Backtesting evaluates trading strategies by comparing predicted outcomes with historical market data to measure accuracy and performance. Stress testing simulates extreme market conditions to assess the resilience and risk exposure of financial models under adverse scenarios. Explore how these methods enhance risk management and investment decision-making.

Main Difference

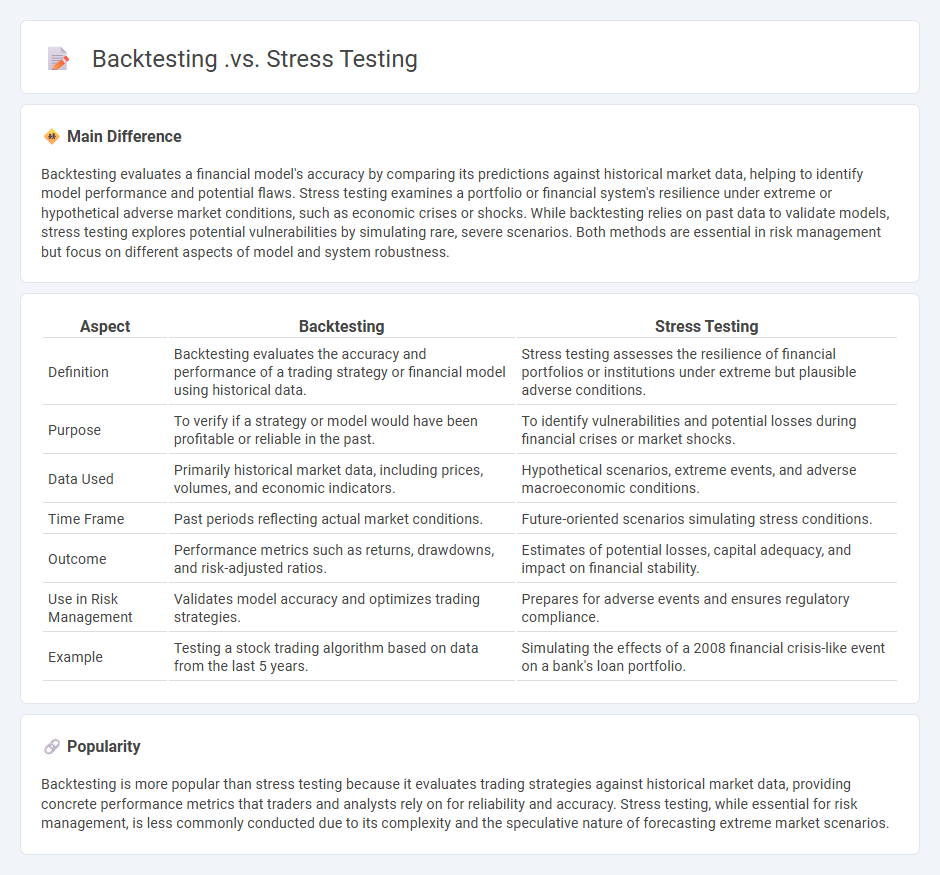

Backtesting evaluates a financial model's accuracy by comparing its predictions against historical market data, helping to identify model performance and potential flaws. Stress testing examines a portfolio or financial system's resilience under extreme or hypothetical adverse market conditions, such as economic crises or shocks. While backtesting relies on past data to validate models, stress testing explores potential vulnerabilities by simulating rare, severe scenarios. Both methods are essential in risk management but focus on different aspects of model and system robustness.

Connection

Backtesting evaluates the accuracy of financial models by comparing predicted outcomes with historical data, ensuring reliability and effectiveness. Stress testing examines model performance under extreme or adverse market conditions to assess risk exposure and resilience. Together, these techniques validate financial models by identifying weaknesses and enhancing risk management strategies for robust decision-making.

Comparison Table

| Aspect | Backtesting | Stress Testing |

|---|---|---|

| Definition | Backtesting evaluates the accuracy and performance of a trading strategy or financial model using historical data. | Stress testing assesses the resilience of financial portfolios or institutions under extreme but plausible adverse conditions. |

| Purpose | To verify if a strategy or model would have been profitable or reliable in the past. | To identify vulnerabilities and potential losses during financial crises or market shocks. |

| Data Used | Primarily historical market data, including prices, volumes, and economic indicators. | Hypothetical scenarios, extreme events, and adverse macroeconomic conditions. |

| Time Frame | Past periods reflecting actual market conditions. | Future-oriented scenarios simulating stress conditions. |

| Outcome | Performance metrics such as returns, drawdowns, and risk-adjusted ratios. | Estimates of potential losses, capital adequacy, and impact on financial stability. |

| Use in Risk Management | Validates model accuracy and optimizes trading strategies. | Prepares for adverse events and ensures regulatory compliance. |

| Example | Testing a stock trading algorithm based on data from the last 5 years. | Simulating the effects of a 2008 financial crisis-like event on a bank's loan portfolio. |

