The Lucas critique highlights the limitations of traditional macroeconomic models by emphasizing that policy evaluations must account for changes in agents' expectations and behavior over time. In contrast, the Sims critique focuses on the importance of incorporating uncertainty and the dynamic interplay of multiple economic variables without imposing rigid structural assumptions. Explore the distinct implications of these critiques for modern economic modeling and policy analysis.

Main Difference

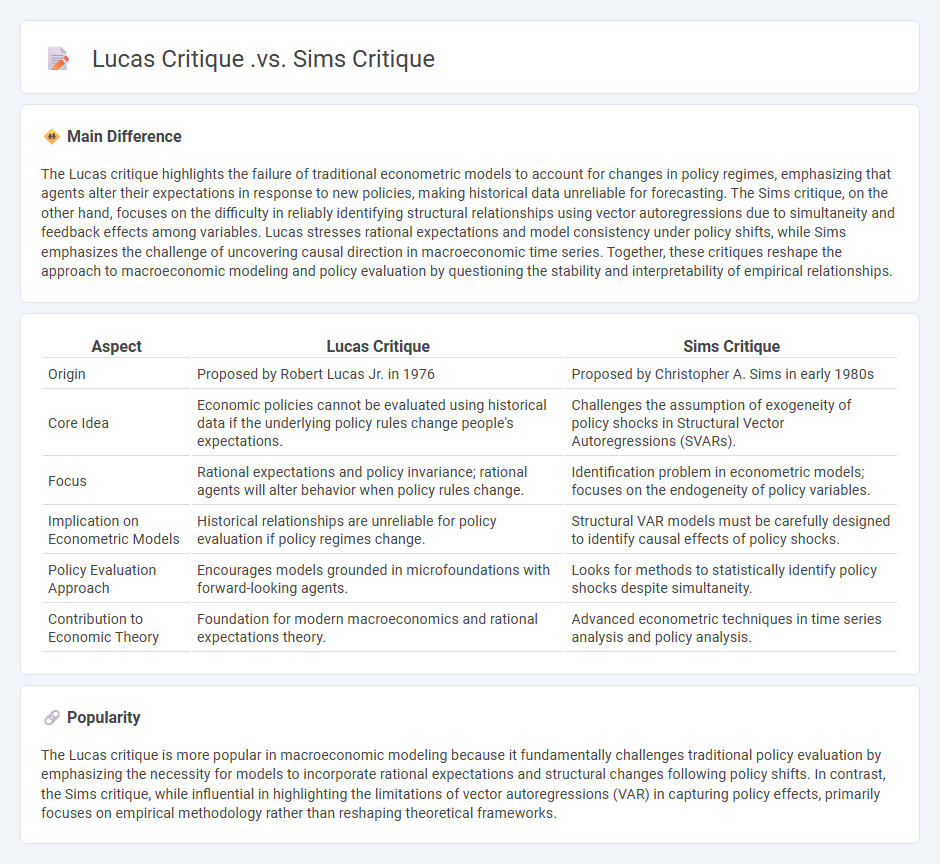

The Lucas critique highlights the failure of traditional econometric models to account for changes in policy regimes, emphasizing that agents alter their expectations in response to new policies, making historical data unreliable for forecasting. The Sims critique, on the other hand, focuses on the difficulty in reliably identifying structural relationships using vector autoregressions due to simultaneity and feedback effects among variables. Lucas stresses rational expectations and model consistency under policy shifts, while Sims emphasizes the challenge of uncovering causal direction in macroeconomic time series. Together, these critiques reshape the approach to macroeconomic modeling and policy evaluation by questioning the stability and interpretability of empirical relationships.

Connection

The Lucas critique highlights the importance of accounting for agents' expectations in macroeconomic policy models, emphasizing that traditional models fail when policy changes alter behavior. The Sims critique complements this by questioning the identification of structural shocks in vector autoregressions, advocating for models that incorporate rational expectations and structural interpretations. Both critiques fundamentally challenge traditional econometric modeling by insisting on the integration of expectations and structural parameters to improve policy analysis accuracy.

Comparison Table

| Aspect | Lucas Critique | Sims Critique |

|---|---|---|

| Origin | Proposed by Robert Lucas Jr. in 1976 | Proposed by Christopher A. Sims in early 1980s |

| Core Idea | Economic policies cannot be evaluated using historical data if the underlying policy rules change people's expectations. | Challenges the assumption of exogeneity of policy shocks in Structural Vector Autoregressions (SVARs). |

| Focus | Rational expectations and policy invariance; rational agents will alter behavior when policy rules change. | Identification problem in econometric models; focuses on the endogeneity of policy variables. |

| Implication on Econometric Models | Historical relationships are unreliable for policy evaluation if policy regimes change. | Structural VAR models must be carefully designed to identify causal effects of policy shocks. |

| Policy Evaluation Approach | Encourages models grounded in microfoundations with forward-looking agents. | Looks for methods to statistically identify policy shocks despite simultaneity. |

| Contribution to Economic Theory | Foundation for modern macroeconomics and rational expectations theory. | Advanced econometric techniques in time series analysis and policy analysis. |

Rational Expectations

Rational expectations theory posits that individuals and firms make decisions based on all available information, using models that accurately predict future economic variables. This concept, introduced by John F. Muth in 1961 and later expanded by Robert Lucas, challenges adaptive expectations by emphasizing forward-looking behavior in markets. Rational expectations minimize systematic forecasting errors, influencing policy effectiveness and macroeconomic models such as New Classical Economics. Empirical studies reveal mixed results, but the theory remains critical for understanding inflation dynamics, monetary policy, and market equilibrium.

