The Monty Hall Problem and the St. Petersburg Paradox both illustrate key challenges in behavioral finance modeling by highlighting how individuals process risk and uncertainty differently from classical economic assumptions. The Monty Hall Problem demonstrates the impact of information asymmetry and probabilistic reasoning errors, while the St. Petersburg Paradox exposes inconsistencies in expected utility theory due to infinite expected payoff scenarios. Explore how these paradoxes deepen our understanding of decision-making biases and risk assessment in financial behavior.

Main Difference

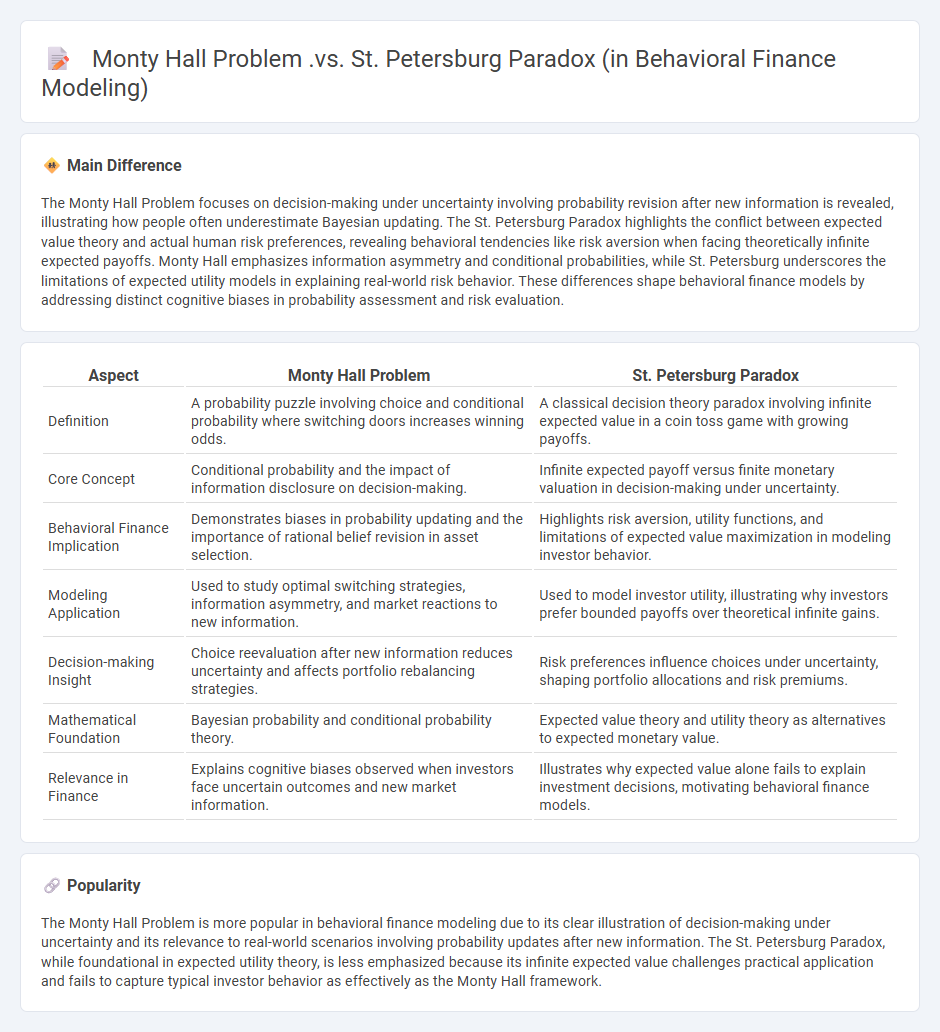

The Monty Hall Problem focuses on decision-making under uncertainty involving probability revision after new information is revealed, illustrating how people often underestimate Bayesian updating. The St. Petersburg Paradox highlights the conflict between expected value theory and actual human risk preferences, revealing behavioral tendencies like risk aversion when facing theoretically infinite expected payoffs. Monty Hall emphasizes information asymmetry and conditional probabilities, while St. Petersburg underscores the limitations of expected utility models in explaining real-world risk behavior. These differences shape behavioral finance models by addressing distinct cognitive biases in probability assessment and risk evaluation.

Connection

The Monty Hall Problem and the St. Petersburg Paradox both highlight challenges in decision-making under uncertainty, illustrating how human behavior deviates from classical expected utility theory. In behavioral finance modeling, these problems underscore the importance of psychological biases and risk perception, such as overweighing unlikely outcomes in the Monty Hall scenario and infinite expected values in the St. Petersburg Paradox. This connection informs models that integrate prospect theory, helping explain investor behavior that departs from rational maximization principles.

Comparison Table

| Aspect | Monty Hall Problem | St. Petersburg Paradox |

|---|---|---|

| Definition | A probability puzzle involving choice and conditional probability where switching doors increases winning odds. | A classical decision theory paradox involving infinite expected value in a coin toss game with growing payoffs. |

| Core Concept | Conditional probability and the impact of information disclosure on decision-making. | Infinite expected payoff versus finite monetary valuation in decision-making under uncertainty. |

| Behavioral Finance Implication | Demonstrates biases in probability updating and the importance of rational belief revision in asset selection. | Highlights risk aversion, utility functions, and limitations of expected value maximization in modeling investor behavior. |

| Modeling Application | Used to study optimal switching strategies, information asymmetry, and market reactions to new information. | Used to model investor utility, illustrating why investors prefer bounded payoffs over theoretical infinite gains. |

| Decision-making Insight | Choice reevaluation after new information reduces uncertainty and affects portfolio rebalancing strategies. | Risk preferences influence choices under uncertainty, shaping portfolio allocations and risk premiums. |

| Mathematical Foundation | Bayesian probability and conditional probability theory. | Expected value theory and utility theory as alternatives to expected monetary value. |

| Relevance in Finance | Explains cognitive biases observed when investors face uncertain outcomes and new market information. | Illustrates why expected value alone fails to explain investment decisions, motivating behavioral finance models. |

