Rational expectations theory assumes individuals use all available information efficiently to forecast future economic variables, resulting in unbiased predictions. Adaptive expectations theory suggests that individuals form future expectations based solely on past experiences and adjust them gradually over time. Explore the nuances of these contrasting models to better understand economic forecasting methods.

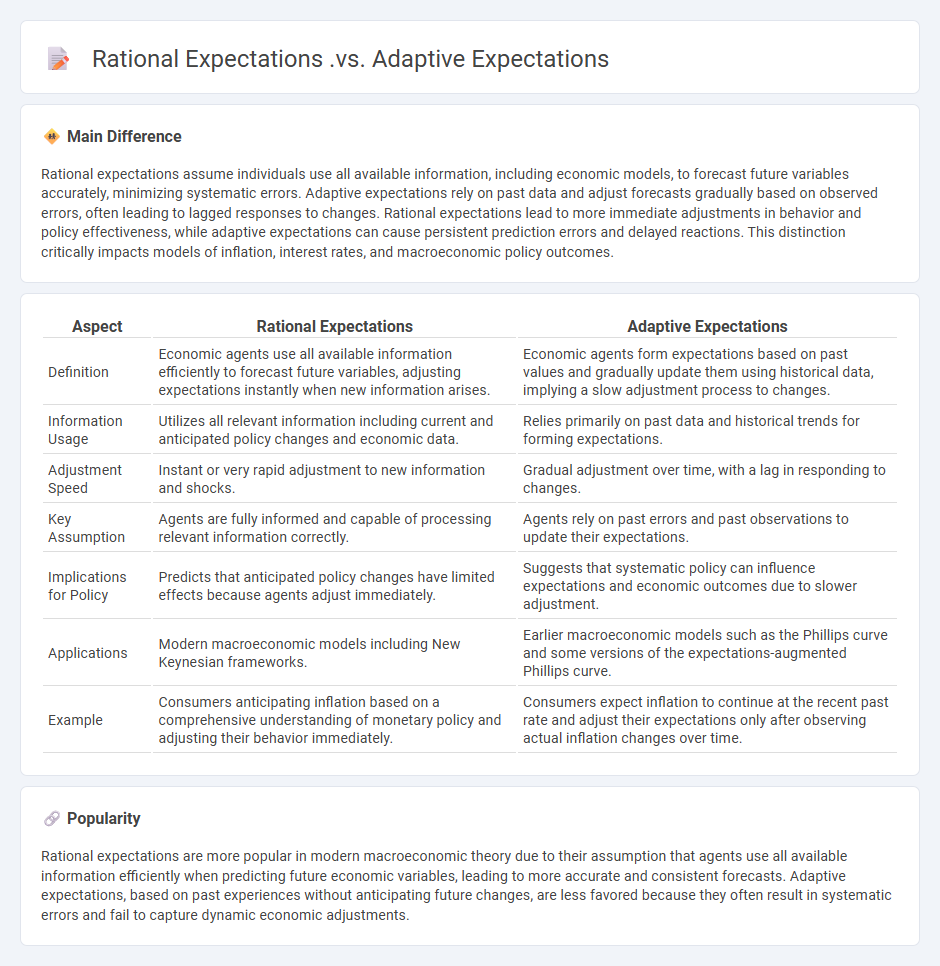

Main Difference

Rational expectations assume individuals use all available information, including economic models, to forecast future variables accurately, minimizing systematic errors. Adaptive expectations rely on past data and adjust forecasts gradually based on observed errors, often leading to lagged responses to changes. Rational expectations lead to more immediate adjustments in behavior and policy effectiveness, while adaptive expectations can cause persistent prediction errors and delayed reactions. This distinction critically impacts models of inflation, interest rates, and macroeconomic policy outcomes.

Connection

Rational expectations and adaptive expectations are connected through their approach to forecasting economic variables, where rational expectations assume agents use all available information efficiently, while adaptive expectations rely on past data to predict future outcomes. Both models influence inflation expectations and monetary policy effectiveness, with rational expectations addressing potential forecast errors more comprehensively. Understanding their interaction helps economists analyze how expectations shape market behavior and policy responses.

