The Lucas Critique challenges traditional econometric models by emphasizing that policy evaluations must account for changes in agents' expectations, which affect economic behavior. The Rational Expectations Hypothesis posits that individuals use all available information to forecast future economic variables accurately, influencing policy outcomes. Explore the key differences and implications of these foundational economic theories to better understand macroeconomic policy analysis.

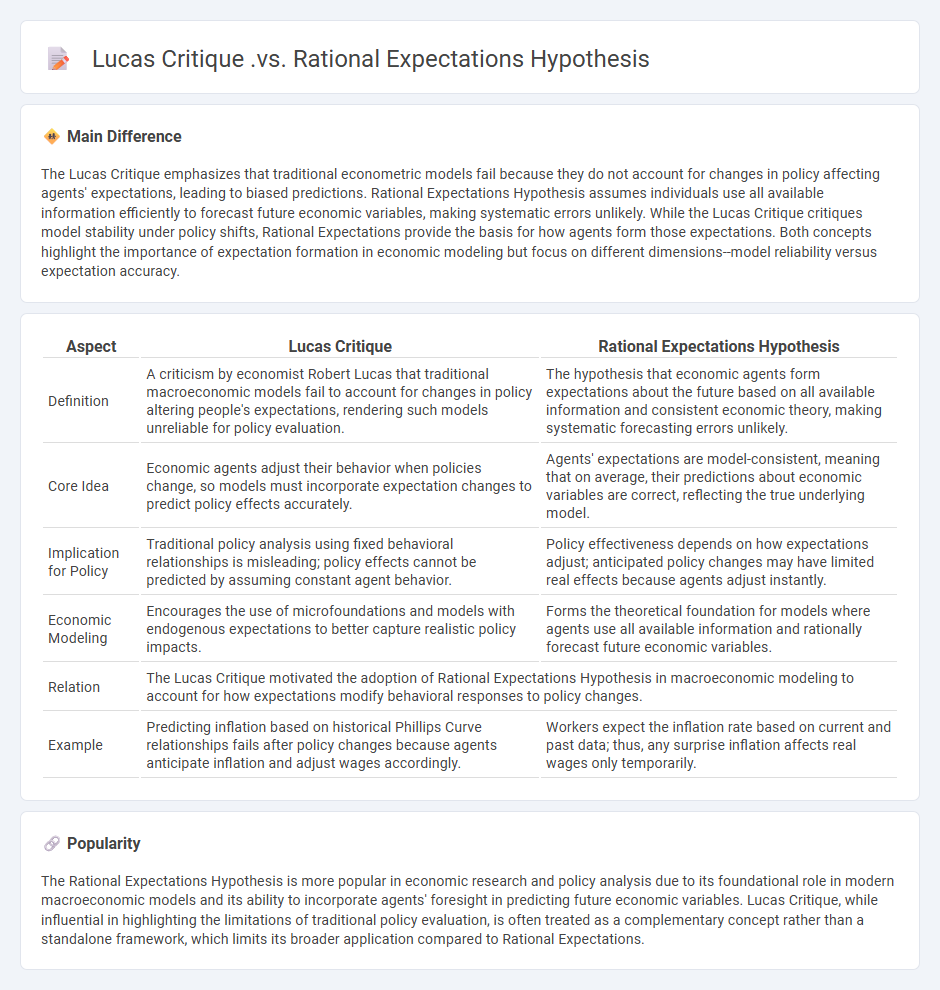

Main Difference

The Lucas Critique emphasizes that traditional econometric models fail because they do not account for changes in policy affecting agents' expectations, leading to biased predictions. Rational Expectations Hypothesis assumes individuals use all available information efficiently to forecast future economic variables, making systematic errors unlikely. While the Lucas Critique critiques model stability under policy shifts, Rational Expectations provide the basis for how agents form those expectations. Both concepts highlight the importance of expectation formation in economic modeling but focus on different dimensions--model reliability versus expectation accuracy.

Connection

The Lucas Critique challenges traditional econometric policy evaluation by emphasizing that economic agents adjust their expectations based on changes in policy, which undermines the stability of estimated relationships. The Rational Expectations Hypothesis complements this by asserting that individuals use all available information efficiently to forecast future economic variables, aligning their behavior with anticipated policy shifts. Together, these theories highlight the necessity for models to incorporate forward-looking expectations to accurately predict policy impacts.

Comparison Table

| Aspect | Lucas Critique | Rational Expectations Hypothesis |

|---|---|---|

| Definition | A criticism by economist Robert Lucas that traditional macroeconomic models fail to account for changes in policy altering people's expectations, rendering such models unreliable for policy evaluation. | The hypothesis that economic agents form expectations about the future based on all available information and consistent economic theory, making systematic forecasting errors unlikely. |

| Core Idea | Economic agents adjust their behavior when policies change, so models must incorporate expectation changes to predict policy effects accurately. | Agents' expectations are model-consistent, meaning that on average, their predictions about economic variables are correct, reflecting the true underlying model. |

| Implication for Policy | Traditional policy analysis using fixed behavioral relationships is misleading; policy effects cannot be predicted by assuming constant agent behavior. | Policy effectiveness depends on how expectations adjust; anticipated policy changes may have limited real effects because agents adjust instantly. |

| Economic Modeling | Encourages the use of microfoundations and models with endogenous expectations to better capture realistic policy impacts. | Forms the theoretical foundation for models where agents use all available information and rationally forecast future economic variables. |

| Relation | The Lucas Critique motivated the adoption of Rational Expectations Hypothesis in macroeconomic modeling to account for how expectations modify behavioral responses to policy changes. | |

| Example | Predicting inflation based on historical Phillips Curve relationships fails after policy changes because agents anticipate inflation and adjust wages accordingly. | Workers expect the inflation rate based on current and past data; thus, any surprise inflation affects real wages only temporarily. |

