Sinking funds require issuers to regularly set aside money to repay bondholders, reducing credit risk and enhancing bond safety, while callable bonds grant issuers the right to redeem bonds before maturity, often leading to reinvestment risk for investors. The presence of a sinking fund can lower borrowing costs due to increased security, whereas callable bonds usually offer higher yields to compensate for early redemption risk. Explore the differences in detail to understand how these features impact investment strategies and bond valuations.

Main Difference

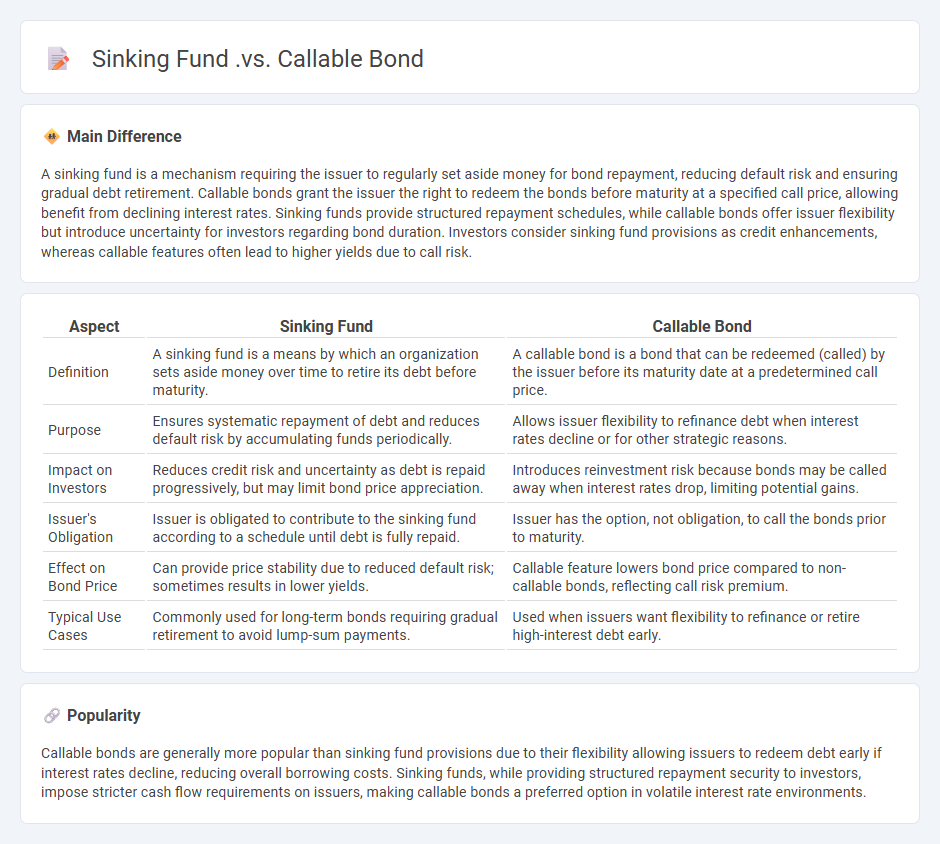

A sinking fund is a mechanism requiring the issuer to regularly set aside money for bond repayment, reducing default risk and ensuring gradual debt retirement. Callable bonds grant the issuer the right to redeem the bonds before maturity at a specified call price, allowing benefit from declining interest rates. Sinking funds provide structured repayment schedules, while callable bonds offer issuer flexibility but introduce uncertainty for investors regarding bond duration. Investors consider sinking fund provisions as credit enhancements, whereas callable features often lead to higher yields due to call risk.

Connection

A sinking fund is a reserve set up by an issuer to periodically repurchase or redeem callable bonds before maturity, reducing credit risk and ensuring timely debt repayment. Callable bonds provide issuers the option to redeem the bond early, often utilizing sinking fund payments to manage debt efficiently and reduce interest costs. This connection enhances issuer flexibility while providing investors structured repayment schedules.

Comparison Table

| Aspect | Sinking Fund | Callable Bond |

|---|---|---|

| Definition | A sinking fund is a means by which an organization sets aside money over time to retire its debt before maturity. | A callable bond is a bond that can be redeemed (called) by the issuer before its maturity date at a predetermined call price. |

| Purpose | Ensures systematic repayment of debt and reduces default risk by accumulating funds periodically. | Allows issuer flexibility to refinance debt when interest rates decline or for other strategic reasons. |

| Impact on Investors | Reduces credit risk and uncertainty as debt is repaid progressively, but may limit bond price appreciation. | Introduces reinvestment risk because bonds may be called away when interest rates drop, limiting potential gains. |

| Issuer's Obligation | Issuer is obligated to contribute to the sinking fund according to a schedule until debt is fully repaid. | Issuer has the option, not obligation, to call the bonds prior to maturity. |

| Effect on Bond Price | Can provide price stability due to reduced default risk; sometimes results in lower yields. | Callable feature lowers bond price compared to non-callable bonds, reflecting call risk premium. |

| Typical Use Cases | Commonly used for long-term bonds requiring gradual retirement to avoid lump-sum payments. | Used when issuers want flexibility to refinance or retire high-interest debt early. |

