Contango occurs when futures prices are higher than the spot price, often reflecting storage costs or expectations of rising prices. Backwardation is the opposite, where futures prices are lower than the spot price, indicating supply shortages or high demand in the present. Explore the dynamics of Contango vs Backwardation to enhance your futures trading strategies.

Main Difference

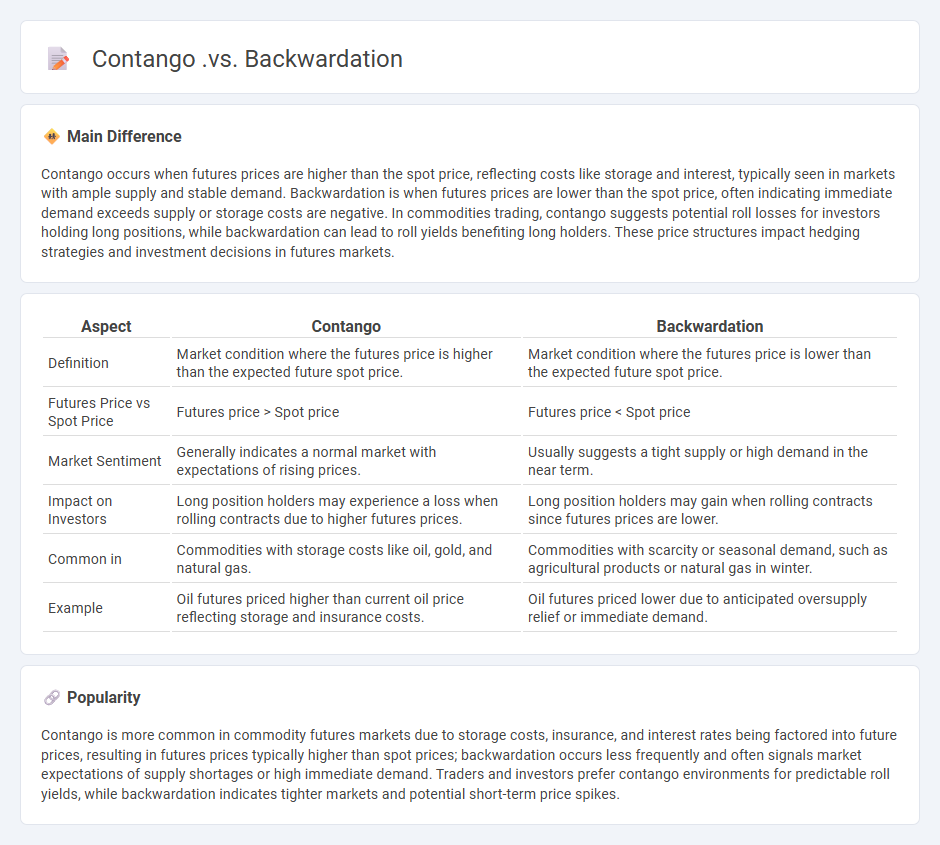

Contango occurs when futures prices are higher than the spot price, reflecting costs like storage and interest, typically seen in markets with ample supply and stable demand. Backwardation is when futures prices are lower than the spot price, often indicating immediate demand exceeds supply or storage costs are negative. In commodities trading, contango suggests potential roll losses for investors holding long positions, while backwardation can lead to roll yields benefiting long holders. These price structures impact hedging strategies and investment decisions in futures markets.

Connection

Contango and backwardation describe futures market conditions where asset prices differ from expected future spot prices. In contango, futures prices are higher than the anticipated spot price, often signaling storage costs or convenience yields exceeding expected price appreciation. Backwardation occurs when futures prices are lower than the expected spot price, indicating scarcity or high demand for immediate delivery relative to the future.

Comparison Table

| Aspect | Contango | Backwardation |

|---|---|---|

| Definition | Market condition where the futures price is higher than the expected future spot price. | Market condition where the futures price is lower than the expected future spot price. |

| Futures Price vs Spot Price | Futures price > Spot price | Futures price < Spot price |

| Market Sentiment | Generally indicates a normal market with expectations of rising prices. | Usually suggests a tight supply or high demand in the near term. |

| Impact on Investors | Long position holders may experience a loss when rolling contracts due to higher futures prices. | Long position holders may gain when rolling contracts since futures prices are lower. |

| Common in | Commodities with storage costs like oil, gold, and natural gas. | Commodities with scarcity or seasonal demand, such as agricultural products or natural gas in winter. |

| Example | Oil futures priced higher than current oil price reflecting storage and insurance costs. | Oil futures priced lower due to anticipated oversupply relief or immediate demand. |

Futures Curve

The futures curve illustrates the relationship between futures contract prices and their expiration dates, reflecting market expectations for asset prices over time. It often displays contango or backwardation, indicating whether future prices are higher or lower than spot prices, respectively. Traders and investors use the futures curve to identify arbitrage opportunities, hedge risk, and predict commodity or financial asset price trends. Key markets displaying futures curves include commodities like crude oil, gold, and financial instruments such as interest rate futures.

