Systematic risk refers to the inherent market-wide uncertainties affecting all investments, driven by factors like economic shifts, geopolitical events, and interest rate changes, impacting entire portfolios. Unsystematic risk, also known as specific risk, arises from individual company or industry factors such as management decisions, competitive pressures, or operational failures, and can be mitigated through diversification. Explore the distinctions and management strategies of these risks to enhance investment decision-making.

Main Difference

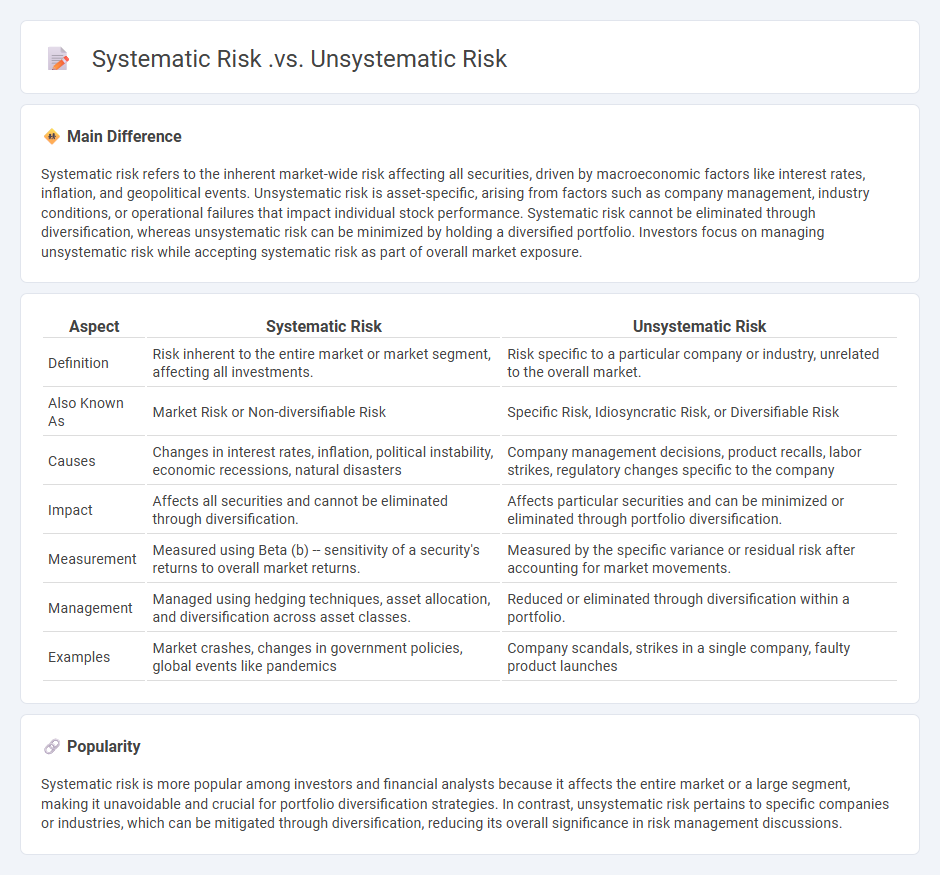

Systematic risk refers to the inherent market-wide risk affecting all securities, driven by macroeconomic factors like interest rates, inflation, and geopolitical events. Unsystematic risk is asset-specific, arising from factors such as company management, industry conditions, or operational failures that impact individual stock performance. Systematic risk cannot be eliminated through diversification, whereas unsystematic risk can be minimized by holding a diversified portfolio. Investors focus on managing unsystematic risk while accepting systematic risk as part of overall market exposure.

Connection

Systematic risk affects the entire market or a broad segment of the market and cannot be eliminated through diversification, while unsystematic risk is specific to a single company or industry and can be reduced through portfolio diversification. Both types of risks are components of total risk, influencing investment decisions and asset pricing models like the Capital Asset Pricing Model (CAPM). Understanding the interplay between systematic and unsystematic risk is crucial for optimizing portfolio risk management and achieving desired returns.

Comparison Table

| Aspect | Systematic Risk | Unsystematic Risk |

|---|---|---|

| Definition | Risk inherent to the entire market or market segment, affecting all investments. | Risk specific to a particular company or industry, unrelated to the overall market. |

| Also Known As | Market Risk or Non-diversifiable Risk | Specific Risk, Idiosyncratic Risk, or Diversifiable Risk |

| Causes | Changes in interest rates, inflation, political instability, economic recessions, natural disasters | Company management decisions, product recalls, labor strikes, regulatory changes specific to the company |

| Impact | Affects all securities and cannot be eliminated through diversification. | Affects particular securities and can be minimized or eliminated through portfolio diversification. |

| Measurement | Measured using Beta (b) -- sensitivity of a security's returns to overall market returns. | Measured by the specific variance or residual risk after accounting for market movements. |

| Management | Managed using hedging techniques, asset allocation, and diversification across asset classes. | Reduced or eliminated through diversification within a portfolio. |

| Examples | Market crashes, changes in government policies, global events like pandemics | Company scandals, strikes in a single company, faulty product launches |

