Value at Risk (VaR) estimates the maximum potential loss over a specified time period at a given confidence level, widely used in financial risk management. Conditional Value at Risk (CVaR), also known as Expected Shortfall, provides the average loss exceeding the VaR threshold, capturing tail risk more effectively. Explore further to understand how these metrics enhance portfolio risk assessment and decision-making.

Main Difference

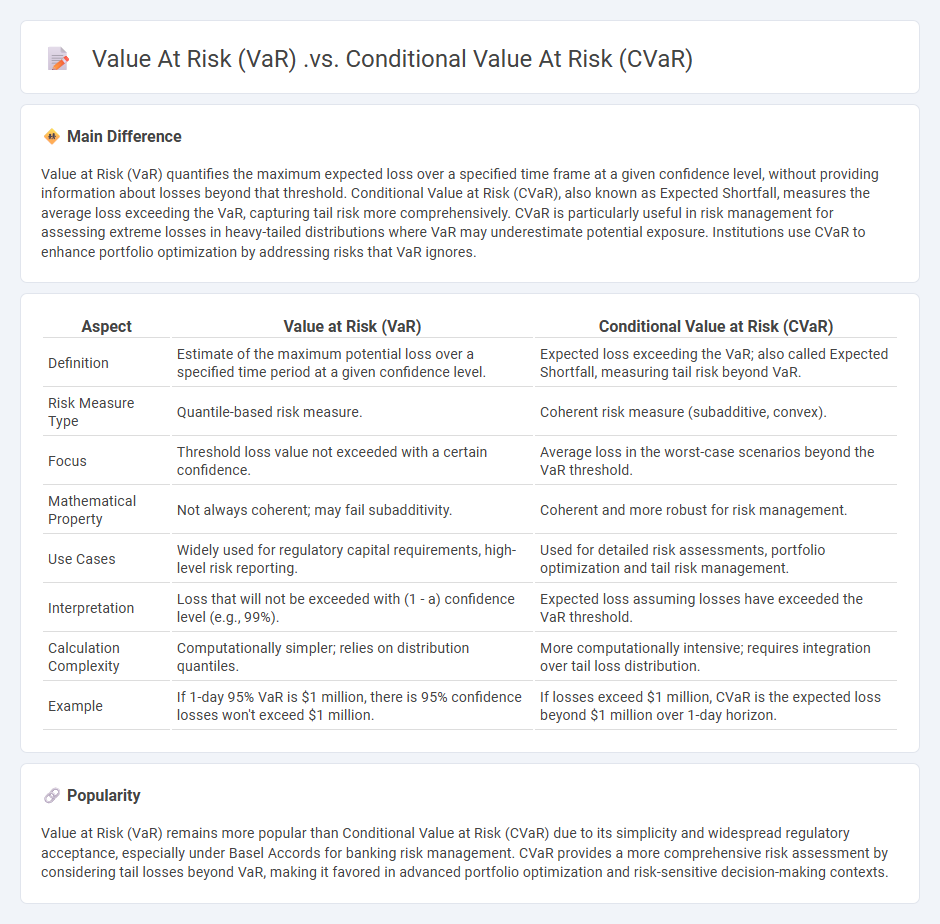

Value at Risk (VaR) quantifies the maximum expected loss over a specified time frame at a given confidence level, without providing information about losses beyond that threshold. Conditional Value at Risk (CVaR), also known as Expected Shortfall, measures the average loss exceeding the VaR, capturing tail risk more comprehensively. CVaR is particularly useful in risk management for assessing extreme losses in heavy-tailed distributions where VaR may underestimate potential exposure. Institutions use CVaR to enhance portfolio optimization by addressing risks that VaR ignores.

Connection

Value at Risk (VaR) quantifies the maximum expected loss over a specified time horizon at a given confidence level, while Conditional Value at Risk (CVaR) measures the average loss exceeding the VaR threshold, providing a deeper assessment of tail risk. CVaR offers a coherent risk measure by capturing the severity of losses beyond the VaR cutoff, making it more sensitive to extreme market events. Both metrics are integral to risk management frameworks, with CVaR enhancing portfolio optimization and regulatory capital calculations by addressing VaR's limitations in tail risk sensitivity.

Comparison Table

| Aspect | Value at Risk (VaR) | Conditional Value at Risk (CVaR) |

|---|---|---|

| Definition | Estimate of the maximum potential loss over a specified time period at a given confidence level. | Expected loss exceeding the VaR; also called Expected Shortfall, measuring tail risk beyond VaR. |

| Risk Measure Type | Quantile-based risk measure. | Coherent risk measure (subadditive, convex). |

| Focus | Threshold loss value not exceeded with a certain confidence. | Average loss in the worst-case scenarios beyond the VaR threshold. |

| Mathematical Property | Not always coherent; may fail subadditivity. | Coherent and more robust for risk management. |

| Use Cases | Widely used for regulatory capital requirements, high-level risk reporting. | Used for detailed risk assessments, portfolio optimization and tail risk management. |

| Interpretation | Loss that will not be exceeded with (1 - a) confidence level (e.g., 99%). | Expected loss assuming losses have exceeded the VaR threshold. |

| Calculation Complexity | Computationally simpler; relies on distribution quantiles. | More computationally intensive; requires integration over tail loss distribution. |

| Example | If 1-day 95% VaR is $1 million, there is 95% confidence losses won't exceed $1 million. | If losses exceed $1 million, CVaR is the expected loss beyond $1 million over 1-day horizon. |

