Securitization involves pooling financial assets to create marketable securities, transferring risk to investors, and enhancing liquidity. Participation refers to shared ownership or rights in an asset or loan, allowing multiple parties to benefit from cash flows without creating tradable securities. Explore detailed differences and applications of securitization versus participation for deeper financial insights.

Main Difference

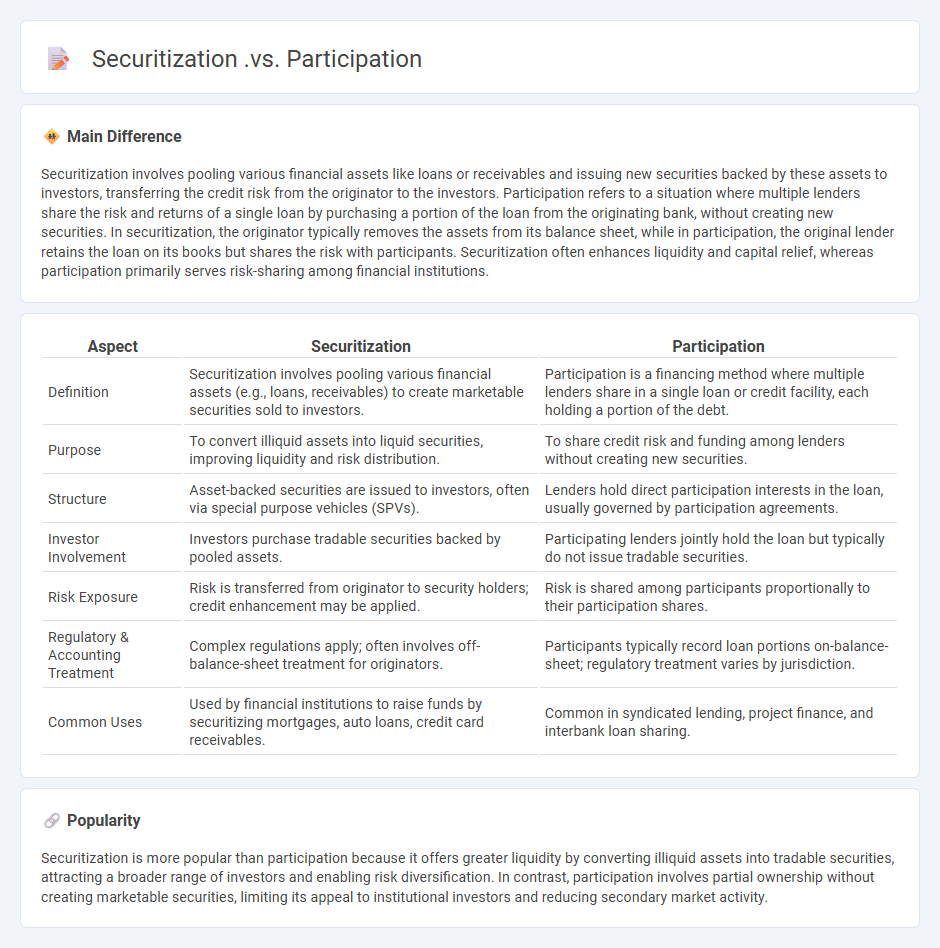

Securitization involves pooling various financial assets like loans or receivables and issuing new securities backed by these assets to investors, transferring the credit risk from the originator to the investors. Participation refers to a situation where multiple lenders share the risk and returns of a single loan by purchasing a portion of the loan from the originating bank, without creating new securities. In securitization, the originator typically removes the assets from its balance sheet, while in participation, the original lender retains the loan on its books but shares the risk with participants. Securitization often enhances liquidity and capital relief, whereas participation primarily serves risk-sharing among financial institutions.

Connection

Securitization transforms illiquid financial assets into marketable securities, enabling investors to participate in asset-backed investment opportunities. Participation involves investors acquiring ownership interests or shares in these securitized assets, providing liquidity and risk diversification. This connection facilitates capital flow from investors to originators through structured financial products.

Comparison Table

| Aspect | Securitization | Participation |

|---|---|---|

| Definition | Securitization involves pooling various financial assets (e.g., loans, receivables) to create marketable securities sold to investors. | Participation is a financing method where multiple lenders share in a single loan or credit facility, each holding a portion of the debt. |

| Purpose | To convert illiquid assets into liquid securities, improving liquidity and risk distribution. | To share credit risk and funding among lenders without creating new securities. |

| Structure | Asset-backed securities are issued to investors, often via special purpose vehicles (SPVs). | Lenders hold direct participation interests in the loan, usually governed by participation agreements. |

| Investor Involvement | Investors purchase tradable securities backed by pooled assets. | Participating lenders jointly hold the loan but typically do not issue tradable securities. |

| Risk Exposure | Risk is transferred from originator to security holders; credit enhancement may be applied. | Risk is shared among participants proportionally to their participation shares. |

| Regulatory & Accounting Treatment | Complex regulations apply; often involves off-balance-sheet treatment for originators. | Participants typically record loan portions on-balance-sheet; regulatory treatment varies by jurisdiction. |

| Common Uses | Used by financial institutions to raise funds by securitizing mortgages, auto loans, credit card receivables. | Common in syndicated lending, project finance, and interbank loan sharing. |

