Internal Rate of Return (IRR) measures the profitability of potential investments by calculating the discount rate that makes the net present value (NPV) of cash flows zero. Modified Internal Rate of Return (MIRR) addresses IRR's limitations by incorporating cost of capital and reinvestment rates, providing a more accurate reflection of an investment's profitability. Explore the differences between IRR and MIRR to optimize your investment decision-making strategies.

Main Difference

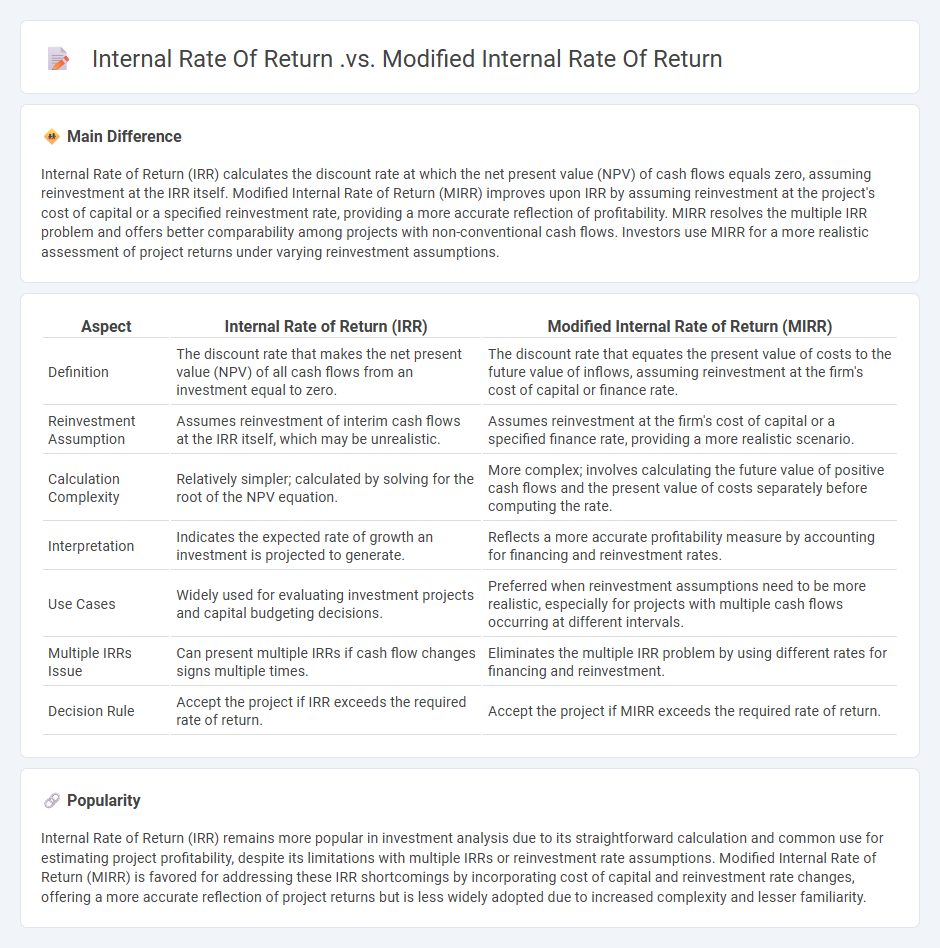

Internal Rate of Return (IRR) calculates the discount rate at which the net present value (NPV) of cash flows equals zero, assuming reinvestment at the IRR itself. Modified Internal Rate of Return (MIRR) improves upon IRR by assuming reinvestment at the project's cost of capital or a specified reinvestment rate, providing a more accurate reflection of profitability. MIRR resolves the multiple IRR problem and offers better comparability among projects with non-conventional cash flows. Investors use MIRR for a more realistic assessment of project returns under varying reinvestment assumptions.

Connection

Internal Rate of Return (IRR) and Modified Internal Rate of Return (MIRR) are connected as financial metrics used to evaluate investment profitability, with MIRR addressing IRR's limitations by incorporating reinvestment rate assumptions and cost of capital. IRR calculates the discount rate that makes the net present value (NPV) of cash flows zero, assuming reinvestment at the IRR itself. MIRR provides a more accurate reflection of an investment's performance by assuming reinvestment at the firm's cost of capital, enhancing decision-making in capital budgeting.

Comparison Table

| Aspect | Internal Rate of Return (IRR) | Modified Internal Rate of Return (MIRR) |

|---|---|---|

| Definition | The discount rate that makes the net present value (NPV) of all cash flows from an investment equal to zero. | The discount rate that equates the present value of costs to the future value of inflows, assuming reinvestment at the firm's cost of capital or finance rate. |

| Reinvestment Assumption | Assumes reinvestment of interim cash flows at the IRR itself, which may be unrealistic. | Assumes reinvestment at the firm's cost of capital or a specified finance rate, providing a more realistic scenario. |

| Calculation Complexity | Relatively simpler; calculated by solving for the root of the NPV equation. | More complex; involves calculating the future value of positive cash flows and the present value of costs separately before computing the rate. |

| Interpretation | Indicates the expected rate of growth an investment is projected to generate. | Reflects a more accurate profitability measure by accounting for financing and reinvestment rates. |

| Use Cases | Widely used for evaluating investment projects and capital budgeting decisions. | Preferred when reinvestment assumptions need to be more realistic, especially for projects with multiple cash flows occurring at different intervals. |

| Multiple IRRs Issue | Can present multiple IRRs if cash flow changes signs multiple times. | Eliminates the multiple IRR problem by using different rates for financing and reinvestment. |

| Decision Rule | Accept the project if IRR exceeds the required rate of return. | Accept the project if MIRR exceeds the required rate of return. |