Risk Measurement

Risk measurement in finance involves quantifying the potential losses an investment or portfolio might experience due to market fluctuations, credit defaults, or operational failures. Common metrics include Value at Risk (VaR), Expected Shortfall (ES), and standard deviation, which help assess the likelihood and magnitude of adverse financial outcomes. Advanced models utilize historical data and statistical techniques to forecast volatility and correlations, enabling more accurate risk assessment. Accurate risk measurement is essential for regulatory compliance, capital allocation, and strategic decision-making in financial institutions.

Tail Risk

Tail risk refers to the probability of asset returns moving beyond three standard deviations from the mean, often resulting in extreme financial losses. It is a critical concept in risk management, particularly for portfolios with exposure to rare but severe market events. Financial models like Value at Risk (VaR) frequently underestimate tail risk due to their reliance on normal distribution assumptions, making stress testing and scenario analysis essential. Institutions often use options, diversification, and capital reserves to mitigate the impact of tail risk on investment portfolios.

Confidence Level

Confidence level in finance represents the probability that a statistical estimate or model, such as Value at Risk (VaR) or portfolio return, falls within a specified range. Common confidence levels include 90%, 95%, and 99%, which indicate the degree of certainty investors or analysts have in forecasting financial outcomes. This metric is critical in risk management, as it helps quantify the potential losses and inform decision-making under uncertainty. Financial institutions use confidence levels to set capital reserves and comply with regulatory requirements such as those outlined in Basel III.

Loss Distribution

Loss distribution in finance quantifies the probability and magnitude of potential financial losses within a portfolio or asset class, enabling effective risk management and capital allocation. Statistical models such as the normal, lognormal, and Pareto distributions are commonly applied to estimate loss probabilities and severities. Advanced risk measures like Value at Risk (VaR) and Expected Shortfall (ES) rely on accurate loss distribution modeling to assess potential adverse outcomes under different market conditions. Regulatory frameworks such as Basel III emphasize the importance of loss distribution analysis for maintaining financial stability and solvency.

Portfolio Optimization

Portfolio optimization involves selecting the best mix of assets to maximize returns while minimizing risk, based on modern portfolio theory introduced by Harry Markowitz. Techniques commonly used include mean-variance optimization, which evaluates expected returns against portfolio variance, and the Capital Asset Pricing Model (CAPM) for determining the appropriate required return of an asset. Advanced methods integrate constraints such as transaction costs, liquidity requirements, and regulatory limits to enhance practical applicability. Quantitative tools like Monte Carlo simulations and quadratic programming are essential for solving complex portfolio optimization problems in contemporary financial markets.

Source and External Links

Value at risk - Wikipedia - VaR estimates the maximum potential loss over a given time and probability, while CVaR measures the average loss beyond the VaR threshold, capturing tail risk more comprehensively.

CVaR vs: VaR: Which Risk Measure Should You Use - FasterCapital - VaR reflects the quantile-based maximum loss at a confidence level, whereas CVaR, also called Expected Shortfall, represents the expected loss in the worst-case percentile beyond VaR.

Value at Risk and Conditional Value at Risk: - Deborah Kidd, CFA - CVaR is subadditive and accounts for tail risk by averaging expected losses beyond VaR, making it a more robust risk measure than VaR, which only indicates a threshold loss value.

FAQs

What is Value at Risk?

Value at Risk (VaR) quantifies the maximum potential loss of a portfolio over a specified time frame at a given confidence level, commonly used in financial risk management.

What is Conditional Value at Risk?

Conditional Value at Risk (CVaR) is a risk assessment measure that quantifies the expected loss exceeding the Value at Risk (VaR) at a specified confidence level, providing insight into tail risk in financial portfolios.

How does VaR differ from CVaR?

VaR (Value at Risk) measures the maximum potential loss at a specific confidence level, while CVaR (Conditional Value at Risk) calculates the expected loss exceeding the VaR threshold, providing a more comprehensive risk assessment of tail losses.

What are the advantages of CVaR over VaR?

CVaR provides a more comprehensive risk assessment by measuring expected losses beyond the VaR threshold, offers coherence as a risk measure ensuring subadditivity and convexity, captures tail risk better, and supports more effective portfolio optimization compared to VaR.

How is VaR calculated?

Value at Risk (VaR) is calculated by determining the maximum potential loss over a specified time period at a given confidence level using historical simulation, variance-covariance method, or Monte Carlo simulation.

How is CVaR calculated?

CVaR (Conditional Value at Risk) is calculated as the expected loss exceeding the Value at Risk (VaR) at a specified confidence level, mathematically defined as the average of the tail losses beyond the VaR threshold.

Why use CVaR instead of VaR?

CVaR provides a more accurate measure of tail risk by capturing the average loss beyond the VaR threshold, enhancing risk assessment in extreme market conditions.