Moral hazard occurs when one party takes on risk because they do not bear the full consequences, often seen in insurance contexts where policyholders may engage in riskier behavior after coverage. Adverse selection arises when asymmetric information leads to the selection of higher-risk individuals by insurers, causing market inefficiencies due to hidden risk profiles. Explore further to understand their impact on insurance markets and risk management strategies.

Main Difference

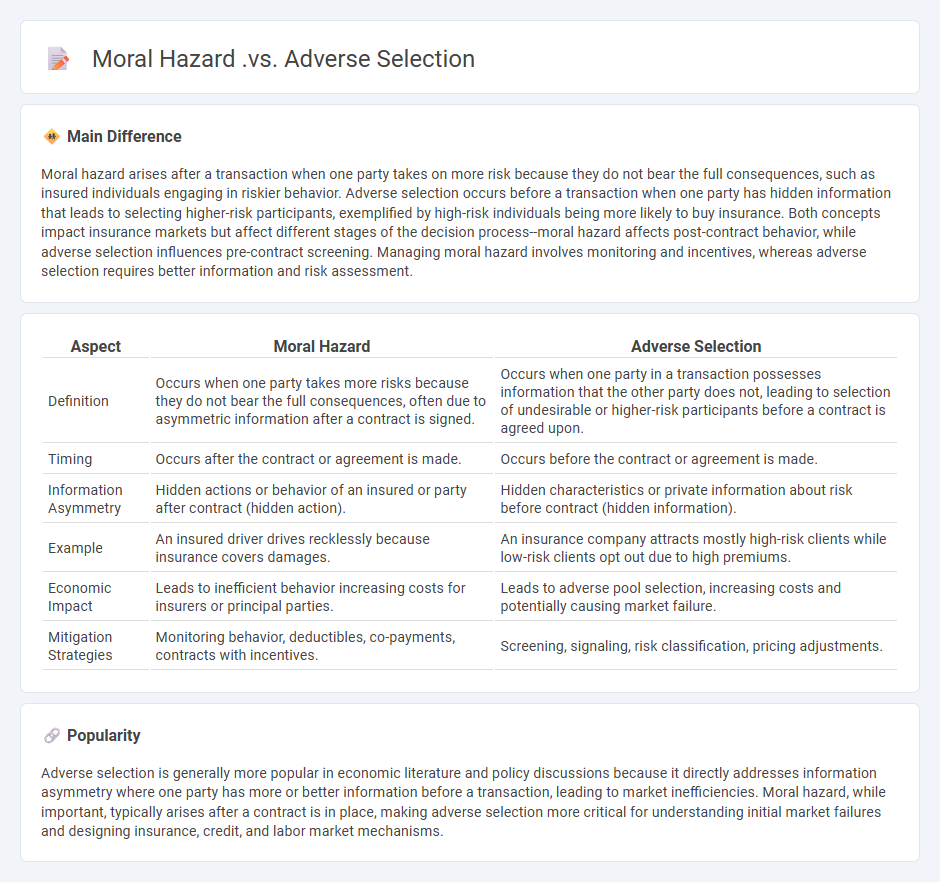

Moral hazard arises after a transaction when one party takes on more risk because they do not bear the full consequences, such as insured individuals engaging in riskier behavior. Adverse selection occurs before a transaction when one party has hidden information that leads to selecting higher-risk participants, exemplified by high-risk individuals being more likely to buy insurance. Both concepts impact insurance markets but affect different stages of the decision process--moral hazard affects post-contract behavior, while adverse selection influences pre-contract screening. Managing moral hazard involves monitoring and incentives, whereas adverse selection requires better information and risk assessment.

Connection

Moral hazard and adverse selection are interconnected concepts in economics and insurance markets, both arising from asymmetric information between parties. Adverse selection occurs when one party has more information about risks before a transaction, leading to high-risk individuals being more likely to participate, while moral hazard emerges after the transaction due to changes in behavior when risks are partially transferred. Understanding their link helps insurers design better contracts to mitigate risks and improve market efficiency.

Comparison Table

| Aspect | Moral Hazard | Adverse Selection |

|---|---|---|

| Definition | Occurs when one party takes more risks because they do not bear the full consequences, often due to asymmetric information after a contract is signed. | Occurs when one party in a transaction possesses information that the other party does not, leading to selection of undesirable or higher-risk participants before a contract is agreed upon. |

| Timing | Occurs after the contract or agreement is made. | Occurs before the contract or agreement is made. |

| Information Asymmetry | Hidden actions or behavior of an insured or party after contract (hidden action). | Hidden characteristics or private information about risk before contract (hidden information). |

| Example | An insured driver drives recklessly because insurance covers damages. | An insurance company attracts mostly high-risk clients while low-risk clients opt out due to high premiums. |

| Economic Impact | Leads to inefficient behavior increasing costs for insurers or principal parties. | Leads to adverse pool selection, increasing costs and potentially causing market failure. |

| Mitigation Strategies | Monitoring behavior, deductibles, co-payments, contracts with incentives. | Screening, signaling, risk classification, pricing adjustments. |

