Accruals and deferrals are fundamental accounting concepts that impact financial reporting by recognizing revenues and expenses in the appropriate periods. Accruals record income and expenses when they are earned or incurred, while deferrals postpone recognition until cash transactions occur. Explore the detailed differences between accruals and deferrals to enhance your understanding of accurate financial statements.

Main Difference

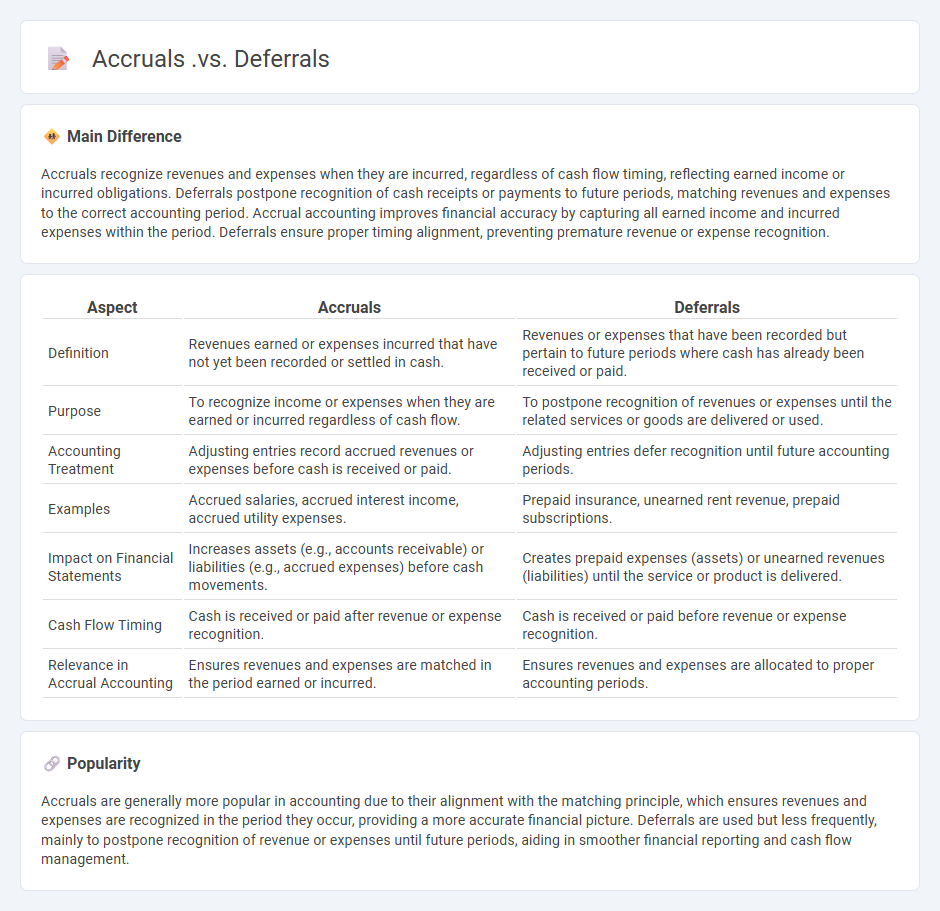

Accruals recognize revenues and expenses when they are incurred, regardless of cash flow timing, reflecting earned income or incurred obligations. Deferrals postpone recognition of cash receipts or payments to future periods, matching revenues and expenses to the correct accounting period. Accrual accounting improves financial accuracy by capturing all earned income and incurred expenses within the period. Deferrals ensure proper timing alignment, preventing premature revenue or expense recognition.

Connection

Accruals and deferrals are connected by their role in adjusting financial statements to reflect the true financial position within a specific accounting period. Accruals recognize revenues and expenses when they are earned or incurred, regardless of cash flow, while deferrals postpone recognition until the cash transaction occurs. Both concepts ensure compliance with the matching principle and improve the accuracy of financial reporting.

Comparison Table

| Aspect | Accruals | Deferrals |

|---|---|---|

| Definition | Revenues earned or expenses incurred that have not yet been recorded or settled in cash. | Revenues or expenses that have been recorded but pertain to future periods where cash has already been received or paid. |

| Purpose | To recognize income or expenses when they are earned or incurred regardless of cash flow. | To postpone recognition of revenues or expenses until the related services or goods are delivered or used. |

| Accounting Treatment | Adjusting entries record accrued revenues or expenses before cash is received or paid. | Adjusting entries defer recognition until future accounting periods. |

| Examples | Accrued salaries, accrued interest income, accrued utility expenses. | Prepaid insurance, unearned rent revenue, prepaid subscriptions. |

| Impact on Financial Statements | Increases assets (e.g., accounts receivable) or liabilities (e.g., accrued expenses) before cash movements. | Creates prepaid expenses (assets) or unearned revenues (liabilities) until the service or product is delivered. |

| Cash Flow Timing | Cash is received or paid after revenue or expense recognition. | Cash is received or paid before revenue or expense recognition. |

| Relevance in Accrual Accounting | Ensures revenues and expenses are matched in the period earned or incurred. | Ensures revenues and expenses are allocated to proper accounting periods. |

