Temporary equilibrium describes a market state where supply and demand balance at a specific point in time without accounting for future adjustments or expectations. General equilibrium extends this concept by analyzing how multiple markets simultaneously reach balance, incorporating interdependencies and dynamic feedback across the entire economy. Explore the distinctions between these equilibrium concepts to understand their implications in economic modeling and forecasting.

Main Difference

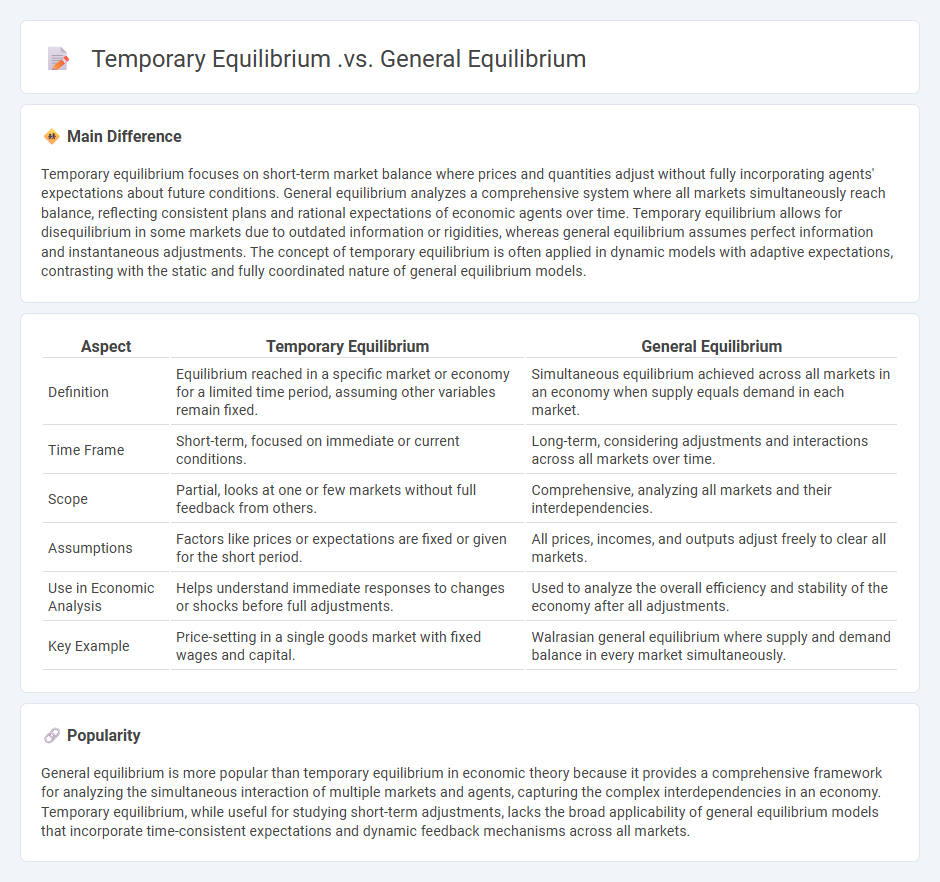

Temporary equilibrium focuses on short-term market balance where prices and quantities adjust without fully incorporating agents' expectations about future conditions. General equilibrium analyzes a comprehensive system where all markets simultaneously reach balance, reflecting consistent plans and rational expectations of economic agents over time. Temporary equilibrium allows for disequilibrium in some markets due to outdated information or rigidities, whereas general equilibrium assumes perfect information and instantaneous adjustments. The concept of temporary equilibrium is often applied in dynamic models with adaptive expectations, contrasting with the static and fully coordinated nature of general equilibrium models.

Connection

Temporary equilibrium represents a short-term state where prices and quantities adjust within a fixed structure of expectations and constraints, while general equilibrium describes a comprehensive, long-term balance across all markets simultaneously. The transition from temporary to general equilibrium occurs as agents continuously update expectations and reallocate resources, ultimately achieving consistency between supply, demand, and prices in every market. This dynamic process links temporary equilibria as successive steps converging toward the stable, overall general equilibrium in an economy.

Comparison Table

| Aspect | Temporary Equilibrium | General Equilibrium |

|---|---|---|

| Definition | Equilibrium reached in a specific market or economy for a limited time period, assuming other variables remain fixed. | Simultaneous equilibrium achieved across all markets in an economy when supply equals demand in each market. |

| Time Frame | Short-term, focused on immediate or current conditions. | Long-term, considering adjustments and interactions across all markets over time. |

| Scope | Partial, looks at one or few markets without full feedback from others. | Comprehensive, analyzing all markets and their interdependencies. |

| Assumptions | Factors like prices or expectations are fixed or given for the short period. | All prices, incomes, and outputs adjust freely to clear all markets. |

| Use in Economic Analysis | Helps understand immediate responses to changes or shocks before full adjustments. | Used to analyze the overall efficiency and stability of the economy after all adjustments. |

| Key Example | Price-setting in a single goods market with fixed wages and capital. | Walrasian general equilibrium where supply and demand balance in every market simultaneously. |