Diversification

Diversification in finance involves spreading investments across various asset classes, industries, and geographical regions to reduce risk and improve portfolio stability. Research from Morningstar shows diversified portfolios historically experience lower volatility and higher risk-adjusted returns compared to concentrated holdings. Financial advisors recommend combining equities, bonds, real estate, and alternative assets to optimize diversification benefits. According to Vanguard, a well-diversified portfolio can protect against market downturns and help achieve long-term financial goals.

Market Risk

Market risk refers to the possibility of an investor experiencing losses due to factors that affect the overall performance of financial markets. It includes risks such as equity price risk, interest rate risk, currency risk, and commodity price risk. Quantitative models like Value at Risk (VaR) and stress testing are commonly used to measure and manage market risk exposure. Institutions such as banks, hedge funds, and asset managers continuously monitor market risk to protect portfolios from volatility and systemic shocks.

Asset-Specific Risk

Asset-specific risk refers to the potential variability in an asset's returns caused by factors unique to that asset, such as management decisions, product recalls, or regulatory changes affecting a particular company. This type of risk contrasts with systematic risk, which impacts all assets in the market due to macroeconomic conditions like inflation or interest rates. Diversification within a portfolio reduces asset-specific risk by spreading exposure across multiple, uncorrelated securities. Financial models such as the Capital Asset Pricing Model (CAPM) primarily account for systematic risk, as asset-specific risk can be mitigated through diversification.

Portfolio Management

Portfolio management involves the strategic allocation and oversight of investments across various asset classes to optimize returns while managing risk. Techniques include asset diversification, risk assessment, and performance monitoring based on financial metrics such as the Sharpe ratio and alpha. Professional portfolio managers utilize modern portfolio theory (MPT) and algorithmic trading tools to balance expected returns against volatility for clients ranging from individual investors to institutional funds. Effective portfolio management drives wealth growth by aligning investment strategies with the client's financial goals and market conditions.

Risk Mitigation

Risk mitigation in finance involves identifying, assessing, and prioritizing potential financial risks to minimize their impact on investment portfolios or business operations. Techniques include diversification, hedging with derivatives, insurance policies, and implementing robust internal controls to prevent fraud and operational failures. Regulatory compliance with bodies such as the SEC or Basel III standards further strengthens risk management frameworks. Effective risk mitigation enhances financial stability and supports sustainable growth in volatile markets.

Source and External Links

Systematic Risk vs. Unsystematic Risk - SmartAsset - Systematic risk affects the entire market and is uncontrollable, driven by macro factors like inflation or interest rates, while unsystematic risk affects specific companies or industries and can be controlled or minimized by those entities.

Systematic vs. Unsystematic Risk: Differences and Similarities - Indeed - Systematic risk impacts the whole market resulting from broad economic changes and is mitigated by asset allocation or hedging, whereas unsystematic risk affects individual securities and can be reduced through portfolio diversification.

Systematic Risk and Unsystematic Risk - Key Differences - Bajaj Finserv - Systematic risk, also called market risk, is external and unavoidable affecting all investments simultaneously, while unsystematic risk is internal to specific companies or sectors and can be mitigated or avoided by diversification and strategic investment decisions.

FAQs

What is risk in finance?

Risk in finance is the potential for financial loss or the variability of returns on an investment.

What is systematic risk?

Systematic risk is the inherent risk affecting the entire market or a broad segment, caused by factors like economic recessions, interest rate changes, or geopolitical events that cannot be eliminated through diversification.

What is unsystematic risk?

Unsystematic risk is the risk specific to a company or industry, such as management decisions or product recalls, that can be minimized through diversification.

How do systematic and unsystematic risks differ?

Systematic risk affects the entire market or a broad range of assets due to macroeconomic factors like inflation or interest rates, while unsystematic risk is specific to a single company or industry, such as management decisions or product recalls.

What are examples of systematic risk?

Examples of systematic risk include economic recessions, interest rate changes, inflation, political instability, and natural disasters.

What are examples of unsystematic risk?

Examples of unsystematic risk include company bankruptcy, management fraud, product recalls, labor strikes, and regulatory fines.

How can investors manage systematic and unsystematic risks?

Investors manage systematic risk through asset diversification, hedging with derivatives, and using asset allocation strategies; they mitigate unsystematic risk by diversifying portfolios across different industries, sectors, and geographic regions to reduce company-specific exposure.