Capital rationing involves setting a fixed limit on investment funds, restricting project selection to maximize returns within budget constraints. Soft capital rationing arises from internal company policies or temporary limitations rather than external funding shortages, affecting project prioritization flexibility. Explore further to understand how these approaches impact strategic investment decisions and financial management.

Main Difference

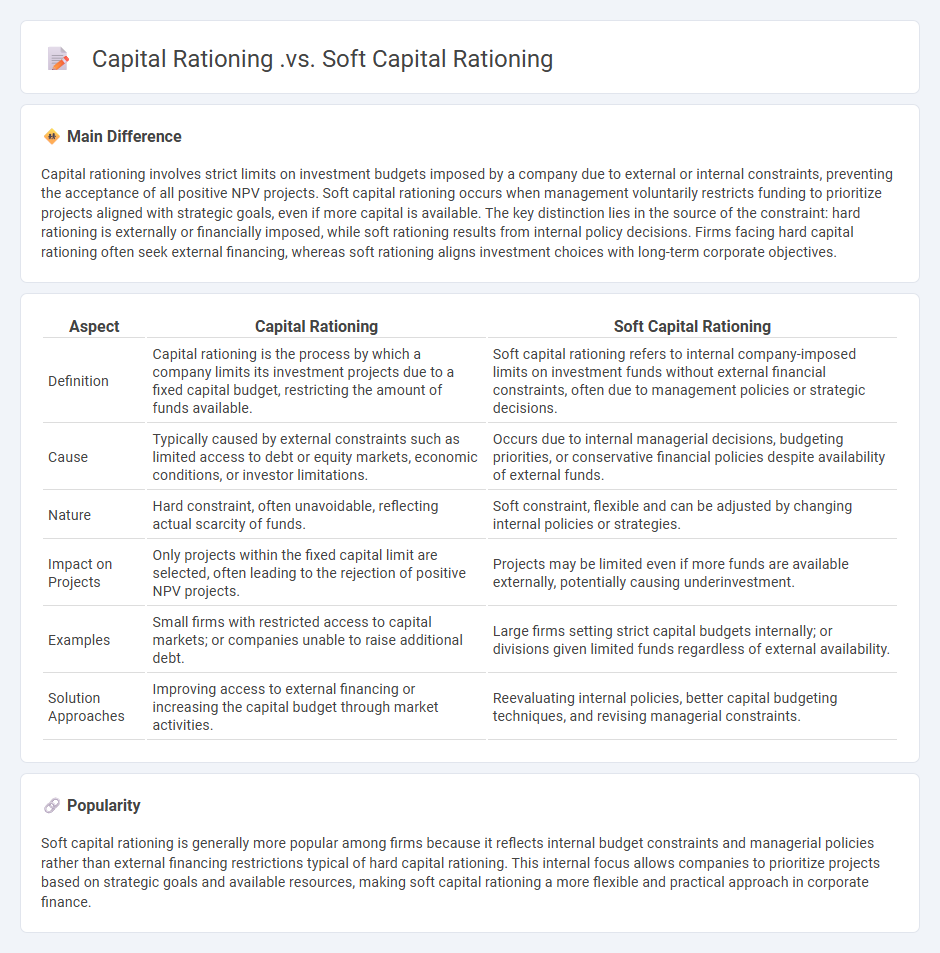

Capital rationing involves strict limits on investment budgets imposed by a company due to external or internal constraints, preventing the acceptance of all positive NPV projects. Soft capital rationing occurs when management voluntarily restricts funding to prioritize projects aligned with strategic goals, even if more capital is available. The key distinction lies in the source of the constraint: hard rationing is externally or financially imposed, while soft rationing results from internal policy decisions. Firms facing hard capital rationing often seek external financing, whereas soft rationing aligns investment choices with long-term corporate objectives.

Connection

Capital rationing involves limiting investment projects due to budget constraints, while soft capital rationing arises internally from management policies rather than external financing limits. Both concepts restrict available capital for projects, influencing how firms prioritize and allocate resources to maximize returns. Understanding the link helps in strategic financial planning and optimizing investment decisions under constrained budgets.