Spot Price

Spot price in finance refers to the current market price at which a particular asset, such as commodities, securities, or currencies, can be bought or sold for immediate delivery and settlement. It reflects real-time supply and demand conditions and serves as a benchmark for futures contracts and derivative pricing. For example, the spot price of gold fluctuates based on global economic indicators, geopolitical events, and currency strength, impacting investment strategies. Traders and investors closely monitor spot prices to make informed decisions about short-term market movements and hedging opportunities.

Carrying Costs

Carrying costs in finance represent the total expenses incurred to hold an investment or inventory over a specific period, including storage fees, insurance, depreciation, and opportunity costs. For stocks and commodities, carrying costs influence pricing models such as the cost-of-carry model, which impacts futures contracts valuation. Businesses managing inventory calculate carrying costs to optimize stock levels, balancing capital tied up against demand fulfillment. Accurate estimation of carrying costs is essential for effective financial planning and profit margin maximization.

Roll Yield

Roll yield in finance refers to the return generated from rolling futures contracts forward over time, capturing the difference between expiring and new contract prices. It is a critical component of total return in commodity and futures investing, influenced by the shape of the futures curve, whether in contango or backwardation. Positive roll yield occurs in backwardation when near-term contracts trade above longer-term contracts, while negative roll yield arises in contango markets where futures prices rise with maturity. Investors and funds tracking commodity indices closely monitor roll yield to assess performance impacts and strategize contract roll timing.

Market Expectations

Market expectations reflect investor forecasts about economic indicators, corporate earnings, and interest rates, shaping asset prices and trading strategies in finance. These expectations influence market volatility, liquidity, and capital allocation by anticipating future monetary policies set by bodies like the Federal Reserve. Analysts use forward-looking metrics such as yield curves, implied volatility from options, and consensus earnings estimates to gauge investor sentiment. Accurate market expectations enhance portfolio management and risk assessment by aligning investment decisions with probable economic outcomes.

Source and External Links

Contango vs Backwardation - Differences in the Futures Market - This article explains contango as an upward sloping curve where futures prices are higher than spot prices, and backwardation as a downward sloping curve where futures prices are lower than spot prices.

Differences Between Contango and Normal Backwardation in Commodity Futures - This blog explores the differences between contango and backwardation, highlighting that contango occurs when futures prices are higher than expected future spot prices, while backwardation occurs when futures prices are lower.

Contango vs. Backwardation in Futures Markets | Britannica Money - This article discusses contango and backwardation, noting that contango features higher long-term futures prices, while backwardation features higher spot and near-term futures prices compared to deferred contracts.

FAQs

What is contango in commodity markets?

Contango in commodity markets occurs when the futures price of a commodity is higher than the expected spot price at contract maturity.

What is backwardation in futures trading?

Backwardation in futures trading occurs when the futures price of a commodity is lower than its current spot price, indicating a market expectation of falling prices.

How does contango affect investors?

Contango increases costs for investors by forcing them to buy higher-priced futures contracts as prices rise over time, reducing potential profits in commodity trading.

How does backwardation benefit traders?

Backwardation benefits traders by allowing them to buy commodities at lower spot prices and sell futures contracts at higher prices, enabling potential profits from price convergence as contracts approach expiration.

What causes a market to be in contango or backwardation?

Contango occurs when future prices of a commodity or asset are higher than the spot price due to carrying costs like storage, insurance, and interest rates; backwardation occurs when future prices are lower than the spot price, often because of high demand for immediate delivery or supply shortages.

How do contango and backwardation impact futures prices?

Contango causes futures prices to be higher than the spot price due to carrying costs, while backwardation results in futures prices below the spot price, reflecting supply shortages or expected price declines.

Why do contango and backwardation matter in risk management?

Contango and backwardation affect risk management by influencing futures contract pricing, hedging effectiveness, and margin requirements, directly impacting trading costs and profit strategies.