Monte Carlo Simulation uses random sampling to model the probability of different outcomes in financial forecasting, capturing a wide range of possible scenarios with high computational intensity. The Binomial Tree Model structures possible price movements in discrete time steps, providing a simpler, lattice-based approach to option pricing and decision analysis. Explore the differences and applications of these simulation methods to enhance your financial modeling strategies.

Main Difference

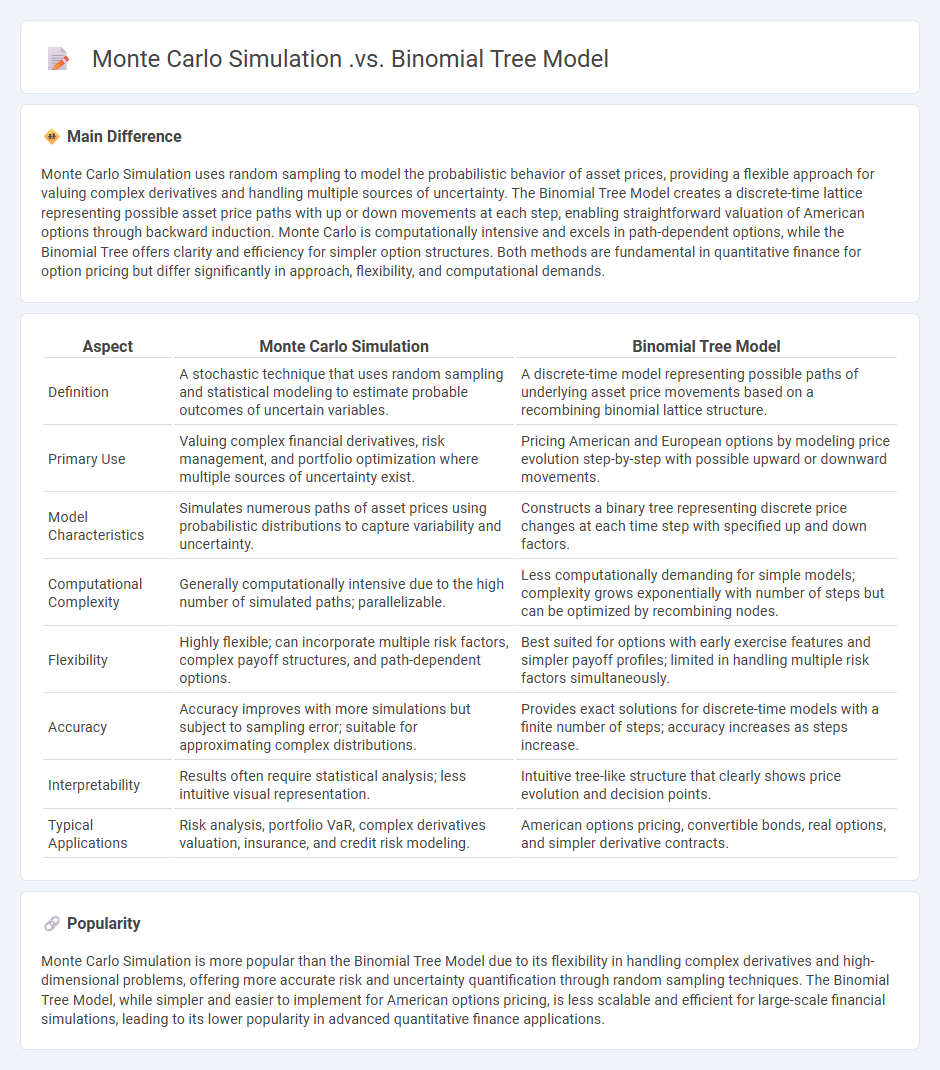

Monte Carlo Simulation uses random sampling to model the probabilistic behavior of asset prices, providing a flexible approach for valuing complex derivatives and handling multiple sources of uncertainty. The Binomial Tree Model creates a discrete-time lattice representing possible asset price paths with up or down movements at each step, enabling straightforward valuation of American options through backward induction. Monte Carlo is computationally intensive and excels in path-dependent options, while the Binomial Tree offers clarity and efficiency for simpler option structures. Both methods are fundamental in quantitative finance for option pricing but differ significantly in approach, flexibility, and computational demands.

Connection

Monte Carlo Simulation and Binomial Tree Model both serve as computational methods for option pricing by estimating the potential future paths of underlying asset prices. The Binomial Tree Model discretizes possible price movements at each time step allowing for a structured evaluation of option value through backward induction, while Monte Carlo Simulation generates numerous random price paths using stochastic processes to approximate the expected payoff. Both techniques rely on probabilistic frameworks and risk-neutral valuation principles, enabling analysts to assess complex derivatives under varying market conditions.

Comparison Table

| Aspect | Monte Carlo Simulation | Binomial Tree Model |

|---|---|---|

| Definition | A stochastic technique that uses random sampling and statistical modeling to estimate probable outcomes of uncertain variables. | A discrete-time model representing possible paths of underlying asset price movements based on a recombining binomial lattice structure. |

| Primary Use | Valuing complex financial derivatives, risk management, and portfolio optimization where multiple sources of uncertainty exist. | Pricing American and European options by modeling price evolution step-by-step with possible upward or downward movements. |

| Model Characteristics | Simulates numerous paths of asset prices using probabilistic distributions to capture variability and uncertainty. | Constructs a binary tree representing discrete price changes at each time step with specified up and down factors. |

| Computational Complexity | Generally computationally intensive due to the high number of simulated paths; parallelizable. | Less computationally demanding for simple models; complexity grows exponentially with number of steps but can be optimized by recombining nodes. |

| Flexibility | Highly flexible; can incorporate multiple risk factors, complex payoff structures, and path-dependent options. | Best suited for options with early exercise features and simpler payoff profiles; limited in handling multiple risk factors simultaneously. |

| Accuracy | Accuracy improves with more simulations but subject to sampling error; suitable for approximating complex distributions. | Provides exact solutions for discrete-time models with a finite number of steps; accuracy increases as steps increase. |

| Interpretability | Results often require statistical analysis; less intuitive visual representation. | Intuitive tree-like structure that clearly shows price evolution and decision points. |

| Typical Applications | Risk analysis, portfolio VaR, complex derivatives valuation, insurance, and credit risk modeling. | American options pricing, convertible bonds, real options, and simpler derivative contracts. |

