Leveraged Buyouts (LBO) involve acquiring a company using significant amounts of borrowed capital, often secured by the company's assets, to finance the purchase. Management Buyouts (MBO) occur when a company's existing management team acquires the business, typically using a combination of personal funds and external financing. Explore further to understand the strategic differences and financial implications between LBOs and MBOs.

Main Difference

An LBO (Leveraged Buyout) involves acquiring a company primarily through borrowed funds, often by external investors or private equity firms. An MBO (Management Buyout) occurs when a company's existing management team acquires the business, usually using a combination of personal funds and external financing. LBOs typically target larger, publicly traded companies, while MBOs focus on privately held businesses with motivated management teams. The key distinction lies in the buyer's identity and the source of financing used to execute the transaction.

Connection

Leveraged Buyouts (LBO) and Management Buyouts (MBO) are connected through their use of significant debt to finance the acquisition of a company, with MBOs specifically involving the existing management team purchasing the business. Both strategies aim to transfer ownership while leveraging future cash flows to repay debt, often resulting in management gaining greater control and alignment with company performance. The overlap lies in the financial structuring and strategic objectives, where MBOs are a subset of LBOs focused on insiders' buyouts.

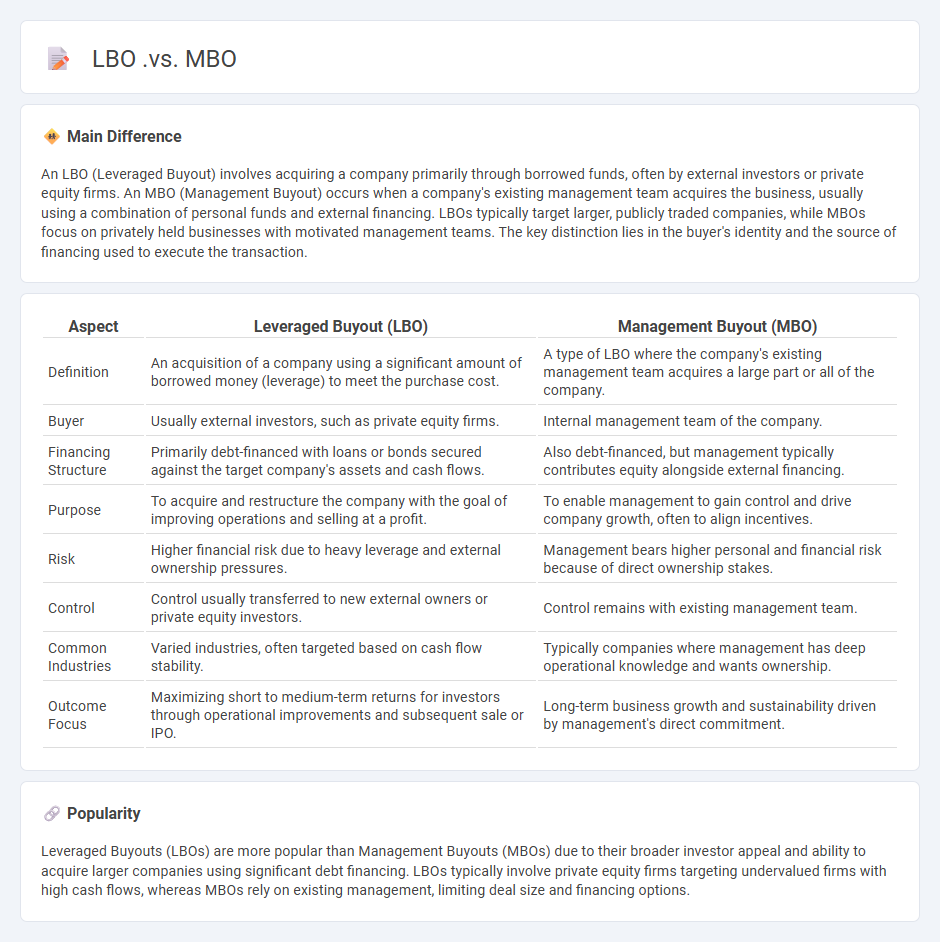

Comparison Table

| Aspect | Leveraged Buyout (LBO) | Management Buyout (MBO) |

|---|---|---|

| Definition | An acquisition of a company using a significant amount of borrowed money (leverage) to meet the purchase cost. | A type of LBO where the company's existing management team acquires a large part or all of the company. |

| Buyer | Usually external investors, such as private equity firms. | Internal management team of the company. |

| Financing Structure | Primarily debt-financed with loans or bonds secured against the target company's assets and cash flows. | Also debt-financed, but management typically contributes equity alongside external financing. |

| Purpose | To acquire and restructure the company with the goal of improving operations and selling at a profit. | To enable management to gain control and drive company growth, often to align incentives. |

| Risk | Higher financial risk due to heavy leverage and external ownership pressures. | Management bears higher personal and financial risk because of direct ownership stakes. |

| Control | Control usually transferred to new external owners or private equity investors. | Control remains with existing management team. |

| Common Industries | Varied industries, often targeted based on cash flow stability. | Typically companies where management has deep operational knowledge and wants ownership. |

| Outcome Focus | Maximizing short to medium-term returns for investors through operational improvements and subsequent sale or IPO. | Long-term business growth and sustainability driven by management's direct commitment. |