Principal Repayment Structure

Principal repayment structure in finance refers to the schedule and method by which the original loan amount or bond principal is repaid over time. Common structures include bullet repayment, where the entire principal is paid at maturity, and amortizing repayment, where both principal and interest are paid periodically, reducing the loan balance gradually. Sinking fund provisions require regular payments into a fund used to retire principal before maturity, often seen in corporate bonds. Understanding the repayment structure is crucial for cash flow planning and credit risk assessment.

Early Redemption Option

The early redemption option allows bondholders or investors to redeem their securities before the scheduled maturity date, often at a premium or specified price. This feature is commonly found in callable bonds, enabling issuers to manage interest rate risk or refinance debt under favorable market conditions. Investors benefit from potential early repayment but may face reinvestment risk if interest rates have declined. Legal terms and specific conditions governing early redemption vary depending on the bond indenture and issuer policies.

Investor Risk Exposure

Investor risk exposure measures the potential financial loss an investor faces due to market fluctuations, asset volatility, or economic changes. It encompasses multiple types of risks including market risk, credit risk, liquidity risk, and operational risk. Understanding risk exposure helps in portfolio diversification and risk management strategies to optimize returns relative to the investor's risk tolerance. Quantitative tools like Value at Risk (VaR) and stress testing are commonly used for assessing and mitigating investor risk exposure.

Issuer Flexibility

Issuer flexibility in finance refers to the ability of an issuer, such as a corporation or government entity, to modify the terms of a security after issuance. This includes adjusting interest rates, maturity dates, or redemption options to better align with market conditions or strategic objectives. Enhanced issuer flexibility can improve capital-raising efficiency and investor appeal by allowing responsive adaptations to economic fluctuations. Examples include callable bonds, convertible securities, and adjustable-rate notes that provide issuers with options to optimize financing costs.

Yield Impact

Yield impact refers to the change in investment returns caused by fluctuations in interest rates, credit risk, or market conditions. It is crucial in fixed income securities, where bond prices inversely correlate with yield variations, affecting portfolio performance. Yield impact analysis helps financial analysts assess risk-adjusted returns and make informed asset allocation decisions. Accurate modeling of yield impacts supports strategies for mitigating losses during economic volatility and optimizing yield curves.

Source and External Links

Callable Bonds: Sinkable Bonds vs: Callable Bonds: Which to Choose - This article compares sinking fund bonds, which provide security through a scheduled repayment plan, with callable bonds, which allow issuers to redeem bonds early, often to take advantage of lower interest rates.

Sinkable Bond Essentials: Mechanisms, Benefits, and ... - This resource details the advantages and disadvantages of sinkable bonds, including their ability to provide early debt repayment and enhance issuer goodwill, but potentially erode investor confidence.

Callable or Redeemable Bonds - Investor.gov - This webpage explains callable bonds and sinking fund redemptions, where bonds can be redeemed early by the issuer, impacting investor returns and interest payments.

FAQs

What is a sinking fund?

A sinking fund is a financial strategy where an organization or individual sets aside money regularly to repay debt or replace a major asset in the future.

What is a callable bond?

A callable bond is a type of bond that allows the issuer to redeem the bond before its maturity date at a specified call price.

How does a sinking fund work in bonds?

A sinking fund in bonds requires the issuer to periodically set aside money to repay bondholders, reducing default risk and ensuring timely redemption of the bond principal.

What are the benefits of a sinking fund for investors?

A sinking fund reduces default risk, enhances bond credit ratings, ensures systematic debt repayment, and increases investor confidence by providing a reliable mechanism for capital preservation.

How do callable bonds affect investors’ returns?

Callable bonds limit investors' returns by allowing issuers to redeem the bonds before maturity, usually at a premium, reducing potential interest income and capital gains.

What is the difference between sinking fund and callable bond features?

A sinking fund requires the issuer to periodically set aside funds to repay bond principal, reducing default risk; callable bond features allow the issuer to redeem the bond before maturity, typically to refinance at lower interest rates.

Why do companies use sinking funds or issue callable bonds?

Companies use sinking funds to systematically repay bond principal, reducing default risk and enhancing creditworthiness; they issue callable bonds to retain the flexibility to refinance debt at lower interest rates when market conditions improve.