The Lucas Critique challenges traditional macroeconomic models by emphasizing the inconsistency of policy evaluation when agents adjust their expectations, undermining predictions based on fixed parameters. Rational Expectations Theory asserts that economic agents optimally use all available information to forecast future variables, making systematic policy interventions ineffective in altering real economic outcomes. Explore deeper insights into how these foundational concepts shape modern economic policy analysis.

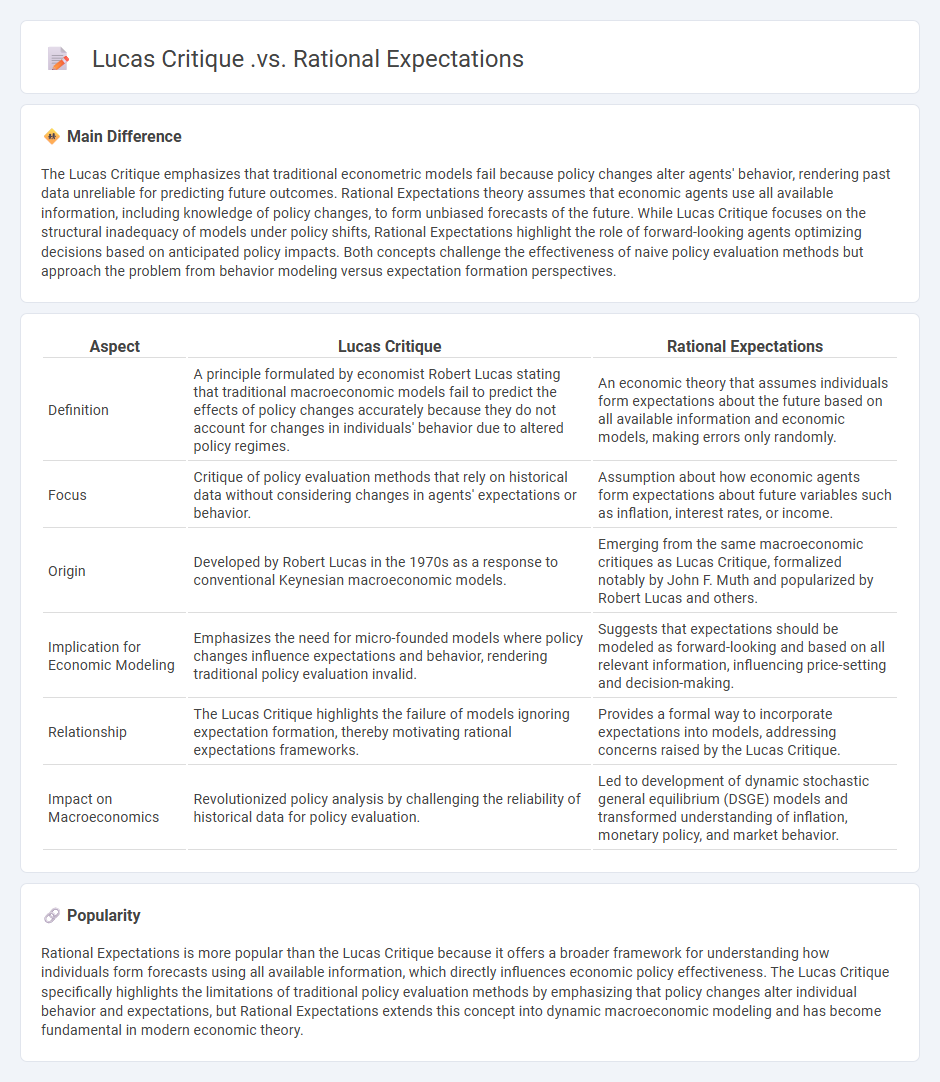

Main Difference

The Lucas Critique emphasizes that traditional econometric models fail because policy changes alter agents' behavior, rendering past data unreliable for predicting future outcomes. Rational Expectations theory assumes that economic agents use all available information, including knowledge of policy changes, to form unbiased forecasts of the future. While Lucas Critique focuses on the structural inadequacy of models under policy shifts, Rational Expectations highlight the role of forward-looking agents optimizing decisions based on anticipated policy impacts. Both concepts challenge the effectiveness of naive policy evaluation methods but approach the problem from behavior modeling versus expectation formation perspectives.

Connection

The Lucas Critique highlights the failure of traditional econometric models to account for changes in policy affecting agents' expectations, emphasizing that economic agents form expectations based on anticipated policy regimes. Rational Expectations theory assumes individuals use all available information to forecast future economic variables accurately, aligning expectations with model-consistent outcomes. Together, they emphasize the need for macroeconomic models to incorporate forward-looking behavior and expectations that adapt to policy changes to improve predictive accuracy.

Comparison Table

| Aspect | Lucas Critique | Rational Expectations |

|---|---|---|

| Definition | A principle formulated by economist Robert Lucas stating that traditional macroeconomic models fail to predict the effects of policy changes accurately because they do not account for changes in individuals' behavior due to altered policy regimes. | An economic theory that assumes individuals form expectations about the future based on all available information and economic models, making errors only randomly. |

| Focus | Critique of policy evaluation methods that rely on historical data without considering changes in agents' expectations or behavior. | Assumption about how economic agents form expectations about future variables such as inflation, interest rates, or income. |

| Origin | Developed by Robert Lucas in the 1970s as a response to conventional Keynesian macroeconomic models. | Emerging from the same macroeconomic critiques as Lucas Critique, formalized notably by John F. Muth and popularized by Robert Lucas and others. |

| Implication for Economic Modeling | Emphasizes the need for micro-founded models where policy changes influence expectations and behavior, rendering traditional policy evaluation invalid. | Suggests that expectations should be modeled as forward-looking and based on all relevant information, influencing price-setting and decision-making. |

| Relationship | The Lucas Critique highlights the failure of models ignoring expectation formation, thereby motivating rational expectations frameworks. | Provides a formal way to incorporate expectations into models, addressing concerns raised by the Lucas Critique. |

| Impact on Macroeconomics | Revolutionized policy analysis by challenging the reliability of historical data for policy evaluation. | Led to development of dynamic stochastic general equilibrium (DSGE) models and transformed understanding of inflation, monetary policy, and market behavior. |