Ownership Structure

Ownership structure in finance refers to the distribution of equity shares among individuals, institutional investors, and entities within a company. It directly influences corporate control, governance practices, and decision-making processes by determining who holds voting rights and the ability to affect management. Common forms include concentrated ownership, where a few shareholders hold significant stakes, and dispersed ownership, characterized by many small shareholders. Understanding ownership structure is crucial for assessing agency problems, shareholder activism, and firm performance.

Financing Sources

Financing sources in finance include equity financing, debt financing, and hybrid instruments, each providing distinct advantages for capital structure optimization. Equity financing involves raising capital through the sale of shares, enabling businesses to access funds without incurring debt obligations. Debt financing includes loans, bonds, and credit lines, which require regular interest payments but do not dilute ownership. Hybrid instruments such as convertible bonds combine features of both equity and debt, allowing flexibility in corporate financing strategies.

Management Involvement

Management involvement in finance significantly impacts strategic decision-making, financial planning, and risk management within organizations. Active participation by executives ensures effective allocation of resources, enhances budgeting accuracy, and drives compliance with regulatory standards like GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). Financial managers collaborate closely with departments to optimize capital structure, analyze investment opportunities, and maximize shareholder value. Data-driven insights and transparent reporting enable management to adapt swiftly to market fluctuations and maintain financial stability.

Risk Allocation

Risk allocation in finance involves distributing potential risks among various parties, such as investors, insurers, and financial institutions, to minimize overall exposure. It plays a critical role in portfolio management, where diversification strategies allocate risk across different asset classes like equities, bonds, and commodities. Financial derivatives, including options and futures, are essential instruments enabling effective risk transfer and hedging. Proper risk allocation enhances capital efficiency and supports regulatory compliance under frameworks like Basel III.

Value Creation Strategies

Effective value creation strategies in finance focus on optimizing capital allocation to maximize shareholder wealth. Leveraging detailed financial analysis and performance metrics helps identify high-return investment opportunities and cost efficiencies. Integrating risk management frameworks ensures sustainable growth by mitigating potential financial exposures. Enhancing operational efficiencies and strategic mergers or acquisitions frequently drive long-term value in competitive markets.

Source and External Links

Leveraged Buyout: MBI vs: LBO: Understanding the Key Differences - The primary difference is financing: MBOs are executed by the existing management team using a combination of personal and external funds and retain control, while LBOs are led by external investors using significant debt, often resulting in less management control and higher financial risk.

What is the Difference Between Management Buyout (MBO) and Leveraged Buyout (LBO)? - MBOs involve internal management leading the purchase with moderate risk and focus on continuity, while LBOs involve external investors using heavy debt for financial returns and operational improvements, carrying higher risk due to leverage.

Management Buyout (MBO) | Transaction Structure + Examples - An MBO is a type of LBO where management leads the transaction and contributes equity, aligning incentives and signaling confidence in running the company better, in contrast to standard LBOs mostly driven by outside investors.

FAQs

What is a leveraged buyout?

A leveraged buyout (LBO) is a financial transaction where a company is acquired using a significant amount of borrowed funds, with the assets of the acquired company often used as collateral for the loans.

What is a management buyout?

A management buyout (MBO) is a transaction where a company's existing management team acquires a significant portion or all of the business, gaining ownership and control.

How do LBO and MBO structures differ?

LBO (Leveraged Buyout) involves acquiring a company using significant debt, often by external investors, while MBO (Management Buyout) occurs when a company's existing management team buys out the company, typically using a combination of personal funds and external financing.

What are the main risks of an LBO?

The main risks of a Leveraged Buyout (LBO) include high debt burden causing financial distress, reduced operational flexibility, sensitivity to interest rate fluctuations, and potential decline in company value impacting debt repayment.

Why do managers prefer MBOs?

Managers prefer Management by Objectives (MBO) because it aligns individual goals with organizational objectives, enhances employee motivation, improves performance measurement, and facilitates clearer communication and accountability.

How is funding secured in an LBO vs. MBO?

In an LBO, funding is primarily secured through a combination of debt financing from banks and bond issuance, leveraging the target company's assets and cash flows, whereas in an MBO, funding relies more on a mix of management equity contributions, private equity investments, and bank debt with a focus on retaining management control.

What are the outcomes for employees in LBO and MBO deals?

Employees in LBO (Leveraged Buyout) deals often face job restructuring, potential layoffs, and pressure to improve operational efficiency, while MBO (Management Buyout) deals typically result in greater employee stability and motivation due to existing management retaining control.