Policy Ineffectiveness

Policy ineffectiveness arises when government interventions fail to influence economic outcomes as intended, often due to rational expectations by agents anticipating policy moves. The concept is central to the New Classical Macroeconomics, emphasizing that systematic monetary policy has no real effects on output or employment in the long run. Models such as the Lucas critique highlight how changes in policy alter private sector behavior, rendering traditional econometric relationships invalid. Empirical studies show that anticipated policy adjustments tend to be neutralized by market responses, limiting the efficacy of fiscal and monetary measures.

Microfoundations

Microfoundations analyze individual agents' behaviors and interactions to explain macroeconomic phenomena, emphasizing decision-making processes in households and firms. This approach grounds aggregate economic models in microeconomic principles, enhancing accuracy in predicting market dynamics and policy impacts. Key contributions arise from game theory, behavioral economics, and information asymmetry, providing insights into consumption, labor supply, and investment patterns. Empirical studies use micro-level data to calibrate and validate models, improving economic forecasting and policy design.

Structural Change

Structural change in economics refers to the dynamic reallocation of resources, labor, and capital across different sectors of an economy, typically from agriculture to industry and services, reflecting development and technological progress. This transformation influences productivity, employment patterns, and income distribution, driving economic growth and higher living standards. Key indicators of structural change include shifts in sectoral GDP shares, labor market transitions, and changes in production techniques. Policymakers monitor structural change to design strategies that promote innovation, competitiveness, and sustainable development.

Model Consistency

Model consistency in economics ensures that theoretical frameworks reliably represent economic behavior across various conditions and datasets. It involves aligning model assumptions with empirical observations, maintaining internal logical coherence, and producing stable predictions. Consistent models are crucial for policy analysis, allowing economists to forecast market outcomes and evaluate intervention effects accurately. This concept underpins econometric practices, where ensuring parameter stability and minimizing specification errors enhance predictive validity.

Predictive Accuracy

Predictive accuracy in economics measures how well economic models forecast future variables such as GDP growth, inflation rates, or unemployment levels. High predictive accuracy enables policymakers and investors to make informed decisions based on reliable economic projections. Techniques like time series analysis, machine learning algorithms, and econometric modeling contribute significantly to improving prediction precision. Empirical studies show that combining structural models with real-time data enhances the robustness of economic forecasts.

Source and External Links

Robert E. Lucas - Econlib - The Lucas Critique argues that traditional macroeconomic models fail when policy changes, because people's expectations--modeled by the Rational Expectations Hypothesis--adjust, rendering past empirical relationships unreliable for predicting future policy effects.

Rational Expectation Hypothesis - Ecoholics - The Rational Expectations Hypothesis states that people use all available information to form expectations about the future, leading to the Policy Ineffectiveness Proposition, while the Lucas Critique specifically warns that models ignoring these expectation shifts give faulty policy advice.

Rational expectation and the Lucas critique [PDF] - Lucas developed the critique by showing that under rational expectations, parameters in econometric models (like the Phillips curve) are not stable across policy regimes, because agents' expectations and behavior change with policy.

FAQs

What is the Lucas Critique?

The Lucas Critique asserts that traditional economic models fail to predict policy effects accurately because they ignore changes in individuals' behavior in response to policy shifts, emphasizing the need for models with micro-founded expectations.

What is the Rational Expectations Hypothesis?

The Rational Expectations Hypothesis states that individuals and firms form forecasts about future economic variables by optimally using all available information, making their predictions unbiased and consistent with the actual economic model.

How does the Lucas Critique challenge traditional policy evaluation?

The Lucas Critique challenges traditional policy evaluation by arguing that policy impact assessments based on historical data fail to account for changes in people's expectations and behavior, leading to unreliable predictions.

What are the assumptions behind the Rational Expectations Hypothesis?

The Rational Expectations Hypothesis assumes that agents have full access to all available information, use all relevant data efficiently, model the economy correctly, and on average predict future variables without systematic errors.

How do the Lucas Critique and Rational Expectations relate to macroeconomic modeling?

The Lucas Critique highlights that traditional macroeconomic models fail when policy changes alter agents' behavior, prompting models to incorporate Rational Expectations, where agents form forecasts based on model-consistent expectations, ensuring policy analysis accounts for behavior shifts.

Why is the Lucas Critique important in economic forecasting?

The Lucas Critique is important in economic forecasting because it highlights that traditional models fail to account for changes in policy altering agents' behavior, making forecasts unreliable if they do not incorporate micro-founded expectations and structural parameters.

How do policymakers adjust their strategies due to the Lucas Critique and Rational Expectations?

Policymakers adjust strategies by designing rules-based policies that anticipate agents' adaptive expectations, avoiding naive policy interventions that fail when agents optimize based on model-consistent forecasts, thus ensuring policy effectiveness under the Lucas Critique and Rational Expectations framework.