Basel I established the first comprehensive international banking regulations focused on credit risk and capital adequacy, setting a minimum capital requirement of 8% for risk-weighted assets. Basel III significantly enhanced these standards by introducing stricter capital definitions, leverage ratios, and liquidity requirements to bolster financial system resilience. Explore the key differences and impacts of Basel I and Basel III to understand the evolution of global banking regulation.

Main Difference

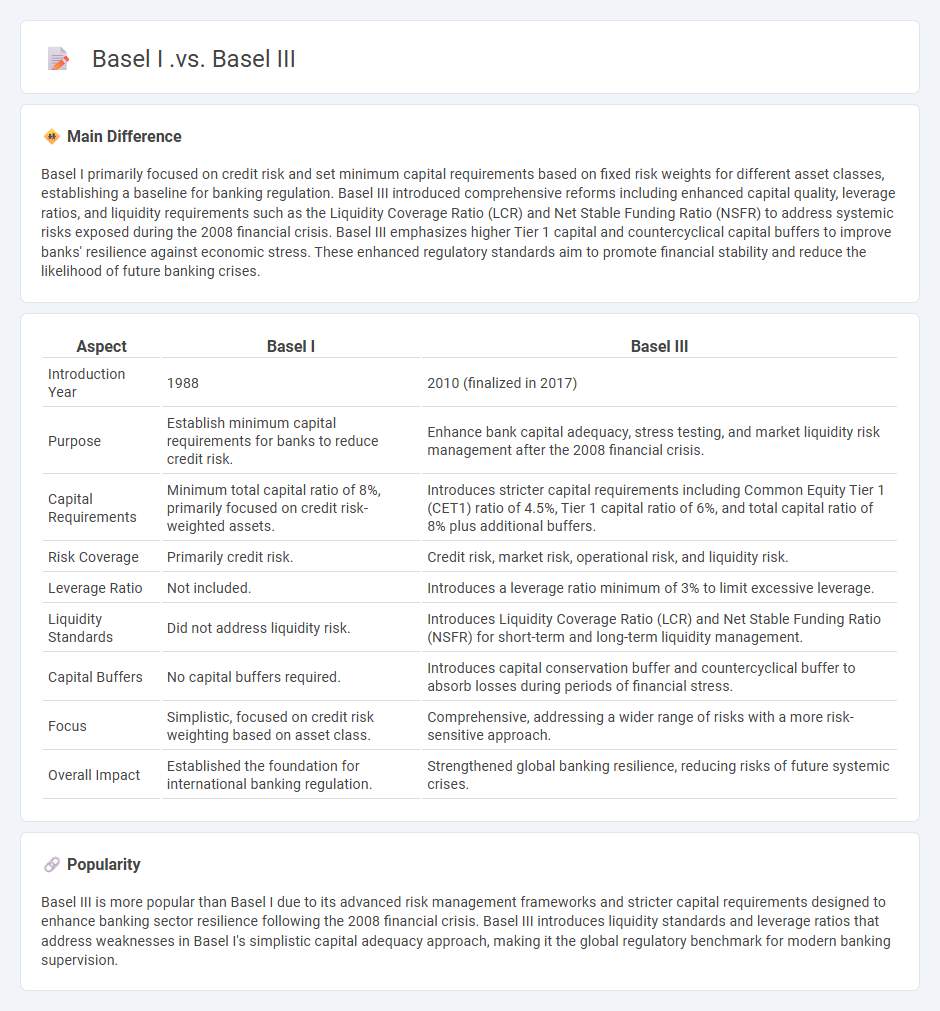

Basel I primarily focused on credit risk and set minimum capital requirements based on fixed risk weights for different asset classes, establishing a baseline for banking regulation. Basel III introduced comprehensive reforms including enhanced capital quality, leverage ratios, and liquidity requirements such as the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) to address systemic risks exposed during the 2008 financial crisis. Basel III emphasizes higher Tier 1 capital and countercyclical capital buffers to improve banks' resilience against economic stress. These enhanced regulatory standards aim to promote financial stability and reduce the likelihood of future banking crises.

Connection

Basel I and Basel III are connected through their common goal of strengthening banking regulation to enhance financial stability. Basel I introduced the initial framework for minimum capital requirements based on credit risk, while Basel III expanded these requirements by incorporating comprehensive measures for market risk, operational risk, and liquidity standards. The evolution from Basel I to Basel III reflects a regulatory response to financial crises by increasing capital adequacy, leverage ratios, and introducing countercyclical buffers.

Comparison Table

| Aspect | Basel I | Basel III |

|---|---|---|

| Introduction Year | 1988 | 2010 (finalized in 2017) |

| Purpose | Establish minimum capital requirements for banks to reduce credit risk. | Enhance bank capital adequacy, stress testing, and market liquidity risk management after the 2008 financial crisis. |

| Capital Requirements | Minimum total capital ratio of 8%, primarily focused on credit risk-weighted assets. | Introduces stricter capital requirements including Common Equity Tier 1 (CET1) ratio of 4.5%, Tier 1 capital ratio of 6%, and total capital ratio of 8% plus additional buffers. |

| Risk Coverage | Primarily credit risk. | Credit risk, market risk, operational risk, and liquidity risk. |

| Leverage Ratio | Not included. | Introduces a leverage ratio minimum of 3% to limit excessive leverage. |

| Liquidity Standards | Did not address liquidity risk. | Introduces Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) for short-term and long-term liquidity management. |

| Capital Buffers | No capital buffers required. | Introduces capital conservation buffer and countercyclical buffer to absorb losses during periods of financial stress. |

| Focus | Simplistic, focused on credit risk weighting based on asset class. | Comprehensive, addressing a wider range of risks with a more risk-sensitive approach. |

| Overall Impact | Established the foundation for international banking regulation. | Strengthened global banking resilience, reducing risks of future systemic crises. |

Capital Adequacy Ratio (CAR)

Capital Adequacy Ratio (CAR) measures a bank's available capital expressed as a percentage of its risk-weighted assets, ensuring financial stability and solvency. Regulators like the Basel Committee on Banking Supervision set minimum CAR requirements, typically 8% under Basel III standards, to mitigate credit, market, and operational risks. Higher CAR indicates stronger capital buffers to absorb losses, protect depositors, and support lending activities. Banks with low CAR face regulatory restrictions and increased vulnerability during economic downturns.