Historical Data

Historical data in finance refers to past market prices, trading volumes, and economic indicators collected over time to analyze trends and forecast future performance. It encompasses stock prices, interest rates, currency exchange rates, and macroeconomic variables such as GDP growth and unemployment rates. Financial analysts and quantitative models utilize this data to develop investment strategies, measure risk, and test hypotheses about asset behavior. Accessing reliable historical financial datasets from sources like Bloomberg, Reuters, and government databases enhances the accuracy of predictive financial models.

Scenario Analysis

Scenario analysis in finance evaluates the impact of different economic conditions on investment portfolios, cash flows, or business performance. It involves modeling various scenarios such as recession, inflation spikes, or market booms to assess potential risks and returns. Financial institutions and corporations use scenario analysis to enhance risk management and inform strategic decision-making. Tools like Monte Carlo simulations and stress testing support the quantitative assessment of these scenarios.

Model Validation

Model validation in finance ensures the accuracy and reliability of financial models used for risk assessment, pricing, and forecasting. It involves back-testing, sensitivity analysis, and benchmarking against historical data to detect biases or errors. Regulatory frameworks like Basel III mandate rigorous validation to maintain model integrity and compliance in banking institutions. Effective model validation minimizes financial risk and supports informed decision-making across trading, credit, and investment portfolios.

Risk Assessment

Risk assessment in finance involves identifying, analyzing, and quantifying potential losses associated with investment portfolios, credit exposures, or market fluctuations. Techniques such as Value at Risk (VaR), stress testing, and scenario analysis quantify uncertainty and guide decision-making. Regulatory frameworks like Basel III require financial institutions to maintain adequate capital reserves based on measured risk levels. Effective risk assessment reduces exposure to default, market volatility, liquidity crises, and operational failures.

Performance Evaluation

Performance evaluation in finance involves assessing the effectiveness of investment portfolios, financial strategies, and managerial decisions using quantitative metrics such as return on investment (ROI), alpha, beta, and the Sharpe ratio. Analysts employ tools like benchmarking against market indices, risk-adjusted returns, and variance analysis to measure financial outcomes and identify areas for improvement. Key performance indicators (KPIs) include profitability ratios, liquidity ratios, and efficiency ratios that provide insights into an organization's financial health and operational success. Accurate performance evaluation supports informed decision-making, enhances portfolio management, and drives value creation in financial markets.

Source and External Links

Backtesting - Meaning, Example, Trading, Vs Stress Testing - Backtesting tests a model or strategy using historical data to evaluate past performance, while stress testing assesses portfolio resistance to possible future market threats using historical, simulated, and hypothetical scenarios.

Stress Testing Vs Scenario Analysis Vs Backtesting | Forum - Stress testing evaluates the impact of unlikely but plausible events on portfolios; backtesting compares predicted results with actual historical data to test model accuracy; scenario analysis is related but distinct.

An Academic Perspective on Backtesting and Stress-Testing - Backtesting compares observed outcomes with model expectations (forecast evaluation), while stress-testing examines model outputs under extreme or outlier conditions through scenario analysis and case studies.

FAQs

What is backtesting in finance?

Backtesting in finance is the process of evaluating a trading strategy or model using historical market data to assess its potential effectiveness and reliability before applying it in real-time trading.

What is stress testing in risk management?

Stress testing in risk management evaluates a financial institution's ability to withstand adverse economic scenarios by simulating extreme but plausible market conditions that impact assets, liabilities, and capital adequacy.

How does backtesting differ from stress testing?

Backtesting evaluates a trading strategy's performance using historical market data, while stress testing assesses its resilience under hypothetical extreme or adverse market conditions.

What are the main objectives of backtesting?

Backtesting aims to evaluate the effectiveness of a trading strategy by applying it to historical market data, assess its risk and return profiles, identify potential weaknesses, and validate its viability before live deployment.

What scenarios are used in stress testing?

Stress testing scenarios include extreme workload spikes, peak user concurrency, limited resource availability (CPU, memory, bandwidth), sudden traffic surges, database overloads, and failure of dependent services.

When should you use backtesting versus stress testing?

Use backtesting to evaluate the accuracy of predictive models based on historical data; use stress testing to assess system or portfolio resilience under extreme, hypothetical scenarios.

What are the limitations of each method?

Each method's limitations include: Method A struggles with scalability in large datasets; Method B has high computational cost; Method C produces lower accuracy in noisy environments; Method D requires extensive labeled data; Method E lacks robustness against data variability.