Stochastic Processes

Stochastic processes play a critical role in finance by modeling the random dynamics of asset prices, interest rates, and market variables over time. The most commonly used stochastic models include the Geometric Brownian Motion for stock prices, the Cox-Ingersoll-Ross model for interest rates, and Levy processes for capturing jumps and heavy tails in returns distributions. These models enable quantitative analysts to price derivatives, assess risk, and optimize portfolios using tools such as the Black-Scholes-Merton formula and Monte Carlo simulations. Accurate estimation of parameters like volatility and drift is essential for the robustness of financial forecasting and risk management strategies.

Path Dependency

Path dependency in finance refers to the concept where the outcome of financial processes or decisions is influenced by historical events or past trajectories rather than just current conditions. This phenomenon is particularly evident in investment strategies, market trends, and company performance, where previous successes or failures shape future options and risks. An example includes momentum investing, where past asset price movements guide ongoing investment decisions, reinforcing existing trends. Understanding path dependency helps in risk management and forecasting by incorporating the impact of historical market behaviors on financial outcomes.

Option Pricing

Option pricing involves determining the fair value of derivative contracts that grant the right to buy or sell an underlying asset at a specified price before or on a certain date. Models like the Black-Scholes formula and the Binomial tree method use factors such as the underlying asset's current price, strike price, volatility, time to expiration, risk-free interest rate, and dividends to estimate option premiums. Implied volatility extracted from market prices reflects expected future volatility and influences option valuations significantly. Accurate option pricing is essential for risk management, trading strategies, and financial decision-making in equity, commodities, and foreign exchange markets.

Computational Complexity

Computational complexity in finance plays a critical role in optimizing portfolio management, risk assessment, and algorithmic trading strategies by efficiently processing vast datasets and complex mathematical models. Techniques such as Monte Carlo simulations, numerical optimization, and machine learning algorithms address challenges in high-dimensional data and nonlinear financial markets. Advanced computational methods enable real-time decision-making and accurate pricing of derivatives, improving market stability and profitability. Financial institutions increasingly invest in high-performance computing infrastructure to tackle these computational demands and maintain competitive advantages.

American vs. European Options

American options allow holders to exercise the contract at any time before expiration, providing greater flexibility for strategic trading. European options restrict exercise rights to the expiration date only, often resulting in lower premiums due to reduced flexibility. Traders and investors frequently choose American options for stocks and exchange-traded derivatives, while European options are commonly used for index options and foreign exchange contracts. Understanding the distinction impacts pricing models like the Black-Scholes model, which originally applies to European-style options only.

Source and External Links

Binomial VS Monte Carlo - Xeon Protocol Docs - This webpage compares binomial and Monte Carlo simulations for options pricing, highlighting that binomial models are simpler and less computationally intensive, while Monte Carlo simulations are more accurate and flexible.

Battle of the Pricing Models: Trees vs Monte Carlo - Savvysoft - This article discusses the differences and similarities between binomial trees and Monte Carlo simulations, noting their applications in pricing derivatives.

Comparing Binomial and Monte Carlo with Black Scholes - QuantNet - This discussion compares the binomial option pricing model and Monte Carlo simulation with the Black-Scholes formula, highlighting how both approximate the Black-Scholes value under certain conditions.

FAQs

What is a Monte Carlo simulation?

A Monte Carlo simulation is a computational technique that uses random sampling and statistical modeling to estimate the probability distribution of complex systems or processes.

What is a binomial tree model?

A binomial tree model is a discrete-time quantitative method used in finance to value options by simulating possible price paths of the underlying asset through a recombining tree structure of upward and downward movements.

How does Monte Carlo simulation work in finance?

Monte Carlo simulation in finance models the probability of different outcomes by running thousands of randomized scenarios based on underlying variables such as asset prices, interest rates, or market volatility to estimate risk, value derivatives, and forecast portfolio performance.

How does the binomial tree model estimate option prices?

The binomial tree model estimates option prices by constructing a discrete-time price lattice that simulates possible underlying asset prices at each time step, calculating option payoffs at the final nodes, and then working backward through the tree using risk-neutral probabilities to determine the present value of the option.

What are the key differences between Monte Carlo simulation and binomial tree model?

Monte Carlo simulation uses random sampling to model complex stochastic processes and estimate the distribution of possible outcomes, while the binomial tree model employs a discrete-time lattice framework to evaluate multiple possible price paths in a recombining tree structure, primarily for option pricing. Monte Carlo is better suited for high-dimensional problems and path-dependent options, whereas the binomial tree offers computational efficiency for American options and simpler derivatives.

When should you use Monte Carlo simulation instead of a binomial tree model?

Use Monte Carlo simulation instead of a binomial tree model when valuing complex derivatives with multiple sources of uncertainty, path-dependent features, or high-dimensional problems where binomial trees become computationally infeasible.

What are the advantages and limitations of each method?

Advantages of Method A include high accuracy and scalability; limitations involve higher cost and longer implementation time. Method B offers faster deployment and lower expenses; limitations consist of reduced precision and limited functionality.