Adjustment Period

The adjustment period in economics refers to the time interval during which an economy or market adapts to new policies, shocks, or structural changes. Economic variables such as prices, wages, and output gradually move towards a new equilibrium, influenced by factors like sticky prices, wage contracts, and information asymmetries. Empirical studies show that adjustment periods can vary significantly across sectors, with labor markets often experiencing longer durations due to frictions in employment contracts and skill matching. Central banks and policymakers monitor adjustment dynamics closely to optimize interventions and minimize transitional unemployment or inflation volatility.

Market Clearing

Market clearing occurs when the quantity of goods supplied equals the quantity demanded at a specific price, resulting in no surplus or shortage. This equilibrium price ensures efficient allocation of resources in a competitive market. Market clearing is fundamental to neoclassical economics and is often modeled using supply and demand curves intersecting at equilibrium. Real-world applications include commodity markets, labor markets, and financial markets where prices adjust to balance supply and demand.

Static vs Dynamic Analysis

Static analysis in economics evaluates the immediate effects of policy changes or market shifts by examining equilibrium conditions without considering time or adjustment processes. Dynamic analysis incorporates time-based changes, forecasting how variables evolve due to capital accumulation, technological progress, or consumer behavior over multiple periods. Models like the Ramsey-Cass-Koopmans framework illustrate dynamic optimization where intertemporal choices impact economic growth trajectories. Empirical studies often combine both approaches to balance short-term policy impacts with long-term economic development insights.

Exogenous vs Endogenous Variables

Exogenous variables in economics are factors determined outside the economic model and remain unaffected by the system's internal dynamics, such as government policy decisions or technological innovations. Endogenous variables are those whose values are explained within the model, like GDP, inflation rates, or employment levels, responding to changes in exogenous inputs. The distinction allows economists to isolate causes and effects, improving the accuracy of economic predictions and policy simulations. Understanding these variable types is crucial for constructing models like the IS-LM framework or Dynamic Stochastic General Equilibrium (DSGE) models.

Long-run vs Short-run Equilibrium

Long-run equilibrium in economics occurs when all input factors, including capital and labor, are variable, allowing firms to adjust production fully and earn normal profits without economic profit or loss. Short-run equilibrium, by contrast, happens when at least one factor of production is fixed, and firms may earn supernormal profits or losses due to temporary imbalances between supply and demand. In perfectly competitive markets, short-run equilibrium can involve economic profits or losses, but long-run forces drive the market toward zero economic profit as firms enter or exit the industry. The distinction between these equilibria affects firm behavior, market supply adjustments, and resource allocation efficiency.

Source and External Links

Temporary Equilibrium Definition & Examples - Quickonomics - Temporary equilibrium describes a short-term balance between supply and demand, influenced by transient factors like seasonal trends or sudden shocks, and is inherently unstable as it does not account for long-term interactions across all markets.

General equilibrium theory - Wikipedia - General equilibrium refers to a stable, economy-wide state where all markets and sectors reach simultaneous balance, with prices and production levels interconnected across the entire economic system over the long term.

Intertemporal equilibrium - Wikipedia - Intertemporal equilibrium extends the idea of general equilibrium over multiple time periods, assuming agents plan consumption and investment decisions based on expectations and opportunities across their entire lifetimes, not just current conditions.

FAQs

What is temporary equilibrium in economics?

Temporary equilibrium in economics refers to a situation where supply and demand balance at given prices and quantities, holding other economic variables constant, before all future adjustments occur.

What is general equilibrium in economics?

General equilibrium in economics is a state where supply and demand balance simultaneously across all markets in an economy, ensuring optimal resource allocation and price consistency.

How does temporary equilibrium differ from general equilibrium?

Temporary equilibrium focuses on short-term market balance with fixed expectations and prices, while general equilibrium examines the simultaneous balance across all markets considering adjustments in prices and expectations over time.

What assumptions underlie temporary equilibrium?

Temporary equilibrium assumes agents optimize based on current information and prices, expectations remain fixed during the period, and markets clear without immediate adjustments to shocks.

What are the key features of general equilibrium?

General equilibrium features include simultaneous determination of prices and quantities in all markets, interdependence of economic agents, market clearing conditions, price flexibility, and allocation efficiency across goods and factors.

How do markets reach general equilibrium?

Markets reach general equilibrium through the interaction of supply and demand where prices adjust so that all goods and services are simultaneously cleared, ensuring no excess supply or demand across all markets.

Why is general equilibrium important for economic analysis?

General equilibrium is important for economic analysis because it provides a comprehensive framework to assess how supply and demand balance across multiple interconnected markets simultaneously, capturing the interdependencies and feedback effects within an entire economy.