Revenue Recognition

Revenue recognition in finance refers to the accounting principle that determines the specific conditions under which revenue is recognized and recorded in financial statements. According to the Financial Accounting Standards Board (FASB) ASC 606, revenue is recognized when control of a promised good or service is transferred to the customer, reflecting the amount expected to be collected. This standard enhances comparability across industries by providing a consistent framework for revenue measurement and disclosure. Accurate revenue recognition is critical for investors and stakeholders assessing a company's financial health and performance.

Expense Matching

Expense matching is a fundamental accounting principle in finance that requires expenses to be recorded in the same accounting period as the revenues they help generate. This method provides a more accurate representation of a company's profitability by aligning costs with associated income, facilitating better financial analysis and decision-making. Common applications include matching cost of goods sold with sales revenue and recognizing depreciation expenses over the useful life of an asset. Compliance with generally accepted accounting principles (GAAP) ensures consistency and reliability in financial reporting.

Accrued Revenues

Accrued revenues represent earnings that have been recognized by a company for goods or services delivered but not yet invoiced or received as cash by the end of an accounting period. These revenues are recorded as assets on the balance sheet, typically under accounts receivable, reflecting amounts owed by customers. Accurate accrual accounting ensures financial statements adhere to the matching principle, aligning revenues with the period they are earned. Common examples include interest income earned but not yet received and consulting services performed but not yet billed.

Deferred Expenses

Deferred expenses represent costs paid in advance for goods or services to be received in future accounting periods, enhancing matching of expenses with revenues. Examples include prepaid insurance premiums and rent, recorded as current assets on the balance sheet until consumed. Proper recognition complies with accrual accounting principles and ensures accurate financial reporting. Tracking deferred expenses aids in cash flow management and financial forecasting for businesses.

Financial Statement Timing

Financial statement timing critically impacts the accuracy and relevance of financial reporting by determining the cut-off period for recording transactions and events. Precise timing ensures compliance with accounting standards like IFRS and GAAP, reflecting a company's true financial position at specific reporting dates. Timing discrepancies can lead to misstatements in revenue recognition or expense matching, affecting stakeholders' decision-making processes. Companies must implement strict internal controls and regular audits to maintain the integrity of financial statement timing.

Source and External Links

Differences Between Accrual vs. Deferral Accounting - This article outlines the key differences between accruals and deferrals in accounting, focusing on timing, expenses, payments, and revenue recognition.

Accrual vs. Deferral in Accounting-What's the Difference? - This resource explains the concepts of accrual and deferral in accounting, highlighting how they affect expenses and revenues differently based on payment timing.

Financial Accounting 101: Accruals and Deferrals - Made Easy - This video provides a simplified explanation of accruals and deferrals, using the mnemonic "Dollars before Action" for deferrals and "Action before Dollars" for accruals.

FAQs

What is the meaning of accruals in accounting?

Accruals in accounting refer to revenues earned or expenses incurred that are recorded before cash is exchanged, aligning income and expenses with the period they relate to.

What is the definition of deferrals?

Deferrals are accounting adjustments that postpone the recognition of revenues or expenses to a future period when the related goods or services are delivered or consumed.

How do accruals and deferrals differ in financial statements?

Accruals recognize revenues and expenses when earned or incurred before cash is exchanged, increasing assets or liabilities on the balance sheet; deferrals delay recognition of revenues and expenses after cash is received or paid, adjusting prepaid assets or unearned liabilities.

What are common examples of accruals?

Common examples of accruals include accrued expenses such as wages payable, interest payable, and utilities payable, as well as accrued revenues like earned but unbilled services and rental income receivable.

What are typical examples of deferrals?

Typical examples of deferrals include prepaid expenses, unearned revenue, and deferred tax liabilities.

Why are accruals important for accurate financial reporting?

Accruals ensure financial statements reflect revenues and expenses when they are incurred, providing a true and fair view of a company's financial position and performance.

How do deferrals impact revenue recognition?

Deferrals delay revenue recognition by recording cash received before earning it, ensuring revenue is recognized only when earned according to accrual accounting principles.