Comparison Table

| Aspect | Capital Rationing | Soft Capital Rationing |

|---|---|---|

| Definition | Capital rationing is the process by which a company limits its investment projects due to a fixed capital budget, restricting the amount of funds available. | Soft capital rationing refers to internal company-imposed limits on investment funds without external financial constraints, often due to management policies or strategic decisions. |

| Cause | Typically caused by external constraints such as limited access to debt or equity markets, economic conditions, or investor limitations. | Occurs due to internal managerial decisions, budgeting priorities, or conservative financial policies despite availability of external funds. |

| Nature | Hard constraint, often unavoidable, reflecting actual scarcity of funds. | Soft constraint, flexible and can be adjusted by changing internal policies or strategies. |

| Impact on Projects | Only projects within the fixed capital limit are selected, often leading to the rejection of positive NPV projects. | Projects may be limited even if more funds are available externally, potentially causing underinvestment. |

| Examples | Small firms with restricted access to capital markets; or companies unable to raise additional debt. | Large firms setting strict capital budgets internally; or divisions given limited funds regardless of external availability. |

| Solution Approaches | Improving access to external financing or increasing the capital budget through market activities. | Reevaluating internal policies, better capital budgeting techniques, and revising managerial constraints. |

Capital Constraints

Capital constraints limit a firm's ability to access sufficient funding for investments, operations, and growth, influencing strategic decision-making and financial planning. These constraints often arise from inadequate internal cash flows, restricted access to external credit markets, or stringent regulatory capital requirements. Research shows that capital constraints can lead to underinvestment, reduced innovation, and lower firm valuation, especially in small and medium-sized enterprises. Effective management of capital constraints involves balancing debt and equity, optimizing working capital, and leveraging alternative financing sources such as venture capital or asset-based lending.

Internal vs External Limitations

Internal limitations in finance refer to constraints within an organization, such as limited capital, inadequate management expertise, or restricted operational capacity. External limitations encompass factors outside the firm's control, including economic downturns, regulatory changes, market competition, and fluctuating interest rates. Both types of limitations significantly impact financial decision-making, budgeting, and investment strategies. Effectively identifying and managing these constraints is crucial for optimizing financial performance and ensuring sustainable growth.

Investment Opportunities

Investment opportunities in finance span various asset classes, including equities, bonds, real estate, and alternative investments such as private equity and hedge funds. Equities offer potential for capital appreciation and dividend income, while bonds provide fixed-income returns with varying risk profiles depending on issuer credit quality. Real estate investments encompass residential, commercial, and industrial properties, often delivering steady cash flow through rentals and long-term value growth. Alternative investments diversify portfolios by accessing non-traditional assets with distinct risk-return characteristics compared to public markets.

Capital Allocation

Capital allocation in finance involves distributing financial resources among various investment opportunities to maximize returns and minimize risk. It includes decisions on debt versus equity financing, budgeting for projects, and managing a company's capital structure. Effective capital allocation aligns with corporate strategy to enhance shareholder value and supports sustainable growth. Financial metrics such as Return on Invested Capital (ROIC) and Weighted Average Cost of Capital (WACC) guide these strategic decisions.

Funding Availability

Funding availability in finance determines a company's capacity to secure capital for operations, expansion, and investment. It depends on factors such as creditworthiness, market conditions, interest rates, and investor confidence. Access to diverse funding sources--including equity, debt, venture capital, and government grants--enhances an organization's financial stability. Firms with strong balance sheets and cash flow are positioned to attract more favorable financing terms and support sustainable growth.

Source and External Links

Here are the comparisons and descriptions for Capital Rationing and Soft Capital Rationing: 1.Capital Rationing - Capital rationing is a decision process used to select projects when funding is limited, encompassing both hard and soft rationing.

2.Soft Capital Rationing - Soft capital rationing involves a company's internal decision to limit investment spending despite having access to external funds, focusing on managing risk and strategic projects.

3.Capital Rationing vs. Soft Capital Rationing - While capital rationing is a broader strategy to limit projects due to funding constraints, soft capital rationing specifically involves voluntary internal restrictions for strategic or risk management purposes.

FAQs

What is capital rationing?

Capital rationing is the process of allocating limited investment funds among competing projects to maximize returns under budget constraints.

How does capital rationing differ from soft capital rationing?

Capital rationing limits investment due to external funding constraints, while soft capital rationing restricts investment based on internal policies or management decisions.

What are the causes of soft capital rationing?

Soft capital rationing is caused by internal policies limiting investment budgets, risk aversion by management, desire to maintain financial flexibility, and the pursuit of optimal capital structure.

What are the effects of soft capital rationing on investment decisions?

Soft capital rationing leads firms to prioritize projects with the highest expected returns and manage internal funds carefully, often resulting in delayed or rejected positive NPV investments due to informal budget limits.

How does hard capital rationing compare to soft capital rationing?

Hard capital rationing strictly limits funding due to external constraints like market conditions or regulatory policies, while soft capital rationing arises from internal management decisions to limit investment despite available external funds.

What are examples of soft capital rationing in business?

Examples of soft capital rationing in business include internal budget limits set by management, prioritizing projects without external funding constraints, using discretionary spending caps, and informal limits on investment to maintain financial flexibility.

Why do companies implement capital rationing?

Companies implement capital rationing to prioritize and allocate limited financial resources efficiently among competing projects, ensuring maximum return on investment and optimal use of capital under budget constraints.