Discount Rate

The discount rate in finance refers to the interest rate used to determine the present value of future cash flows, reflecting the time value of money and investment risk. It plays a crucial role in discounted cash flow (DCF) analysis, capital budgeting, and valuation models by adjusting future amounts to their current worth. Central banks also set discount rates, influencing borrowing costs and monetary policy. A higher discount rate decreases present value, signifying greater risk or opportunity cost.

Reinvestment Assumption

The reinvestment assumption in finance postulates that all interim cash flows generated by an investment are reinvested at the investment's internal rate of return (IRR). This assumption impacts the calculation of IRR, potentially overstating the expected profitability if reinvestment opportunities yield lower returns. Analysts often compare IRR with the modified internal rate of return (MIRR), which assumes reinvestment at the firm's cost of capital, providing a more conservative performance measure. Understanding the reinvestment assumption is crucial for accurately evaluating project viability and capital budgeting decisions.

Cash Flow Timing

Cash flow timing refers to the specific schedule when cash inflows and outflows occur within a business or financial project, impacting liquidity and financial planning. Proper management of cash flow timing ensures that a company maintains sufficient cash on hand to meet its operational expenses and investment opportunities. Businesses analyze cash flow projections by month or quarter to optimize the timing of receivables and payables, thereby minimizing the costs associated with borrowing or idle cash. Accurate timing supports better decision-making in areas such as budgeting, working capital management, and risk assessment.

Project Evaluation

Project evaluation in finance involves assessing the viability, risks, and expected returns of investment opportunities using methods such as Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period. Financial analysts apply discounted cash flow analysis to estimate future cash flows and determine project profitability. Sensitivity analysis and scenario planning help quantify potential uncertainties and their impact on project outcomes. Thorough project evaluation supports effective capital budgeting decisions and strategic financial planning.

Comparative Analysis

Comparative analysis in finance involves evaluating financial statements, ratios, and performance metrics across different companies or time periods to identify trends and operational efficiencies. Key financial documents analyzed include balance sheets, income statements, and cash flow statements, providing insights into liquidity, profitability, and solvency. This approach aids investors and analysts in making informed decisions by benchmarking against industry standards and historical data. Tools such as ratio analysis, vertical and horizontal analysis enhance the precision of financial comparisons.

Source and External Links

Internal Rate of Return (IRR): Definition and Role in PE - Moonfare - The IRR is the discount rate that makes the net present value (NPV) of all future cash flows equal zero, serving as a measure of an investment's profitability and seen as an annualized growth rate similar to CAGR.

Modified Internal Rate of Return (MIRR): Definition, Formula - MIRR adjusts IRR by incorporating specified financing and reinvestment rates for cash flows, providing a more realistic profitability measure when cash inflows and outflows occur at different rates or multiple periods.

Modified Internal Rate of Return (MIRR) - Overview, How to Calculate - Unlike IRR, which can yield multiple or unrealistic solutions, MIRR always produces a single solution by factoring in the cost of capital and reinvestment rate, offering a more accurate investment return measure especially for projects with varying cash flows over time.

FAQs

What is Internal Rate of Return?

Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of all cash flows from a specific investment equal to zero.

What is Modified Internal Rate of Return?

Modified Internal Rate of Return (MIRR) is a financial metric that adjusts the Internal Rate of Return (IRR) by assuming reinvestment of cash flows at the project's cost of capital and providing a more accurate evaluation of an investment's profitability.

How does IRR differ from MIRR?

IRR (Internal Rate of Return) calculates the discount rate that makes the net present value (NPV) of cash flows zero, assuming reinvestment at the IRR itself. MIRR (Modified Internal Rate of Return) adjusts for more realistic reinvestment by assuming cash flows are reinvested at the firm's cost of capital or a specified reinvestment rate, providing a more accurate measure of project profitability.

What are the limitations of IRR?

IRR limitations include multiple IRRs for nonconventional cash flows, difficulty comparing projects of different durations or scales, assumption of reinvestment at the IRR rate, and ignoring external factors like market conditions.

Why use MIRR instead of IRR?

Use MIRR instead of IRR because MIRR accounts for cost of capital and reinvestment rate, providing a more accurate measure of a project's profitability and true return on investment.

How are IRR and MIRR calculated?

IRR is calculated by finding the discount rate that makes the net present value (NPV) of cash flows equal to zero. MIRR is calculated by assuming reinvestment at the project's cost of capital, using the formula: MIRR = (Terminal Value of Positive Cash Flows / Present Value of Negative Cash Flows)^(1/n) - 1, where n is the number of periods.

Which is more reliable for investment decisions: IRR or MIRR?

MIRR is more reliable for investment decisions because it incorporates cost of capital and reinvestment rate, providing a more accurate reflection of project profitability than IRR.