Marshallian demand functions represent consumer choices based on income and prices, maximizing utility subject to a budget constraint. Hicksian demand functions capture compensated demand, holding utility constant and showing how consumption adjusts to price changes without income effects. Explore the distinctions and applications of these demand concepts for deeper economic insights.

Main Difference

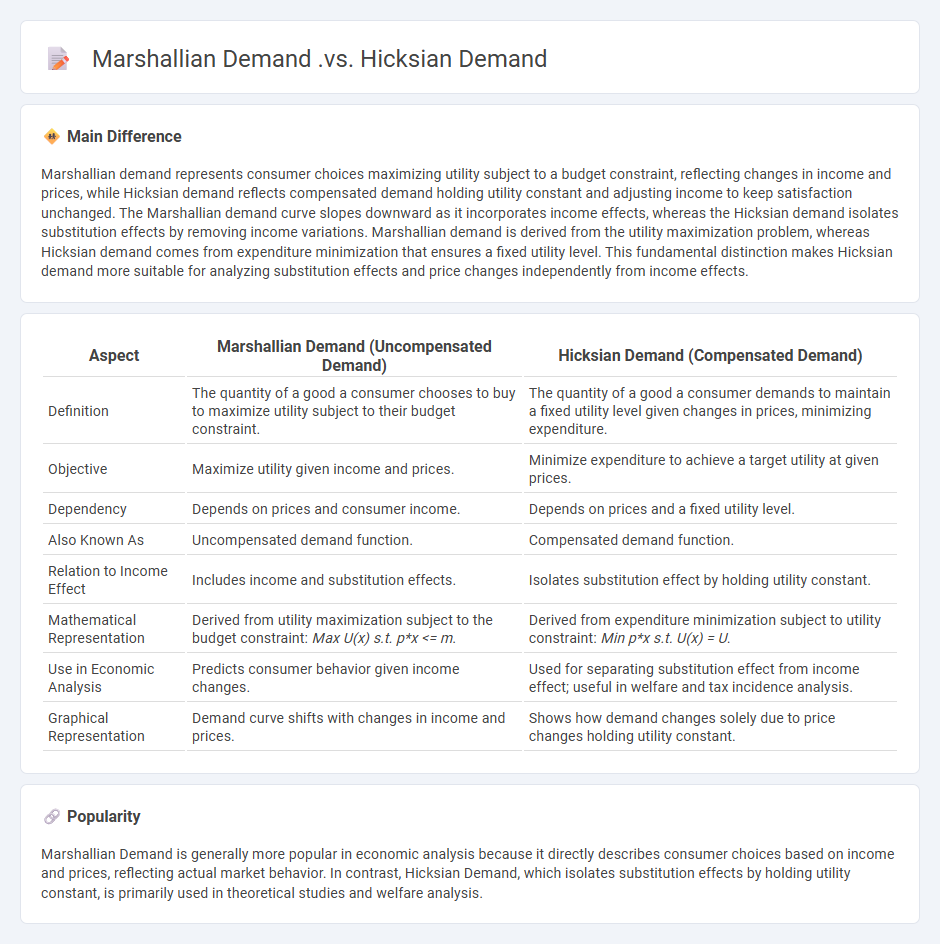

Marshallian demand represents consumer choices maximizing utility subject to a budget constraint, reflecting changes in income and prices, while Hicksian demand reflects compensated demand holding utility constant and adjusting income to keep satisfaction unchanged. The Marshallian demand curve slopes downward as it incorporates income effects, whereas the Hicksian demand isolates substitution effects by removing income variations. Marshallian demand is derived from the utility maximization problem, whereas Hicksian demand comes from expenditure minimization that ensures a fixed utility level. This fundamental distinction makes Hicksian demand more suitable for analyzing substitution effects and price changes independently from income effects.

Connection

Marshallian demand, derived from utility maximization given income and prices, reflects consumer choices under budget constraints and varying income levels. Hicksian demand, focused on expenditure minimization for a fixed utility level, isolates substitution effects by holding real utility constant. The Slutsky equation mathematically links these demands by decomposing the total effect of a price change into substitution and income effects, illustrating how Hicksian demands transform into Marshallian demands when income effects are considered.

Comparison Table

| Aspect | Marshallian Demand (Uncompensated Demand) | Hicksian Demand (Compensated Demand) |

|---|---|---|

| Definition | The quantity of a good a consumer chooses to buy to maximize utility subject to their budget constraint. | The quantity of a good a consumer demands to maintain a fixed utility level given changes in prices, minimizing expenditure. |

| Objective | Maximize utility given income and prices. | Minimize expenditure to achieve a target utility at given prices. |

| Dependency | Depends on prices and consumer income. | Depends on prices and a fixed utility level. |

| Also Known As | Uncompensated demand function. | Compensated demand function. |

| Relation to Income Effect | Includes income and substitution effects. | Isolates substitution effect by holding utility constant. |

| Mathematical Representation | Derived from utility maximization subject to the budget constraint: Max U(x) s.t. p*x <= m. | Derived from expenditure minimization subject to utility constraint: Min p*x s.t. U(x) = U. |

| Use in Economic Analysis | Predicts consumer behavior given income changes. | Used for separating substitution effect from income effect; useful in welfare and tax incidence analysis. |

| Graphical Representation | Demand curve shifts with changes in income and prices. | Shows how demand changes solely due to price changes holding utility constant. |

Utility Maximization

Utility maximization in economics refers to the process by which consumers allocate their income to purchase goods and services that maximize their overall satisfaction or utility. This concept relies on the assumption of rational behavior, where individuals aim to achieve the highest utility given their budget constraints. The utility function measures preferences, often modeled using ordinal or cardinal utility to represent varying levels of satisfaction. Key models include the consumer choice theory and the law of diminishing marginal utility, which explains how the utility gained from each additional unit of a good decreases.