Policy Invariance

Policy invariance in economics refers to the principle that economic models or relationships should remain consistent under different policy regimes or interventions. This concept is crucial for ensuring that estimated parameters or behavioral responses are stable and reliable when policies change. Economists use policy invariance to validate structural models, enabling accurate forecasting and effective policy analysis. Empirical studies often test policy invariance by comparing data before and after policy shifts, such as tax reforms or monetary policy adjustments.

Structural Parameters

Structural parameters in economics refer to fundamental coefficients within economic models that capture inherent relationships and behaviors in an economy, such as the elasticity of substitution between inputs or the degree of risk aversion among consumers. These parameters remain constant across different environments, reflecting underlying economic structures rather than transient market conditions or policy changes. Accurate estimation of structural parameters facilitates robust policy analysis, enabling economists to predict the effects of shocks or interventions with greater confidence. For example, calibrating a general equilibrium model requires precise values for parameters like the labor supply elasticity or capital depreciation rate to simulate realistic economic dynamics.

Adaptive Expectations

Adaptive expectations theory in economics explains how individuals form forecasts of future economic variables based on past data, adjusting their beliefs incrementally as new information becomes available. This model contrasts with rational expectations by assuming agents update predictions primarily through observed errors rather than incorporating all available information instantly. Adaptive expectations widely apply in inflation forecasting, where past inflation rates heavily influence future expectations, impacting wage setting and price dynamics. Empirical evidence from the Phillips Curve studies highlights adaptive expectations' role in explaining persistent inflation and unemployment trade-offs.

Microfoundations

Microfoundations in economics examine the individual behaviors and decisions that underpin aggregate economic phenomena. This approach links macroeconomic models to microeconomic principles such as utility maximization, profit optimization, and rational expectations. Prominent frameworks include the Dynamic Stochastic General Equilibrium (DSGE) models, which incorporate individual agents' optimization problems in explaining fluctuations in output, consumption, and investment. Key contributors to the development of microfoundations theory include economists like Robert Lucas and Thomas Sargent, whose work emphasized the importance of micro-level decision-making in macroeconomic analysis.

Model Consistency

Model consistency in economics ensures that theoretical models align with empirical data and established economic principles, enhancing predictive accuracy and policy relevance. It involves validating assumptions, parameters, and functional forms to reflect real-world behaviors and market dynamics accurately. Achieving consistency reduces contradictions within models, supporting reliable analysis of economic phenomena such as inflation, unemployment, and growth. Consistent models are crucial for guiding decision-making by institutions like the Federal Reserve and the International Monetary Fund.

Source and External Links

Lucas Critique: Definition & Example | Vaia - The Lucas Critique is based on Rational Expectations and argues that traditional Keynesian models fail because they do not account for changes in people's expectations when policies change; Rational Expectations theory posits people use all available information to forecast economic variables, and Lucas Critique highlights that policy changes alter economic relationships by changing expectations, making past data unreliable for predictions.

Robert E. Lucas - Robert Lucas introduced the Lucas Critique showing that econometric models fail to predict effects of policy changes because people's expectations, formed rationally using all information, adjust in response to policy, thus invalidating previous empirical relationships and emphasizing that credible government policies can quickly change inflation expectations with minimal unemployment impact.

Rational expectation and the Lucas critique - Lucas used rational expectations to develop an alternative explanation to the Phillips curve, arguing that prior estimates of trade-offs between inflation and unemployment were unreliable because they were based on adaptive expectations, with rational expectations implying that only unexpected inflation affects output, highlighting the crucial role of information and expectations in economic policy effectiveness.

FAQs

What is the Lucas Critique in economics?

The Lucas Critique in economics argues that traditional policy evaluation models fail because they do not account for changes in agents' expectations and behavior when policies change, emphasizing the need for models based on microfoundations and rational expectations.

What are rational expectations in macroeconomics?

Rational expectations in macroeconomics refer to the hypothesis that individuals and firms use all available information efficiently and accurately to forecast future economic variables, resulting in predictions that, on average, are correct and unbiased.

How does the Lucas Critique challenge traditional economic models?

The Lucas Critique challenges traditional economic models by arguing that they fail to account for changes in policy altering agents' expectations and behavior, rendering model parameters unstable and predictions unreliable.

How do rational expectations alter economic forecasting?

Rational expectations improve economic forecasting by incorporating all available information and anticipated policy effects, reducing systematic errors and making predictions more consistent with actual economic outcomes.

What is the main difference between Lucas Critique and rational expectations?

The main difference is that the Lucas Critique emphasizes that policy evaluations must account for changes in agents' behavior due to altered policy rules, while rational expectations refer to agents forming forecasts based on all available information and consistent economic models.

Why is the Lucas Critique important for policy evaluation?

The Lucas Critique is important for policy evaluation because it highlights that traditional economic models fail to account for changes in agent behavior when policies change, leading to inaccurate predictions and ineffective policy prescriptions.

How do both concepts influence modern macroeconomic theory?

Expectations and market imperfections fundamentally shape modern macroeconomic theory by influencing policy effectiveness, wage-price dynamics, and the formation of economic cycles.