneously; products are perfect substitutes; consumers buy from the cheaper firm. | Firms have some market power due to product differentiation; firms behave competitively but not price-takers. |

| Price Outcome | Prices tend to marginal cost, leading to zero economic profits (paradoxical collapse of price). | Prices are above marginal cost, reflecting firms' market power due to differentiation. |

| Profit Implication | No economic profit in equilibrium due to aggressive price undercutting. | Positive economic profits possible in the short run; long-run equilibrium normal profits. |

| Consumer Choice | Consumers are indifferent between products; choose based on lowest price. | Consumers perceive differences across products influencing demand elasticity. |

| Economic Insight | Demonstrates the unexpected intensity of price competition in oligopolies. | Illustrates how product differentiation softens competition and allows market power. |

| Application | Used in analyzing pricing strategies under price competition. | Applied in studying monopolistic competition and product strategy. |

Price Competition

Price competition occurs when businesses strive to attract customers by lowering prices for similar goods or services within a market. It plays a crucial role in markets characterized by perfect competition and monopolistic competition, driving prices toward equilibrium levels. The intensity of price competition can lead to reduced profit margins, influencing firms' strategies on cost management and product differentiation. Empirical studies in economics highlight its effect on consumer welfare through increased accessibility and market efficiency.

Product Differentiation

Product differentiation in economics refers to the strategy firms use to distinguish their products from those of competitors through unique attributes such as design, quality, features, or branding. It plays a crucial role in monopolistic competition, where many sellers offer similar but not identical products, enabling businesses to create niche markets and reduce price competition. Effective product differentiation can increase consumer loyalty, justify premium pricing, and enhance market share. Empirical studies show differentiated products often lead to higher profit margins and stronger competitive advantage.

Nash Equilibrium

Nash equilibrium represents a fundamental concept in game theory where no player can benefit by unilaterally changing their strategy, assuming the strategies of others remain fixed. This equilibrium applies to various economic models, including oligopoly markets and auction designs, facilitating predictions of strategic interactions and outcomes. Developed by John Nash in 1950, it provides a method to analyze competitive behavior and decision-making under conditions of mutual dependence. Economists utilize Nash equilibrium to study market dynamics, bargaining scenarios, and the strategic foundations of economic policy.

Homogeneous Goods vs Differentiated Products

Homogeneous goods are products that are identical in quality and features, such as crude oil or wheat, making them perfectly substitutable in the market. Differentiated products, like smartphones or automobiles, possess unique attributes or branding that distinguish them from competitors, leading to varying consumer preferences. In economics, the presence of homogeneous goods typically leads to perfect competition, while differentiated products result in monopolistic competition or oligopoly. Market strategies and pricing power vary significantly between these two types of goods based on product uniformity and consumer perception.

Market Outcomes

Market outcomes refer to the results produced by the interaction of supply and demand within a market, determining prices, quantities, and the allocation of resources. Efficient market outcomes occur when resources are allocated to maximize total surplus, reflecting optimal production and consumption. Market failures arise from externalities, public goods, information asymmetries, or monopolies, leading to suboptimal outcomes requiring government intervention. Economic models such as competitive equilibrium and welfare economics analyze these outcomes to guide policy decisions and improve market efficiency.

Source and External Links

A Psychological Reexamination of the Bertrand Paradox - The Bertrand paradox describes how two competing firms, when pricing identically, end up charging marginal cost due to incentives to undercut each other, a paradox since charging higher prices would yield profits but is unstable under rationality assumptions.

Pricing, Product Diversity, and Search Costs - This model integrates the Bertrand Paradox with Chamberlinian monopolistic competition and the Diamond Paradox, showing how market prices and product diversity depend on search costs and firm numbers, bridging perfect competition and monopolistic competition frameworks.

Pricing, Product Diversity, and Search Costs: A Bertrand-Chamberlin-Diamond Model - The study explores price competition when search costs and product differentiation exist, with the Bertrand paradox representing one limit case and Chamberlinian monopolistic competition another, highlighting how search costs affect equilibrium prices, diversity, and market failure.

FAQs

What is the Bertrand paradox?

The Bertrand paradox illustrates that the probability of a random chord in a circle being longer than the side of an inscribed equilateral triangle varies depending on the method used to define "random," highlighting ambiguity in probability definition.

What are the key assumptions of the Bertrand model?

The key assumptions of the Bertrand model are: firms produce homogeneous products, compete by setting prices simultaneously, have identical and constant marginal costs, consumers buy from the firm offering the lowest price, and there are no capacity constraints or product differentiation.

How does the Chamberlin model differ from the Bertrand model?

The Chamberlin model assumes product differentiation and focuses on monopolistic competition with many firms setting prices above marginal cost, while the Bertrand model assumes homogeneous products and predicts price competition driving prices down to marginal cost.

What is product differentiation in the Chamberlin model?

Product differentiation in the Chamberlin model refers to the process by which firms produce products that are similar but not identical, allowing them to have some degree of market power by appealing to specific consumer preferences.

How do prices compare in Bertrand vs. Chamberlin models?

Prices in the Bertrand model typically equal marginal cost due to price undercutting, while prices in the Chamberlin model are above marginal cost because firms have some market power and product differentiation.

What are the main criticisms of the Bertrand paradox?

The main criticisms of the Bertrand paradox highlight its reliance on ambiguous problem definitions, inconsistent assumptions about randomness, and the resulting contradictory probability outcomes challenging classical interpretations of geometric probability.

Why is the Chamberlin model important for understanding real market behavior?

The Chamberlin model is important because it incorporates product differentiation and imperfect competition, offering a realistic framework that explains how firms have market power and set prices above marginal cost in monopolistic competition.