Asymmetric Information

Asymmetric information occurs when one party in an economic transaction possesses more or better information than the other, affecting market outcomes and efficiency. This phenomenon is prevalent in markets such as insurance, where buyers often know more about their risk levels than sellers, leading to adverse selection. It also plays a critical role in credit markets, where lenders face challenges due to borrowers' private information about their ability to repay loans. Addressing asymmetric information often requires mechanisms like signaling, screening, or regulatory intervention to improve transparency and reduce market failures.

Incentive Problem

The incentive problem in economics arises when individuals or organizations lack motivation to act in the best interest of others, often due to misaligned rewards and consequences. Principal-agent problems exemplify this issue, where agents may pursue personal goals over principals' objectives, leading to inefficiencies. Information asymmetry intensifies incentive problems by preventing proper monitoring and contract enforcement. Effective mechanisms like performance-based contracts and regulatory oversight aim to mitigate these challenges by aligning incentives and reducing moral hazard.

Risk Behavior

Risk behavior in economics refers to the decision-making processes individuals and firms use when confronted with uncertainty and potential losses or gains. It is analyzed through models such as expected utility theory, prospect theory, and behavioral economics, which account for varying risk preferences and attitudes. Empirical evidence shows that risk-averse agents prioritize stable returns, while risk-seeking behavior often emerges in contexts with high potential rewards or in speculative markets. Understanding risk behavior helps economists predict market reactions, portfolio choices, insurance uptake, and economic policy responses.

Screening

Screening in economics refers to strategies used by one party to gather information about another party's characteristics or behavior, reducing information asymmetry in markets. Employers use screening techniques such as interviews and tests to identify the most qualified job candidates, while lenders analyze credit scores to assess borrower risk. In insurance markets, screening mechanisms help distinguish between high-risk and low-risk clients, affecting premium pricing and coverage terms. Efficient screening improves market outcomes by aligning incentives and mitigating adverse selection problems.

Hidden Action

Hidden action in economics refers to situations where one party in a transaction cannot fully observe the actions of another, leading to asymmetric information problems. This concept is central in principal-agent theory, where the agent may take unobservable actions that affect outcomes but are not verifiable by the principal. Common examples include moral hazard in insurance markets or effort levels in employment contracts. Addressing hidden action often involves designing incentive-compatible contracts to align interests between parties.

Source and External Links

Money and Banking: Adverse Selection and Moral Hazard - Adverse selection occurs *before* insurance is purchased, involving bad risks more likely to buy insurance due to asymmetric information, while moral hazard occurs *afterwards*, when insured individuals take more risks because they do not bear full costs of their actions.

Adverse Selection vs. Moral Hazard | Overview & Difference - Lesson - Adverse selection refers to a decision made with incomplete information leading to poor outcomes, whereas moral hazard describes risky behavior by an insured person protected from the consequences because another party bears the cost; both arise from asymmetric information.

Moral Hazard and Adverse Selection in Health Insurance | NBER - Moral hazard leads insured individuals to consume more medical care since they pay less out-of-pocket, while adverse selection involves sicker individuals choosing more generous plans, posing challenges in insurance design due to asymmetric information.

FAQs

What is moral hazard?

Moral hazard is the risk that a party insulated from risk behaves differently than if they fully bore the consequences, typically leading to careless or risky actions.

What is adverse selection?

Adverse selection is a market condition where buyers or sellers have asymmetric information, causing high-risk individuals to be more likely to participate than low-risk ones.

How do moral hazard and adverse selection differ?

Moral hazard occurs when one party takes more risks because they do not bear the full consequences, while adverse selection arises when one party has hidden information before a transaction, leading to the selection of higher-risk participants.

What causes moral hazard in insurance?

Moral hazard in insurance is caused by insured individuals engaging in riskier behavior or neglecting preventive measures because they do not bear the full cost of their actions.

What leads to adverse selection in markets?

Adverse selection in markets occurs due to asymmetric information where sellers have more knowledge about product quality than buyers, causing high-risk or low-quality products to dominate.

How can moral hazard be reduced?

Moral hazard can be reduced by implementing risk-sharing mechanisms, increasing transparency, enforcing strict monitoring and reporting requirements, and aligning incentives through deductibles or copayments.

How can adverse selection be prevented?

Adverse selection can be prevented by implementing thorough information screening, using signaling mechanisms, enforcing mandatory disclosure, and designing contracts that align incentives between parties.