Asset Pooling

Asset pooling in finance refers to the aggregation of various financial assets, such as loans, mortgages, or securities, into a single investment vehicle. This process enhances diversification and risk management by spreading exposure across multiple underlying assets. Common forms of asset pooling include mutual funds, exchange-traded funds (ETFs), and collateralized debt obligations (CDOs). Institutional investors and asset managers leverage pooling to optimize portfolio performance and liquidity while reducing individual investment risk.

Risk Transfer

Risk transfer in finance involves shifting the potential financial losses from one party to another through mechanisms such as insurance policies, derivatives contracts, and hedging strategies. This process mitigates exposure to adverse events by allocating risk to entities better equipped to manage or absorb it, such as insurers or financial institutions. Common tools include credit default swaps, options, and futures that allow organizations to protect against fluctuations in market variables like interest rates, currency exchange rates, or commodity prices. Effective risk transfer enhances stability and predictability in financial planning and investment returns.

Ownership Structure

Ownership structure in finance refers to the distribution of equity shares among individuals, institutions, and entities that hold stakes in a company. It influences corporate control, decision-making processes, and the alignment of interests between shareholders and management. An optimized ownership structure balances concentrated control with dispersed ownership to enhance firm value and reduce agency costs. Studies show that institutional investors and insider ownership significantly impact firm performance and governance quality.

Investor Participation

Investor participation in finance significantly influences capital markets by determining the liquidity and valuation of assets. High investor involvement enhances market efficiency, facilitating the allocation of resources to productive enterprises. Institutional investors, including mutual funds and pension funds, often dominate participation, driving market trends and governance practices. Retail investor engagement also impacts market dynamics, increasingly facilitated by digital trading platforms and financial technology innovations.

Regulatory Framework

The regulatory framework in finance encompasses laws, regulations, and guidelines established by government agencies and international bodies to ensure market integrity, protect investors, and maintain financial stability. Key entities include the Securities and Exchange Commission (SEC) in the United States, the Financial Conduct Authority (FCA) in the UK, and the European Securities and Markets Authority (ESMA) in the EU. Regulations such as the Dodd-Frank Act, Basel III, and MiFID II impose capital requirements, risk management protocols, and transparency standards on financial institutions. Compliance with these regulations reduces systemic risk and fosters trust in global financial markets.

Source and External Links

Securitizations vs participations: Balance sheet flexibility vs. leverage - Securitizations involve retaining more leveraged, volatile equity positions and reduce balance sheet flexibility, while participations provide liquidity, non-interest income, and help de-risk credit exposures, enhancing capacity for new loans and flexible capital allocation.

Drafting and Securitizing Participation Mortgages: A Re-Introduction - Participation mortgages can be securitized if properly drafted and procedures followed, though the complexity is higher due to contingent interest participation features.

Loan Participations: Are They "Securities"? - Loan participations give participants limited control and information, affecting their treatment under securities laws, and typically are less complex and less risky compared to securitizations.

FAQs

What is securitization?

Securitization is the financial process of pooling various types of debt instruments, such as mortgages or loans, and converting them into tradable securities to be sold to investors.

What is participation in finance?

Participation in finance refers to the ownership interest or share an investor holds in a financial asset, investment, or partnership, enabling them to receive returns or profits proportional to their stake.

How does securitization differ from participation?

Securitization involves pooling financial assets and issuing new securities backed by those assets, transferring both ownership and risk to investors; participation grants investors a proportional interest in existing assets without transferring ownership or risk, maintaining the original owner's claims.

What are the key advantages of securitization?

Securitization enhances liquidity by converting illiquid assets into marketable securities, reduces funding costs through diversification of investor base, transfers credit risk from originators to investors, improves balance sheet management, and increases capital efficiency for financial institutions.

What are the main benefits of loan participation?

Loan participation offers benefits including risk diversification, increased lending capacity, enhanced liquidity, and shared credit exposure among participating lenders.

How do risks compare between securitization and participation?

Securitization transfers credit and liquidity risks to investors through asset-backed securities, while participation involves shared credit risk between the originator and participant without transferring ownership.

When should a financial institution choose securitization over participation?

A financial institution should choose securitization over participation when it aims to transfer credit risk off-balance sheet, raise funds through capital market investors, enhance liquidity by converting assets into marketable securities, and achieve regulatory capital relief.