Say's Law asserts that supply creates its own demand, emphasizing production as the driver of economic growth. Keynes' Law challenges this, highlighting that demand drives supply and that insufficient aggregate demand leads to unemployment and economic downturns. Explore the fundamental differences between these economic principles and their impact on fiscal policy.

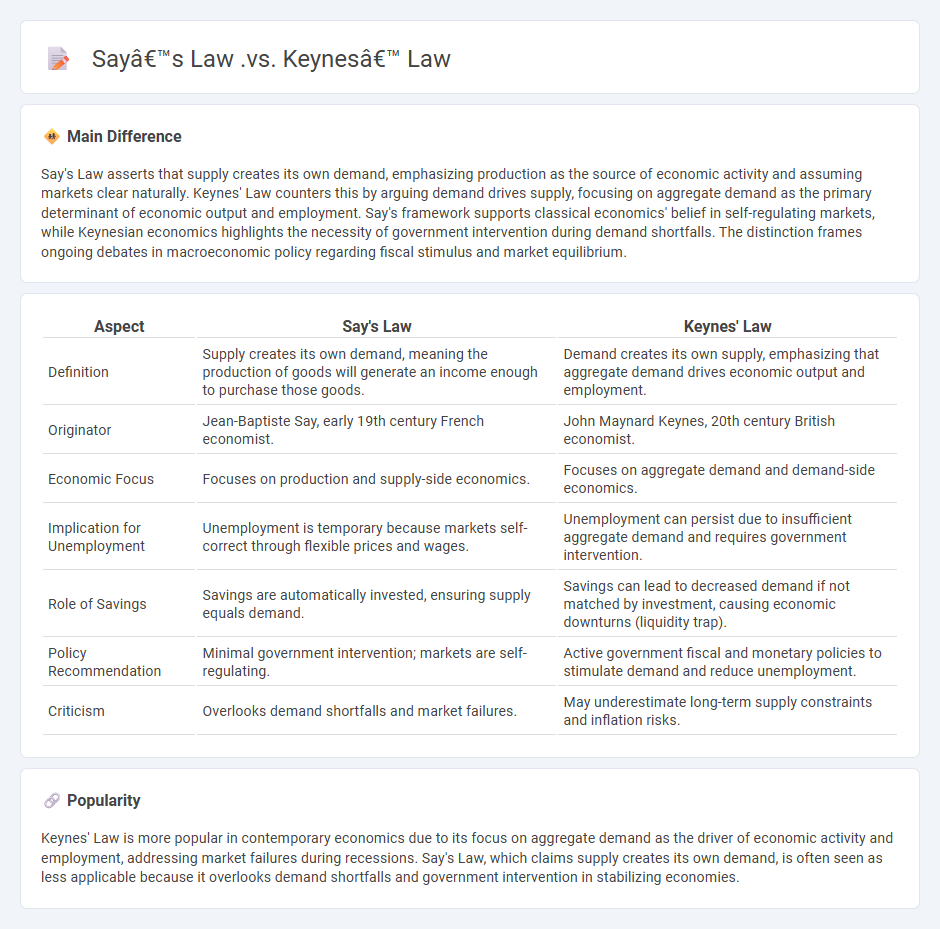

Main Difference

Say's Law asserts that supply creates its own demand, emphasizing production as the source of economic activity and assuming markets clear naturally. Keynes' Law counters this by arguing demand drives supply, focusing on aggregate demand as the primary determinant of economic output and employment. Say's framework supports classical economics' belief in self-regulating markets, while Keynesian economics highlights the necessity of government intervention during demand shortfalls. The distinction frames ongoing debates in macroeconomic policy regarding fiscal stimulus and market equilibrium.

Connection

Say's Law asserts that supply creates its own demand, emphasizing production as the driver of economic equilibrium. Keynes' Law counters this by highlighting demand as the primary force influencing output and employment, especially during downturns. The connection lies in their contrasting views on the role of supply and demand in achieving economic balance.

Comparison Table

| Aspect | Say's Law | Keynes' Law |

|---|---|---|

| Definition | Supply creates its own demand, meaning the production of goods will generate an income enough to purchase those goods. | Demand creates its own supply, emphasizing that aggregate demand drives economic output and employment. |

| Originator | Jean-Baptiste Say, early 19th century French economist. | John Maynard Keynes, 20th century British economist. |

| Economic Focus | Focuses on production and supply-side economics. | Focuses on aggregate demand and demand-side economics. |

| Implication for Unemployment | Unemployment is temporary because markets self-correct through flexible prices and wages. | Unemployment can persist due to insufficient aggregate demand and requires government intervention. |

| Role of Savings | Savings are automatically invested, ensuring supply equals demand. | Savings can lead to decreased demand if not matched by investment, causing economic downturns (liquidity trap). |

| Policy Recommendation | Minimal government intervention; markets are self-regulating. | Active government fiscal and monetary policies to stimulate demand and reduce unemployment. |

| Criticism | Overlooks demand shortfalls and market failures. | May underestimate long-term supply constraints and inflation risks. |