Income Effect

Income effect in economics refers to the change in consumer purchasing power resulting from a change in real income, affecting demand for goods and services. When prices fall, the effective income of consumers increases, allowing them to buy more, whereas rising prices reduce real income and curb consumption. The income effect is a key factor in consumer behavior analysis and helps explain shifts in demand curves beyond substitution effects. It plays a crucial role in labor supply decisions and consumer choice theory, influencing market equilibrium outcomes.

Substitution Effect

The substitution effect in economics describes how consumers adjust their purchasing decisions when the price of a good changes, choosing relatively cheaper alternatives to maximize utility. This effect is a key component in understanding the downward-sloping demand curve, as a price increase typically leads consumers to substitute toward less expensive substitutes. It operates alongside the income effect, which accounts for changes in purchasing power due to price fluctuations. Accurate modeling of the substitution effect is essential for predicting consumer behavior and market responses.

Expenditure Minimization

Expenditure minimization is a fundamental concept in microeconomics focusing on finding the lowest cost combination of goods that achieves a specific utility level. This approach is formalized through the expenditure function, which quantifies the minimal expenditure required to reach a predetermined utility given prevailing prices. The theory relies heavily on duality between utility maximization and expenditure minimization, offering valuable insights into consumer behavior and demand functions. Empirical applications often involve estimating cost functions and analyzing consumer responses to price changes in various markets.

Compensated vs Uncompensated Demand

Compensated demand reflects consumer behavior when prices change, holding the consumer's utility constant by adjusting income, isolating the substitution effect from the income effect. Uncompensated demand, or Marshallian demand, shows the actual quantity consumers purchase given their income and prices, capturing both substitution and income effects. The Slutsky equation mathematically decomposes the total effect of a price change into compensated (substitution) and uncompensated (income) effects. Understanding these Demand concepts is crucial in microeconomics for accurate welfare analysis and policy evaluation.

Source and External Links

Duality of Marshallian and Hicksian Demand Function - Marshallian demand depends on prices and income (budget), reflecting utility changes as income varies, while Hicksian demand depends on prices and a fixed utility level, representing compensated demand that isolates substitution effects; both demand functions intersect consistently at given prices when income compensates for utility changes.

Marshall and Hicks Understanding the Ordinary and Compensated Demand - The key difference is that Marshallian demand is a function of prices and budget (income), showing total demand effect, whereas Hicksian demand is a function of prices and utility level, showing demand when utility is held constant and income is adjusted accordingly.

Lecture Note 6 - Demand Functions: Income Effects, Substitution Effects - Marshallian (uncompensated) demand combines income and substitution effects responding to changes in prices and income, while Hicksian (compensated) demand isolates substitution effects by holding utility constant and adjusting expenditures, mathematically derived from expenditure minimization.

FAQs

What is Marshallian demand?

Marshallian demand is the consumer's optimal quantity of goods chosen to maximize utility subject to a budget constraint at given prices and income.

What is Hicksian demand?

Hicksian demand represents a consumer's optimal quantity of goods purchased to achieve a fixed utility level at the lowest possible cost, derived from expenditure minimization under a given utility constraint.

How do Marshallian and Hicksian demand differ?

Marshallian demand reflects consumer choices maximizing utility subject to a budget constraint with given prices and income, showing actual quantity demanded. Hicksian demand represents compensated demand minimizing expenditure to achieve a fixed utility level at given prices, isolating substitution effects by holding utility constant.

What are the assumptions behind Marshallian demand?

Marshallian demand assumes consumers maximize utility subject to a budget constraint, have well-defined preferences that are complete, transitive, and continuous, face given prices and income, and exhibit non-satiation or monotonicity in their preferences.

What are the assumptions behind Hicksian demand?

Hicksian demand assumes consumer preferences are stable and complete, utility maximization subject to a fixed level of utility, nonsatiation, convex and continuous preferences, and well-defined budget constraints with given prices.

How is expenditure minimized in Hicksian demand?

Expenditure is minimized in Hicksian demand by selecting a consumption bundle that achieves a given utility level at the lowest possible cost, derived from the expenditure function minimizing p*x subject to u(x) = u.

Why are Marshallian and Hicksian demand important in economics?

Marshallian and Hicksian demand functions are important in economics because they capture consumer behavior under different conditions: Marshallian demand reflects quantity demanded based on income and prices (uncompensated demand), while Hicksian demand reflects quantity demanded based on utility maximization under constant utility with price changes (compensated demand), enabling analysis of substitution and income effects essential for welfare economics and policy evaluation.