Risk-Weighted Assets (RWA)

Risk-Weighted Assets (RWA) represent the total of all assets held by a bank or financial institution, weighted by credit risk according to regulatory standards like Basel III. RWAs are crucial for determining the minimum capital requirements, ensuring that banks maintain sufficient equity to cover potential losses. The calculation includes on-balance sheet exposures, off-balance sheet items, and operational risks, scaled by risk weights assigned based on asset class and credit quality. Regulators use RWAs to assess a bank's financial stability and enforce capital adequacy ratios, such as the 8% minimum Tier 1 capital ratio under Basel frameworks.

Tier 1 and Tier 2 Capital

Tier 1 capital, also known as core capital, includes common equity, retained earnings, and disclosed reserves, serving as the primary cushion against financial distress and losses. Tier 2 capital, or supplementary capital, comprises items like revaluation reserves, hybrid instruments, and subordinated term debt that provide additional support but are less secure than Tier 1. Banks must maintain a minimum Tier 1 capital ratio of 6% and a total capital ratio (Tier 1 plus Tier 2) of 8% under Basel III regulations to ensure financial stability. These capital requirements help regulators assess the bank's ability to absorb losses and continue operations during economic downturns.

Minimum Capital Requirements

Minimum capital requirements are regulatory standards set by financial authorities to ensure that banks and financial institutions maintain sufficient capital reserves to absorb losses and protect depositors. These requirements are key components of Basel III, which mandates a minimum common equity tier 1 (CET1) capital ratio of 4.5% and a total capital ratio of 8%. Maintaining these capital thresholds helps promote stability in the financial system by reducing the risk of insolvency during economic downturns. Regulators continuously monitor institutions to enforce compliance and mitigate systemic financial risks.

Leverage and Liquidity Standards

Leverage ratios and liquidity standards are critical metrics used by financial institutions to maintain stability and reduce risk. Basel III regulations set specific leverage ratio requirements, typically a minimum of 3%, to limit excessive borrowing relative to equity. Liquidity coverage ratio (LCR) standards require banks to hold high-quality liquid assets sufficient to cover net cash outflows for 30 days under stressed conditions. These measures collectively ensure resilience against financial shocks and promote sustainable banking practices globally.

Source and External Links

Basel Accords - Wikipedia - Basel I, introduced in 1988, established minimum capital requirements for banks focusing mainly on credit risk, while Basel III, developed post-2008 financial crisis, enhanced these requirements by introducing stricter capital standards, liquidity, and leverage ratios to better manage risks and prevent bank failures.

The Basel framework: the global regulatory standards for banks - Basel I laid the groundwork for capital adequacy, while Basel III was designed as a comprehensive reform to strengthen regulation, supervision, and risk management after the 2007-2008 crisis, with new requirements on liquidity and leverage to ensure banks can withstand economic shocks.

What is Basel III - Financial Edge Training - Basel III builds on Basel I and II by increasing capital requirements, introducing new liquidity and leverage rules to improve the banking sector's resilience and transparency in the wake of the global financial crisis.

FAQs

What is Basel I?

Basel I is the 1988 international banking regulatory framework established by the Basel Committee on Banking Supervision to set minimum capital requirements for banks based on risk-weighted assets.

What is Basel III?

Basel III is an international regulatory framework developed by the Basel Committee on Banking Supervision to strengthen bank capital requirements, improve risk management, and enhance banking sector resilience following the 2008 financial crisis.

How do Basel I and Basel III differ in capital requirements?

Basel I requires a minimum Tier 1 capital ratio of 4% and total capital ratio of 8%, focusing mainly on credit risk; Basel III strengthens these by increasing the minimum Tier 1 capital ratio to 6%, introduces a conservation buffer of 2.5%, a countercyclical buffer of up to 2.5%, and imposes stricter risk coverage including capital requirements for market and operational risks.

What risks are covered by Basel I compared to Basel III?

Basel I covers credit risk through standardized risk-weighted assets, while Basel III expands coverage to include credit risk, market risk, operational risk, and introduces capital quality, liquidity requirements (LCR, NSFR), and leverage ratio limits.

How did the introduction of Basel III improve banking regulations?

Basel III improved banking regulations by increasing capital requirements, enhancing risk management standards, introducing liquidity and leverage ratios, and strengthening bank resilience to financial stress.

What are the key components of Basel III not present in Basel I?

Basel III introduces key components absent in Basel I, including higher minimum capital requirements, the leverage ratio, liquidity coverage ratio (LCR), net stable funding ratio (NSFR), enhanced risk coverage for counterparty credit risk, and stricter supervisory review processes.

Why was Basel III implemented after Basel I?

Basel III was implemented after Basel I to address the latter's inadequate capital requirements and risk coverage by introducing stricter capital standards, improved risk management, and enhanced liquidity measures.