Policy Invariance

Policy invariance in economics refers to the principle that economic agents' behavior remains consistent under different policy regimes, allowing for reliable counterfactual analysis. It underpins structural econometric models, ensuring that estimated parameters reflect fundamental economic relationships rather than policy-specific biases. This concept is critical for predicting the effects of policy changes, such as tax reforms or monetary interventions, based on observed data without the confounding influence of shifting behavioral responses. Empirical validation of policy invariance strengthens the credibility of economic forecasts and policy simulations used by governments and institutions.

Structural Models

Structural models in economics represent complex economic relationships through equations derived from economic theory, allowing analysis of policy impacts and behavioral responses. These models use measurable variables such as consumption, investment, and wages to estimate parameters that reflect economic mechanisms behind observed data. By incorporating causal assumptions, structural models enable economists to simulate different scenarios and predict outcomes under alternative policies or shocks. Prominent examples include the Ramsey-Cass-Koopmans growth model and DSGE models that analyze macroeconomic fluctuations and policy interventions.

Econometric Identification

Econometric identification ensures that economic models produce unique parameter estimates from observed data, enabling precise policy analysis and forecasting. Techniques such as instrumental variables, structural modeling, and natural experiments address issues of endogeneity and omitted variable bias. Identification conditions must be rigorously tested to validate causal inference in complex economic systems. Robust identification underpins empirical research in labor economics, finance, and macroeconomic policy evaluation.

Microfoundations

Microfoundations in economics refer to the study of individual agents' behaviors and decision-making processes that underpin macroeconomic phenomena. This approach involves analyzing consumers, firms, and markets using models grounded in utility maximization, profit optimization, and market equilibrium to explain aggregate outcomes. Microfoundations address limitations of traditional macroeconomic models by ensuring consistency with micro-level evidence and rational expectations. Major contributions include the development of dynamic stochastic general equilibrium (DSGE) models that integrate microeconomic principles into macroeconomic analysis.

Source and External Links

Christopher Sims - Econlib - The Lucas critique argues that policy changes alter the structural relationships in macroeconomic models, while Sims acknowledged this but argued such regime changes are rare and large-scale macroeconomic models remain useful for forecasting without necessarily identifying deep structural parameters.

Chap. I: The Lucas Critique L3-TSE: Macroeconomics - The Lucas Critique focuses on the invalidity of using past empirical relations for policy evaluation due to changing expectations, while the Sims Critique complements this by highlighting practical model implementation issues and the limits of standard econometric structures.

The Lucas Critique: Time Series Evidence - Sims (1982) argued the Lucas critique holds mainly when policy regime shifts are abrupt and permanent, but in many cases policy changes are incremental, so large-scale models can still be informative for forecasting under stable regimes.

FAQs

What is the Lucas critique?

The Lucas critique asserts that traditional economic policy evaluations fail because they do not account for changes in agents' behavior in response to new policies.

What is the Sims critique?

The Sims critique challenges the accuracy and validity of ethnic group categorizations in social science research, emphasizing the oversimplification and misrepresentation of complex identities.

How do the Lucas and Sims critiques differ?

Lucas critiques emphasize the importance of microfoundations and rational expectations in macroeconomic models, challenging traditional Keynesian approaches. Sims critiques focus on the identification problem in structural VAR models, arguing that policy evaluation requires careful consideration of simultaneous interactions without relying heavily on theoretical restrictions.

Why is the Lucas critique important for economic modeling?

The Lucas critique is important for economic modeling because it highlights that traditional models fail to predict policy effects accurately since they do not account for changes in agents' behavior or expectations in response to new policies.

What issue does the Sims critique raise in macroeconomic analysis?

The Sims critique raises the issue that traditional macroeconomic models fail to account for changes in policy regimes affecting the relationships between economic variables, leading to biased or inconsistent policy evaluation.

How did the Lucas critique impact policy evaluation?

The Lucas critique revealed that traditional policy evaluation models fail to account for changes in agents' expectations, leading to the development of dynamic, micro-founded models that incorporate rational expectations for more accurate policy analysis.

How do the Lucas and Sims critiques influence modern econometrics?

The Lucas critique emphasizes the need for models with microfoundations and policy-invariant parameters, leading modern econometrics to prioritize structural models that account for agents' expectations; Sims' critique promotes using vector autoregressions (VARs) to capture dynamic interactions without imposing strong priors, influencing widespread adoption of VAR techniques for empirical macroeconomic analysis.