Pigovian taxes target negative externalities by imposing charges proportional to the social cost of harmful activities, promoting efficient resource allocation and behavioral changes. Lump-sum taxes, in contrast, levy a fixed amount regardless of economic behavior, minimizing distortion but lacking incentives to reduce negative externalities. Explore the differences and impacts of these taxation methods to understand their roles in economic policy design.

Main Difference

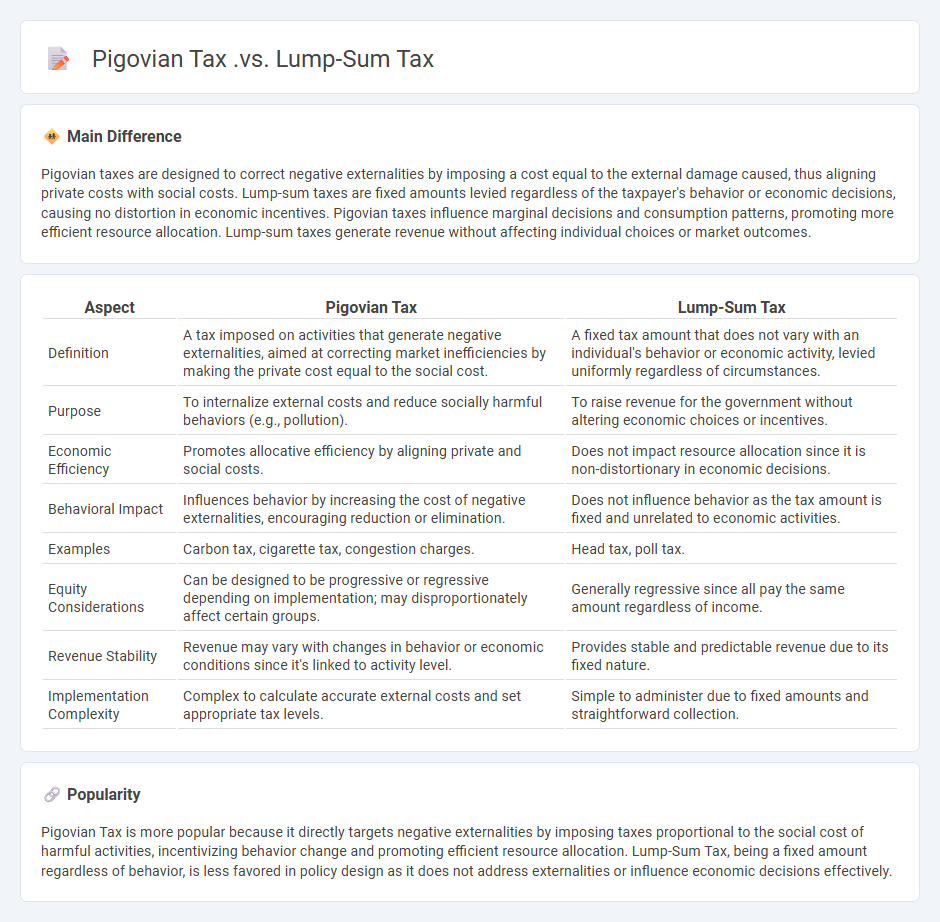

Pigovian taxes are designed to correct negative externalities by imposing a cost equal to the external damage caused, thus aligning private costs with social costs. Lump-sum taxes are fixed amounts levied regardless of the taxpayer's behavior or economic decisions, causing no distortion in economic incentives. Pigovian taxes influence marginal decisions and consumption patterns, promoting more efficient resource allocation. Lump-sum taxes generate revenue without affecting individual choices or market outcomes.

Connection

Pigovian tax and lump-sum tax are connected through their roles in economic policy aimed at addressing externalities and government revenue needs. Pigovian taxes specifically target negative externalities by imposing a cost equal to the external damage, thereby aligning private costs with social costs. Lump-sum taxes do not distort economic behavior as they are fixed amounts irrespective of actions, often used to finance public goods or offset income inequalities, complementing Pigovian taxes' efficiency in correcting market failures.