Aggregate Supply vs Aggregate Demand

Aggregate Supply (AS) represents the total quantity of goods and services producers are willing to supply at different price levels within an economy. Aggregate Demand (AD) signifies the total quantity of goods and services consumers, businesses, government, and foreign buyers are willing to purchase at varying price levels. The interaction between AS and AD determines the overall price level and real GDP, influencing economic equilibrium, inflation, and unemployment rates. Shifts in either curve due to factors like changes in consumer confidence or input costs can result in macroeconomic fluctuations.

Production Creates Its Own Demand

The concept "Production Creates Its Own Demand," known as Say's Law, posits that the act of producing goods and services generates an equivalent demand in the economy. This principle suggests that supply inherently generates sufficient purchasing power to absorb the output, preventing general gluts. Critics argue that this theory overlooks short-term demand fluctuations and the role of money in affecting consumption patterns. Major economists such as Jean-Baptiste Say and later classical economists endorse this view to explain economic equilibrium in markets.

Demand-Driven Output

Demand-driven output reflects the total production level determined by consumer demand and market conditions rather than supply constraints. Economic models such as Keynesian theory emphasize that aggregate demand drives output and employment in the short run, especially during recessions. Businesses adjust production plans based on shifts in consumer spending, investment, government expenditures, and net exports. Understanding demand-driven output helps policymakers design effective fiscal and monetary interventions to stabilize economic growth.

Economic Recessions

Economic recessions represent significant declines in economic activity across the economy, typically identified by two consecutive quarters of negative GDP growth. During recessions, unemployment rates surge as businesses reduce production and cut jobs, leading to decreased consumer spending and lower industrial output. Central banks often respond by lowering interest rates and implementing quantitative easing to stimulate demand and stabilize financial markets. Historical data indicate that severe recessions, such as the 2008 global financial crisis, can cause prolonged economic downturns and require extensive fiscal and monetary interventions.

Market Equilibrium

Market equilibrium occurs when the quantity of goods supplied equals the quantity demanded at a specific price point, resulting in a stable market condition. This balance minimizes shortages and surpluses, ensuring efficient allocation of resources in competitive markets. Prices adjust through supply and demand interactions, reflecting consumer preferences and production costs. The equilibrium price and quantity are fundamental concepts in microeconomic theory, crucial for predicting market behavior and informing policy decisions.

Source and External Links

Say's Law - This economic principle posits that supply creates its own demand, emphasizing the role of production and supply in the economy.

Keynes' Law - This principle focuses on aggregate demand and suggests that economic growth is driven by demand, particularly in situations of economic slack.

Say's Law vs Keynes' Law - These two laws represent contrasting views on the drivers of economic activity, with Say's Law emphasizing supply and Keynes' Law focusing on demand.

FAQs

What is Say’s Law?

Say's Law states that supply creates its own demand, meaning production of goods and services generates enough income to purchase all outputs.

What is Keynes’ Law?

Keynes' Law states that aggregate demand determines overall economic output and employment levels, asserting that demand creates its own supply.

How does Say’s Law explain economic output?

Say's Law explains economic output by asserting that supply creates its own demand, meaning total production in an economy inherently generates enough income to purchase all goods produced, ensuring full utilization of resources and balancing output.

How does Keynes’ Law address demand and employment?

Keynes' Law states that aggregate demand directly determines employment levels, asserting that insufficient demand leads to unemployment because firms produce only what is demanded.

What are the major differences between Say’s Law and Keynes’ Law?

Say's Law states that supply creates its own demand, emphasizing production as the driver of economic equilibrium. Keynes' Law asserts that demand creates its own supply, highlighting aggregate demand as the key factor in determining output and employment levels. Say's Law assumes flexible prices and markets clear naturally, while Keynes' Law argues for government intervention to address demand shortfalls and prevent unemployment.

Which economic situations favor Say’s Law over Keynes’ Law?

Say's Law is favored in economic situations characterized by flexible prices and wages, full employment, and supply-driven growth, where markets clear without persistent demand shortfalls.

How do Say’s Law and Keynes’ Law influence modern economic policy?

Say's Law, emphasizing supply creates its own demand, guides policies promoting production and market self-regulation; Keynes' Law, highlighting demand-driven economic activity, supports fiscal stimulus and active government intervention during downturns.