Probability Paradox

The Probability Paradox in finance highlights how investors often misinterpret low-probability, high-impact events, leading to flawed risk assessments and suboptimal portfolio choices. This paradox is evident in market behavior during financial crises, where rare events like the 2008 collapse expose the limitations of models assuming normal distributions. Financial models such as Value at Risk (VaR) frequently underestimate tail risks due to the paradox, contributing to systemic vulnerabilities. Recognizing this paradox is crucial for developing robust risk management strategies that incorporate fat-tailed distributions and scenario analyses.

Expected Value

Expected value in finance represents the weighted average of all possible returns from an investment, calculated by multiplying each potential outcome by its probability and summing the results. It serves as a critical metric for assessing risk and making informed investment decisions by quantifying the anticipated return. Portfolio managers and analysts use expected value to evaluate stocks, bonds, and other assets to optimize risk-reward profiles. This concept underpins essential financial theories, including modern portfolio theory and capital asset pricing model (CAPM).

Decision-Making Bias

Decision-making bias in finance significantly impacts investment choices and risk assessment, often leading to suboptimal portfolio performance. Common biases such as overconfidence, anchoring, and loss aversion skew traders' and investors' perception of market data and financial forecasts. Behavioral finance studies quantify that biases can reduce average investment returns by several percentage points annually compared to rational models. Understanding these cognitive distortions allows for improved financial strategies and risk management frameworks in both individual and institutional contexts.

Risk Perception

Risk perception in finance significantly influences investor behavior and market dynamics by shaping how individuals assess potential losses and gains under uncertainty. Empirical studies reveal that cognitive biases such as overconfidence, herd behavior, and loss aversion distort accurate risk evaluation, leading to suboptimal decision-making. Advanced quantitative models incorporating behavioral insights improve portfolio management by adjusting risk assessments for psychological factors. Financial institutions increasingly integrate risk perception metrics to enhance risk management strategies and regulatory compliance.

Rational Choice Theory

Rational Choice Theory in finance explains how investors make decisions by maximizing expected utility based on available information and risk preferences. It assumes individuals act rationally to optimize financial outcomes, considering trade-offs between risk and return. This theory underpins models like the Capital Asset Pricing Model (CAPM) and Modern Portfolio Theory (MPT), which guide investment strategies and asset pricing. Empirical evidence frequently supports rational behavior in efficient markets, although behavioral finance highlights exceptions due to cognitive biases.

Source and External Links

Monty Hall problem - Wikipedia - The Monty Hall problem is a counterintuitive probability puzzle showing that switching choices after additional information improves winning chances, illustrating behavioral biases in decision-making under uncertainty, unlike the St. Petersburg paradox which involves infinite expected value dilemmas in gamble valuations.

Expected utility hypothesis - Wikipedia - The St. Petersburg paradox reveals limitations of expected value in behavioral finance, demonstrating how people reject infinite expected payoff gambles due to risk aversion and utility considerations, contrasting with Monty Hall where update of beliefs leads to better expected outcomes.

The St. Petersburg Paradox (Simple Example + Explanation) - The St. Petersburg paradox is explained through ergodicity economics as a temporal wealth accumulation problem rather than a traditional expected value one; this contrasts with the Monty Hall problem which involves probability updating, both highlighting different behavioral finance modeling issues in decision theory.

FAQs

What is the Monty Hall Problem?

The Monty Hall Problem is a probability puzzle where a contestant chooses one of three doors, behind one door is a prize, and after the host reveals a non-winning door among the remaining two, switching the initial choice doubles the chance of winning from 1/3 to 2/3.

What is the St. Petersburg Paradox?

The St. Petersburg Paradox is a decision theory problem illustrating a conflict between expected value calculated from an infinite expected monetary payoff and people's actual willingness to pay a finite amount to play a lottery with exponentially increasing rewards.

How does each problem illustrate probability in behavioral finance?

Each problem illustrates probability in behavioral finance by demonstrating how individuals assess risks, estimate likelihoods, and make decisions under uncertainty, often revealing biases like overconfidence, availability heuristic, or anchoring that affect rational probability evaluation.

What psychological biases appear in the Monty Hall Problem?

The Monty Hall Problem reveals confirmation bias, availability heuristic, and the gambler's fallacy as key psychological biases affecting decision-making.

How does risk perception differ between the two paradoxes?

Risk perception in the Ellsberg Paradox involves ambiguity aversion, where individuals prefer known probabilities over unknown ones. In the St. Petersburg Paradox, risk perception is challenged by the infinite expected value, causing difficulty in assigning finite utility to large but improbable gains.

What can these problems teach us about irrational decision-making?

These problems reveal cognitive biases and emotional influences that lead to deviations from rational choices, highlighting how heuristics, risk misperception, and framing effects contribute to irrational decision-making.

How are these paradoxes applied in behavioral finance modeling?

Paradoxes like the Ellsberg and Allais paradoxes are applied in behavioral finance modeling to explain deviations from expected utility theory by incorporating ambiguity aversion and inconsistent risk preferences into models of investor behavior.