Comparison Table

| Aspect | Pigovian Tax | Lump-Sum Tax |

|---|---|---|

| Definition | A tax imposed on activities that generate negative externalities, aimed at correcting market inefficiencies by making the private cost equal to the social cost. | A fixed tax amount that does not vary with an individual's behavior or economic activity, levied uniformly regardless of circumstances. |

| Purpose | To internalize external costs and reduce socially harmful behaviors (e.g., pollution). | To raise revenue for the government without altering economic choices or incentives. |

| Economic Efficiency | Promotes allocative efficiency by aligning private and social costs. | Does not impact resource allocation since it is non-distortionary in economic decisions. |

| Behavioral Impact | Influences behavior by increasing the cost of negative externalities, encouraging reduction or elimination. | Does not influence behavior as the tax amount is fixed and unrelated to economic activities. |

| Examples | Carbon tax, cigarette tax, congestion charges. | Head tax, poll tax. |

| Equity Considerations | Can be designed to be progressive or regressive depending on implementation; may disproportionately affect certain groups. | Generally regressive since all pay the same amount regardless of income. |

| Revenue Stability | Revenue may vary with changes in behavior or economic conditions since it's linked to activity level. | Provides stable and predictable revenue due to its fixed nature. |

| Implementation Complexity | Complex to calculate accurate external costs and set appropriate tax levels. | Simple to administer due to fixed amounts and straightforward collection. |

Externalities

Externalities in economics refer to costs or benefits arising from economic activities that affect third parties without being reflected in market prices. Negative externalities, such as pollution from industrial production, impose social costs not borne by producers, leading to market inefficiencies. Positive externalities include benefits like improved public health from vaccinations, which enhance societal welfare beyond individual gains. Addressing externalities often requires government intervention through taxes, subsidies, or regulation to align private incentives with social optimality.

Marginal Social Cost

Marginal Social Cost (MSC) represents the total cost imposed on society by producing one additional unit of a good or service, including both private costs and externalities. It is crucial in environmental economics, where pollution or resource depletion generates negative externalities not reflected in market prices. Calculating MSC involves summing marginal private costs and marginal external costs to guide efficient resource allocation and policy decisions. Measuring MSC accurately helps establish optimal taxes or regulations aimed at reducing social harm and achieving sustainable economic outcomes.

Deadweight Loss

Deadweight loss in economics represents the loss of economic efficiency when the equilibrium outcome is not achievable or not achieved. It occurs due to market distortions such as taxes, subsidies, price ceilings, or floors that prevent supply and demand from reaching equilibrium. This inefficiency leads to a reduction in total surplus, comprising consumer and producer surplus. Quantifying deadweight loss helps economists assess the cost of interventions like taxation or monopolies on market welfare.

Tax Incidence

Tax incidence measures the distribution of tax burdens between buyers and sellers in a market, reflecting how taxes affect prices and quantities. The economic concept analyzes who truly bears the cost of a tax, depending on price elasticity of demand and supply. In markets with inelastic demand, consumers typically shoulder a larger share of the tax, whereas inelastic supply shifts more burden to producers. This analysis guides policymakers in designing taxes that minimize economic distortions and inefficiencies.

Economic Efficiency

Economic efficiency measures the optimal allocation of resources to maximize output and minimize waste in an economy. It occurs when goods and services are produced at their lowest possible cost and distributed according to consumer preferences. Key types include allocative efficiency, where resources meet consumer demand, and productive efficiency, where production uses the least input for maximum output. Economists use indicators such as Pareto efficiency and productivity ratios to assess economic efficiency across markets.

Source and External Links

Pigovian Questions - Pigouvian taxes are beneficial as they correct market failures and can be combined with lump-sum rebates or reductions in other taxes.

Pigouvian Tax - A Pigouvian tax is used to internalize negative externalities by adjusting market prices to reflect the true social cost, whereas a lump-sum tax is a fixed amount paid by each taxpayer.

Limitation of Pigouvian Taxes - Pigouvian taxes, when combined with lump-sum taxes, can achieve optimal long-run competitive equilibrium and social outcomes.

FAQs

What is a Pigovian tax?

A Pigovian tax is a government-imposed tax on activities that generate negative externalities, designed to correct market inefficiencies by internalizing social costs.

What is a lump-sum tax?

A lump-sum tax is a fixed tax amount imposed on individuals or entities regardless of income, consumption, or economic behavior.

How do Pigovian and lump-sum taxes differ in purpose?

Pigovian taxes aim to correct negative externalities by increasing costs on harmful activities, while lump-sum taxes generate revenue without influencing behavior.

What effects do Pigovian taxes have on consumer behavior?

Pigovian taxes reduce consumption of negative externality goods by increasing their prices, incentivizing consumers to choose healthier or environmentally friendly alternatives.

Are lump-sum taxes considered fair or regressive?

Lump-sum taxes are considered regressive because they impose the same fixed amount on all taxpayers regardless of income, disproportionately burdening lower-income individuals.

How do governments use Pigovian taxes in public policy?

Governments use Pigovian taxes to internalize negative externalities by imposing fees on activities that generate social costs, such as pollution, encouraging producers and consumers to reduce harmful behaviors and fund public goods or environmental programs.

Which tax is more efficient in correcting externalities?

Pigouvian tax is more efficient in correcting externalities by directly pricing the negative external cost.