Comparison Table

| Aspect | Rational Expectations | Adaptive Expectations |

|---|---|---|

| Definition | Economic agents use all available information efficiently to forecast future variables, adjusting expectations instantly when new information arises. | Economic agents form expectations based on past values and gradually update them using historical data, implying a slow adjustment process to changes. |

| Information Usage | Utilizes all relevant information including current and anticipated policy changes and economic data. | Relies primarily on past data and historical trends for forming expectations. |

| Adjustment Speed | Instant or very rapid adjustment to new information and shocks. | Gradual adjustment over time, with a lag in responding to changes. |

| Key Assumption | Agents are fully informed and capable of processing relevant information correctly. | Agents rely on past errors and past observations to update their expectations. |

| Implications for Policy | Predicts that anticipated policy changes have limited effects because agents adjust immediately. | Suggests that systematic policy can influence expectations and economic outcomes due to slower adjustment. |

| Applications | Modern macroeconomic models including New Keynesian frameworks. | Earlier macroeconomic models such as the Phillips curve and some versions of the expectations-augmented Phillips curve. |

| Example | Consumers anticipating inflation based on a comprehensive understanding of monetary policy and adjusting their behavior immediately. | Consumers expect inflation to continue at the recent past rate and adjust their expectations only after observing actual inflation changes over time. |

Information Utilization

Information utilization in economics refers to the efficient gathering, processing, and application of data to enhance decision-making processes in markets and organizations. It plays a critical role in reducing information asymmetry, thus enabling more accurate pricing, resource allocation, and risk assessment. Advanced technologies and big data analytics have significantly improved the ability to harness economic information for forecasting and policy development. Empirical studies demonstrate that markets with higher levels of information transparency tend to exhibit increased liquidity and lower transaction costs.

Forecasting Method

Forecasting methods in economics leverage quantitative techniques such as time series analysis, econometric modeling, and machine learning to predict future economic indicators. These methods utilize historical data on GDP, inflation rates, unemployment, and consumer spending to generate accurate projections. Economists use models like ARIMA, Vector Autoregression (VAR), and Bayesian inference to capture complex relationships and trends within economic systems. Accurate forecasting supports policy decisions, financial planning, and risk management across various sectors.

Adjustment Speed

Adjustment speed in economics measures how quickly an economic variable, such as prices or wages, responds to changes in market conditions or shocks. It is crucial in models of inflation dynamics, where faster adjustment speeds can lead to more stable price levels. Empirical studies often estimate adjustment speeds using error-correction models to quantify the speed at which variables return to equilibrium. Understanding adjustment speed helps policymakers design interventions that minimize economic volatility and improve market efficiency.

Policy Effectiveness

Policy effectiveness in economics measures how well government interventions achieve intended outcomes, such as economic growth, inflation control, or unemployment reduction. Evaluating effectiveness involves analyzing policy tools like fiscal stimulus, monetary adjustments, and regulatory reforms against real economic indicators. Consideration of lag effects, behavioral responses, and external factors is essential for accurate assessment. Empirical studies often utilize econometric models and historical data to quantify policy impacts and inform future decisions.

Systematic Errors

Systematic errors in economics refer to consistent, predictable inaccuracies that skew data collection, measurement, or analysis, leading to biased conclusions and faulty economic models. These errors can arise from flawed survey design, misreported data by respondents, or inherent biases in econometric techniques. Understanding and correcting for systematic errors is essential for accurate economic forecasting, policy formulation, and research integrity. Prominent examples include errors in inflation measurement or persistent bias in income surveys.

Source and External Links

Adaptive Expectations - What Is It, Limitations - WallStreetMojo [adaptive expectations are backward-looking, using only past data, while rational expectations are forward-looking and incorporate all available information]

Chapter 4 Expectations | Macroeconomics - Bookdown [adaptive expectations rely on historical trends, causing slower adjustment to new policies, whereas rational expectations allow agents to quickly adapt to changes by anticipating the future based on available information]

Principles of Economics - Vaia [adaptive expectations use past outcomes to forecast the future, while rational expectations use current and all relevant information to make forecasts]

FAQs

What are economic expectations?

Economic expectations are predictions or anticipations about future economic conditions, such as inflation rates, unemployment levels, GDP growth, and market trends, which influence decision-making by consumers, businesses, and policymakers.

What is the difference between rational and adaptive expectations?

Rational expectations assume individuals use all available information and economic models to predict future variables accurately, while adaptive expectations rely on past data and adjust predictions gradually based on historical errors.

How are rational expectations formed?

Rational expectations are formed by individuals using all available information, including past data, current policies, and economic models, to make unbiased and statistically accurate forecasts about future economic variables.

How are adaptive expectations calculated?

Adaptive expectations are calculated using the formula: Et+1 = Et + l(At - Et) where Et+1 is the expected value for the next period, Et is the current expectation, At is the actual value observed, and l (0 < l <= 1) is the adjustment coefficient indicating the speed of expectation adjustment.

What is the impact of rational expectations on monetary policy?

Rational expectations lead to monetary policy ineffectiveness by causing individuals to anticipate policy actions, neutralizing their intended effects on output and employment while primarily influencing only inflation.

How do adaptive expectations affect inflation predictions?

Adaptive expectations cause inflation predictions to rely heavily on past inflation rates, leading to systematic lags in adjusting to new inflation trends.

Why do rational expectations matter in economic forecasting?

Rational expectations matter in economic forecasting because they ensure that predictions incorporate all available information, reducing systematic forecasting errors and improving the accuracy of models in anticipating economic behavior.